Janet Yellen was in the hot seat yesterday before the Senate Banking Committee. Due to a remarkably public vetting process, the presidential nomination for US Federal Reserve Chair that put her there also constituted a comedown for Yellen’s principal rival for the job: Larry Summers. At an International Monetary Fund Conference in honor of former Bank of Israel Governor—and earlier IMF chief economist—Stan Fischer on Nov. 8, Summers made a strong bid for continued relevance to economic policy-making as a private citizen with a trenchant speech. (David Wessel gives an overall report on the conference in this Wall Street Journal article.) Here is the speech:

Janet Yellen was in the hot seat yesterday before the Senate Banking Committee. Due to a remarkably public vetting process, the presidential nomination for US Federal Reserve Chair that put her there also constituted a comedown for Yellen’s principal rival for the job: Larry Summers. At an International Monetary Fund Conference in honor of former Bank of Israel Governor—and earlier IMF chief economist—Stan Fischer on Nov. 8, Summers made a strong bid for continued relevance to economic policy-making as a private citizen with a trenchant speech. (David Wessel gives an overall report on the conference in this Wall Street Journal article.) Here is the speech:

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Summers begins by crediting Fischer for inspiring him to be a macroeconomist, saying this of Fischer’s graduate course on Monetary Economics at MIT: “It was a remarkable intellectual experience. And it was remarkable also because Stan never lost sight of the fact that this was not just an intellectual game: getting these questions right made a profound difference in the lives of nations and their peoples.” Summers transmitted that attitude to me as one of my professors at Harvard, and I have tried to hand it on to my own students.

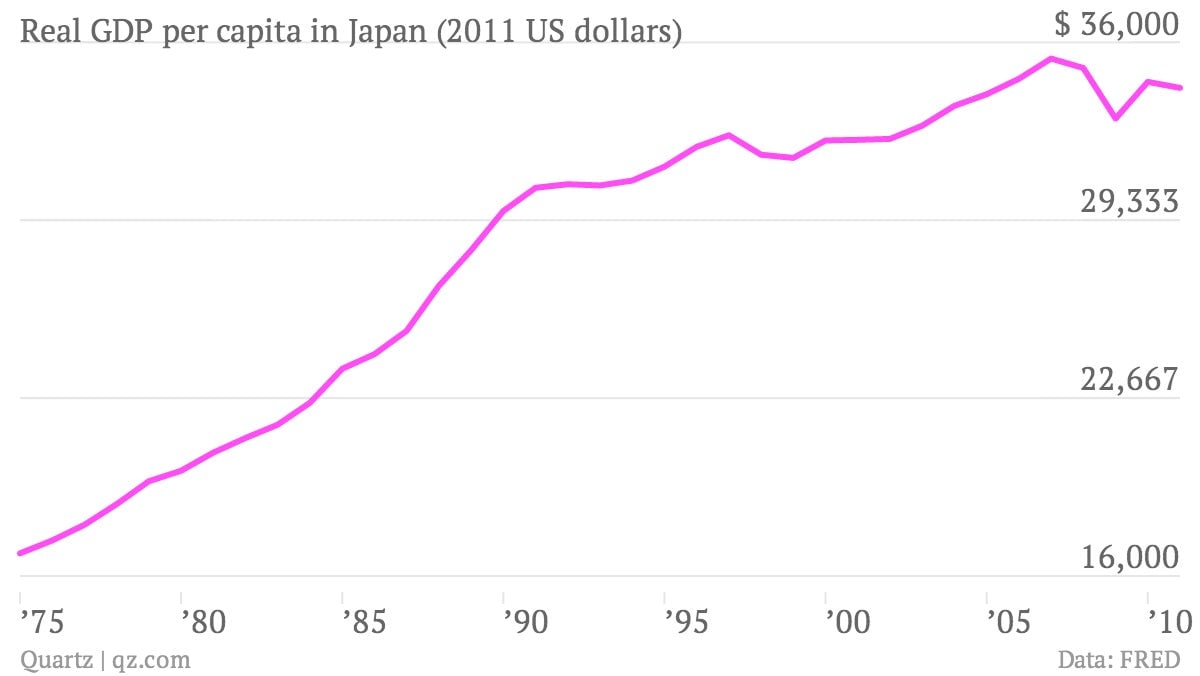

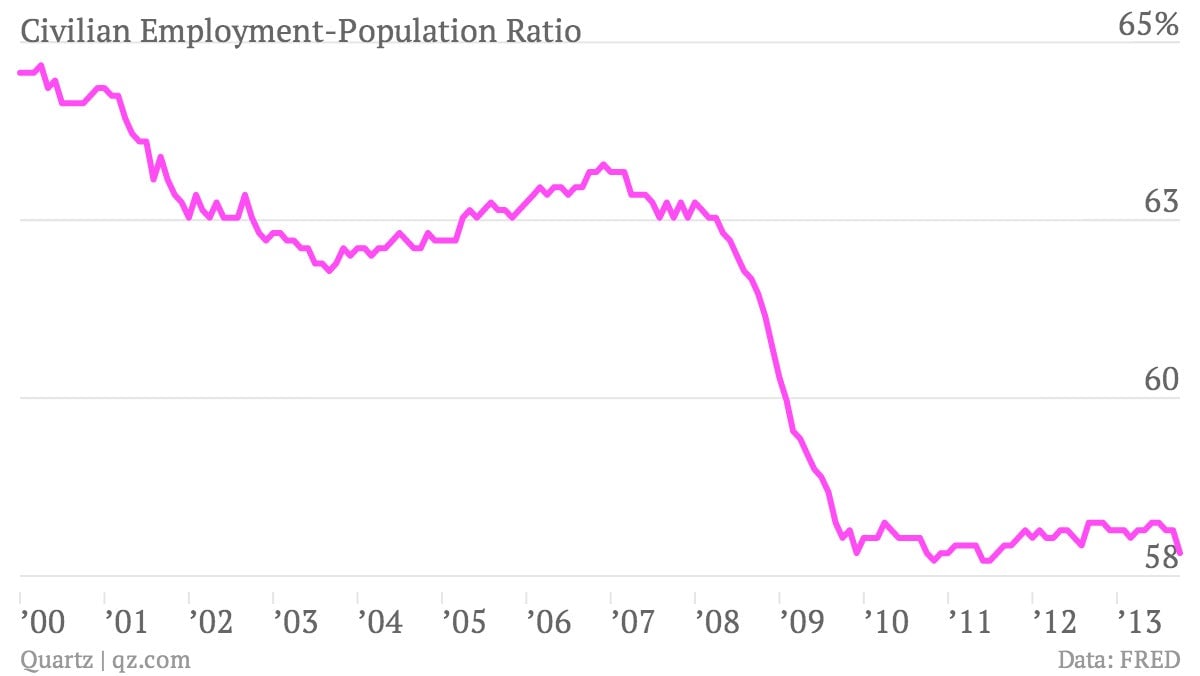

After his praise of Fischer, Summers gives a conventional account of the financial crisis in the fall of 2008 and the largely successful efforts to contain that crisis. But the rest of his speech goes in surprising directions. Summers emphasizes the possibility of “secular stagnation” like that the Japanese economy has suffered in the last two decades. The extent of Japan’s stagnation is breathtaking: In 2013, the Japanese economy is only half the size economists in the 1990’s predicted it would be by now. Even here in the US, GDP is falling further and further behind what we would have predicted just a few years back, and the fraction of the population that has a job has hardly recovered at all in the past four years, despite the fact that the financial crisis was well-contained by November 2009.

What lies behind the stagnation the Japanese economy has suffered in the last two decades and that Summers fears for the United States? He suggests this:

Suppose that the short-term real interest rate that was consistent with full employment had fallen to negative 2% or negative 3% sometime in the middle of the last decade.

With a 2% rate of inflation, an interest rate 3% below inflation would be a negative 1% interest rate in ordinary terms (what macroeconomists would call a -1% nominal interest rate.) But conventional monetary policy can’t reach an interest rate as low as -1%, because anyone can lend as much as they want to the government at 0% by piling up paper currency. This is the zero lower bound on nominal interest rates that macroeconomists justly obsess over. The zero lower bound creates situations where interest rates seem low, but are not low enough to put the economy in high gear.

In the years before the financial crisis, financial excess propped the economy up without ever getting to the kind of excess demand that would push unemployment down to unsustainably low levels and cause higher inflation. In Summers’ words:

Even a great bubble wasn’t enough to produce any excess of aggregate demand…Even with artificial stimulus to demand, coming from all this financial imprudence, you wouldn’t see any excess.

After the financial crisis, the end of financial excess left too little demand and stagnant employment.

What can be done? It isn’t easy to fix things:

Here is Larry Summers’s conclusion, which stops just short of what the US and the world economy needs—a solution:

It is not over until it is over…We may well need, in the years ahead, to think about how we manage an economy in which the zero nominal interest rate is a chronic and systemic inhibitor of economic activity, holding our economies back, below their potential.

So let me return to versions of two of the questions I posed at the end of July, in “Three big questions for Larry Summers, Janet Yellen, and anyone else who wants to head the Fed.”

Though crucial, diagnosing a problem is not enough. Every diagnosis suggests places to look for a cure. If the zero lower bound is the problem, then getting rid of it is an obvious solution. The economists I talk to, including the many economists I have talked to in central banks around the world, recognize that the real difficulties in eliminating the zero lower bound are political difficulties rather than technical difficulties. So the major economies of the world and the many smaller ones that face the zero lower bound have a choice: politics as usual, with a real chance of secular stagnation, or paving the way for negative interest rates. Politics will stay the same until a critical mass of people do what it takes to make them different. Summers proved at the IMF conference that he is still an economic policy heavyweight—someone who could contribute a lot toward reaching that critical mass in the war against the zero lower bound, if he is willing to join the fight.

Follow Miles on Twitter $TWTR at@mileskimball. His blog is supplysideliberal.com. We welcome your comments at [email protected].