As the high-stakes wrangling over the fiscal cliff gets underway, we thought it might be the proper moment to remind everybody just how the United States managed to become the world’s biggest debtor.

As the high-stakes wrangling over the fiscal cliff gets underway, we thought it might be the proper moment to remind everybody just how the United States managed to become the world’s biggest debtor.

So, here’s how.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

As the high-stakes wrangling over the fiscal cliff gets underway, we thought it might be the proper moment to remind everybody just how the United States managed to become the world’s biggest debtor.

So, here’s how.

The US was born in debt. The earliest full reckoning of US national debt was compiled by Alexander Hamilton, the first US Treasury Secretary, who was sort of like the Nate Silver of his era—a self-taught economist.

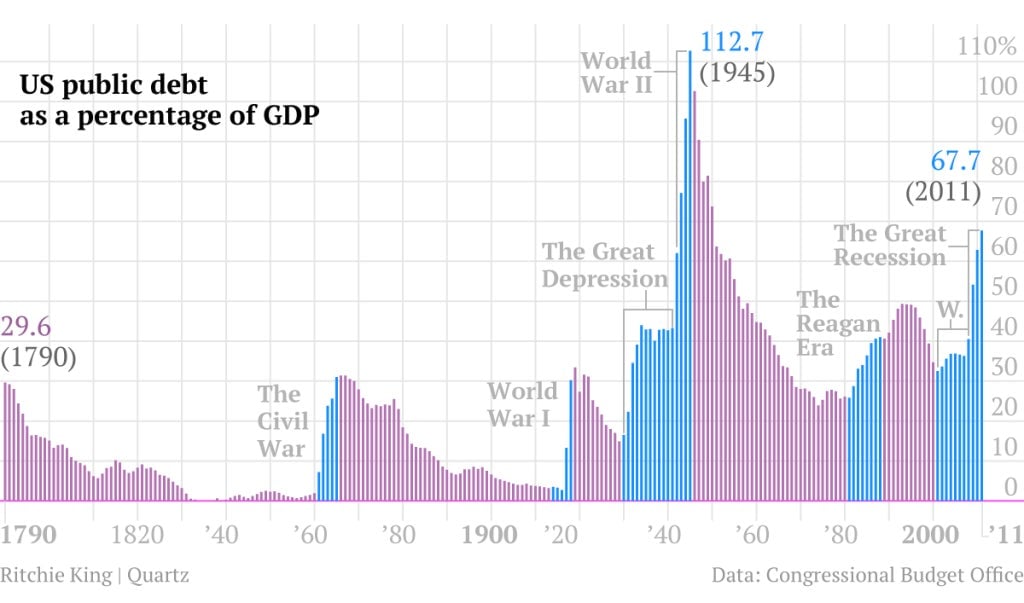

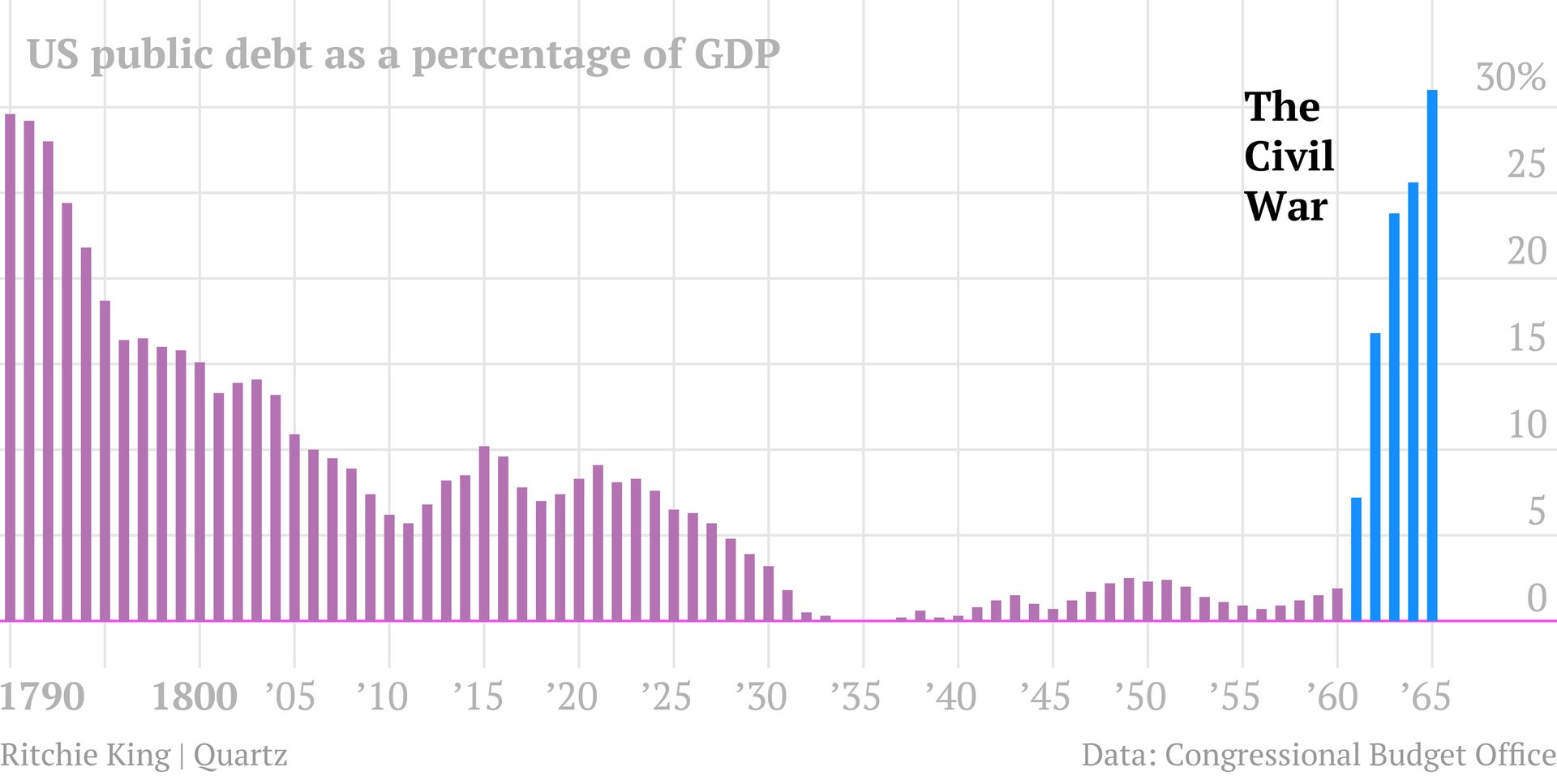

The analysis dates to 1790 and puts the newborn US at around a 30% debt-to-GDP ratio, with the debt a bit higher than $75 million. Where did that debt come from? Well, the Continental Congress, the rough equivalent of the Federal government in revolution-era America, lacked the power to tax. It first tried to pay for stuff by printing money. This currency, known as the Continental, collapsed. The nascent US government also raised cash by borrowing under all sorts of authorities. This National Bureau of Economic Research working paper lists them:

These included certificates issued by the Registrar of the Treasury, the Commissioners of Loans of the States, the Commissioners for the adjustment of accounts of the Quartermaster, Commissary, Hospital, Clothing and Marine Departments, the Paymaster General, and the Commissioner of Army Accounts. In addition, interest on these certificates had often been paid in further certificates known as ‘indents of interest.’

All in, the US owed about $11.7 million to foreigners, mostly to Dutch bankers and the French government, and about $42 million to domestic creditors. The states also had a ton of debt (about $25 million, Hamilton reckoned), which the Federal Government assumed—take a hint, euro zone!—in 1790.

As Secretary of the Treasury, Hamilton was laser-focused on the debt, not so much to pay it off, but rather just to ensure that the fledging government could make all its payments to creditors. How? Well, tariffs and taxes. Americans were cool with that? No, 0f course not. People hated it. After all, the country had just fought a war inspired in part by a revolt against the taxation imposed by the British.

But the federal government stuck to its guns, literally suppressing an armed anti-tax uprising in western Pennsylvania in 1794, known as the Whiskey Rebellion. Meanwhile, the economy grew, helping to shrink debt-to-GDP. Later on, Hamilton’s arch-nemesis, Thomas Jefferson, was even more focused on paying off the debt as fast as possible, driving US debt-to-GDP below 10%. All this work was undone, when the US had to borrow heavily to finance the war of 1812.

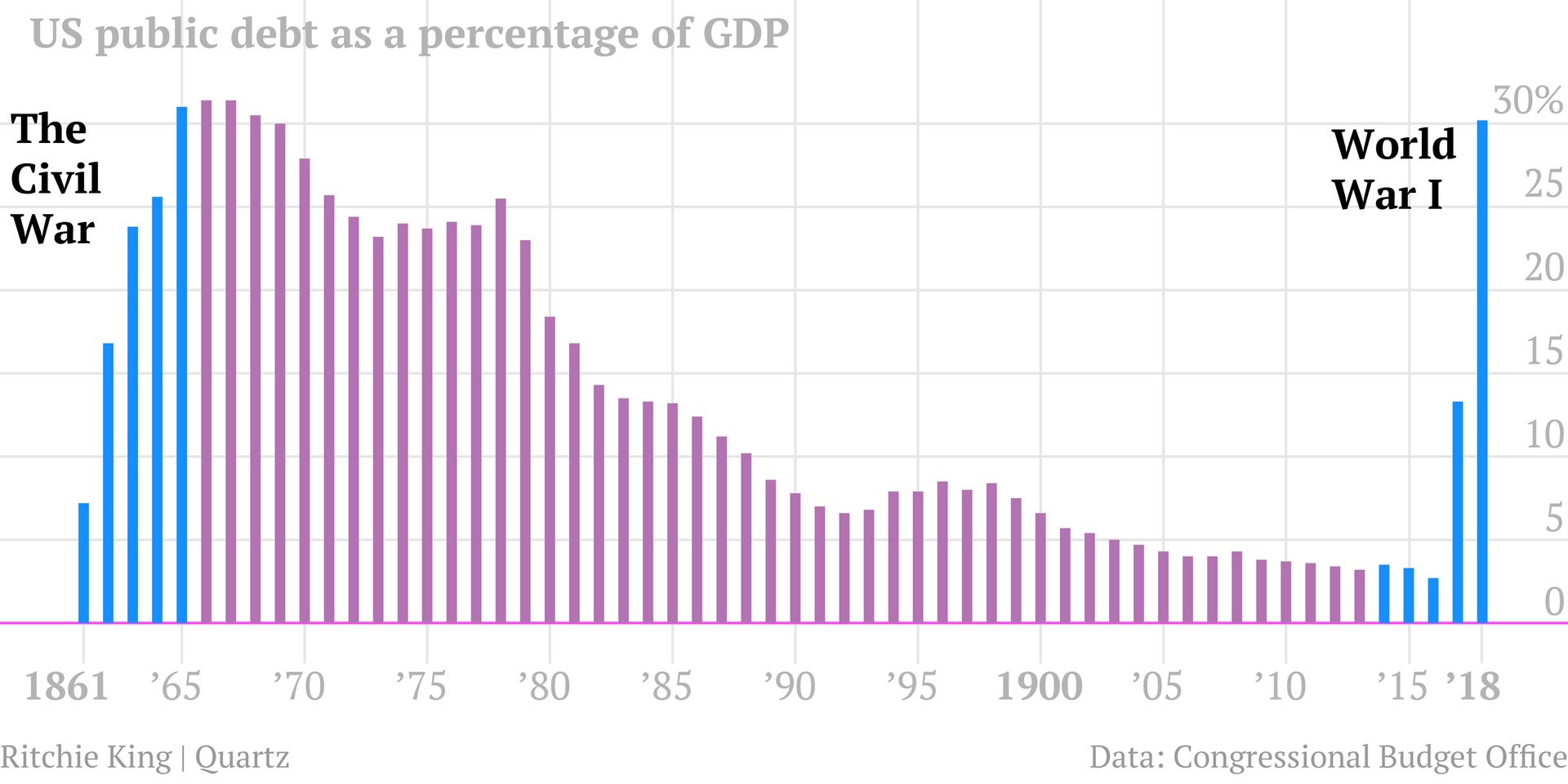

The next major surge in debt coincided with the US Civil War. The federal government was nearly debt-free before the war. The public debt surged from about $65 million in 1860 to $2.76 billion in 1866. (The Lincoln administration also signed into law the first income tax in the country’s history in 1862, which was repealed 10 years later.) The debt would never get below $900 million again. But a surge of late-19th-century economic growth, with a bit of inflation, helped the US gradually reduce the the Civil War debt as a percentage of economic output.

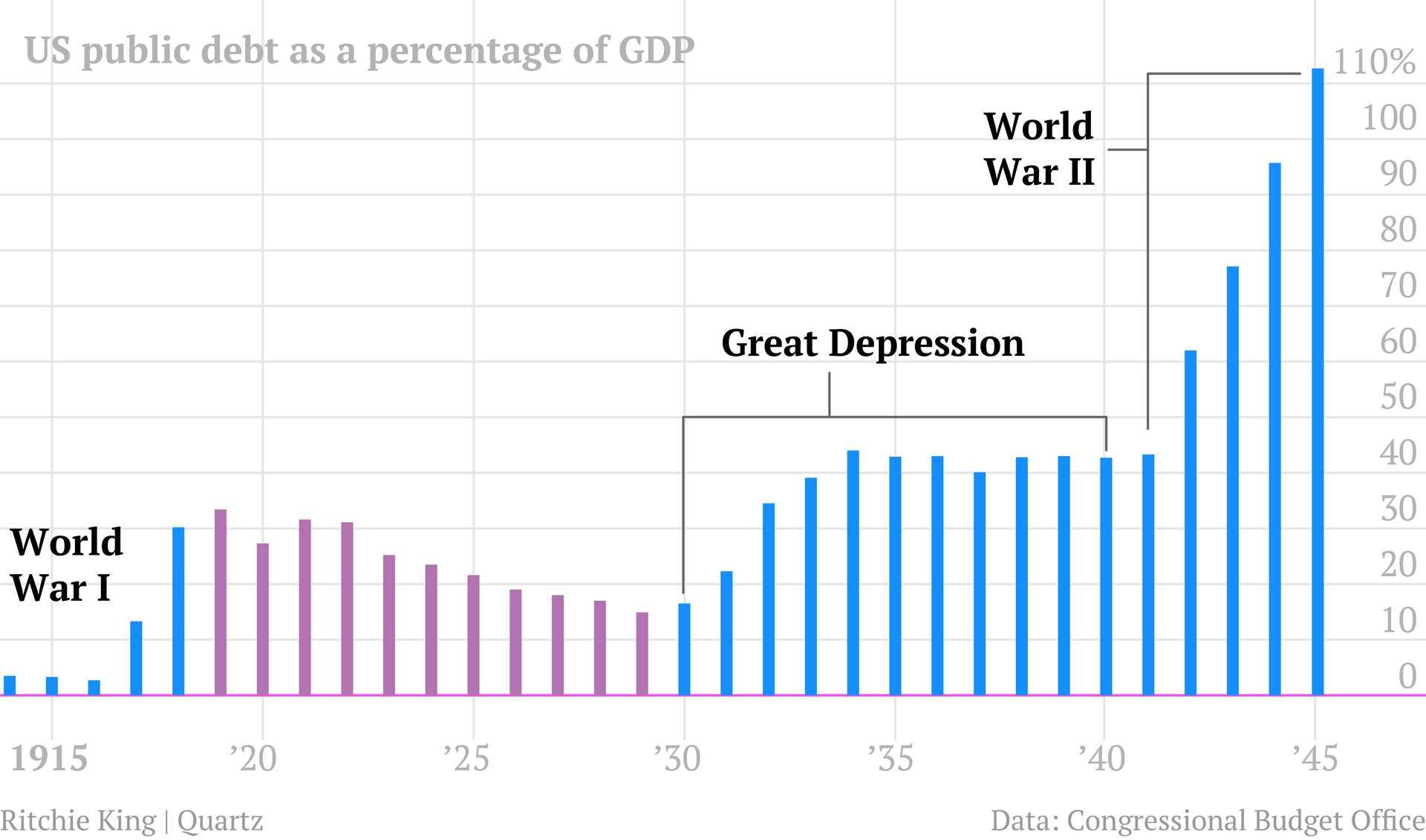

Again, from a GDP perspective, the US was virtually debt-free before sending the doughboys to France. In 1916, as a share of the economy the debt accounted for just 2.7% . The surge in debt associated with World War I was financed largely by selling bonds to the US public. (By the time the US entered the war, pretty much all the other major powers were already in it up to their necks, and thus, didn’t have any money to lend.)

In the aftermath of the war, the Uncle Sam hit a new record high debt-to-GDP of about 33%, with more than $25 billion in debts, or about $334 billion in today’s dollars. But with a combination of budget surpluses, expenditures aimed explicitly at paying off debt early, and payments from the losers of war, the US made significant progress in whittling the debt down. It fell by more than $9 billion by 1930, a reduction of more than a third.

This period coincided with a period of Republican dominance in the US, in which taxes were cut repeatedly from high wartime levels. But at the same time there was widespread agreement that taxes had to be sufficient to pay down the debt.

It’s also worth noting that this is the period when the US congress effectively ceded a large part of its authority over how much the country borrows. Before World War I, the Congress voted to approve the individual debt sales that were used to finance projects like the construction of the Panama canal and the the Spanish-American war. To give the Treasury more flexibility to raise money during World War I, the Congress agreed to set an overall limit to what the Treasury could borrow, but not to demand a say on each individual sale of Treasury bonds. That overall limit is the ancestor of the debt limit that was the source of so much consternation in late 2011.

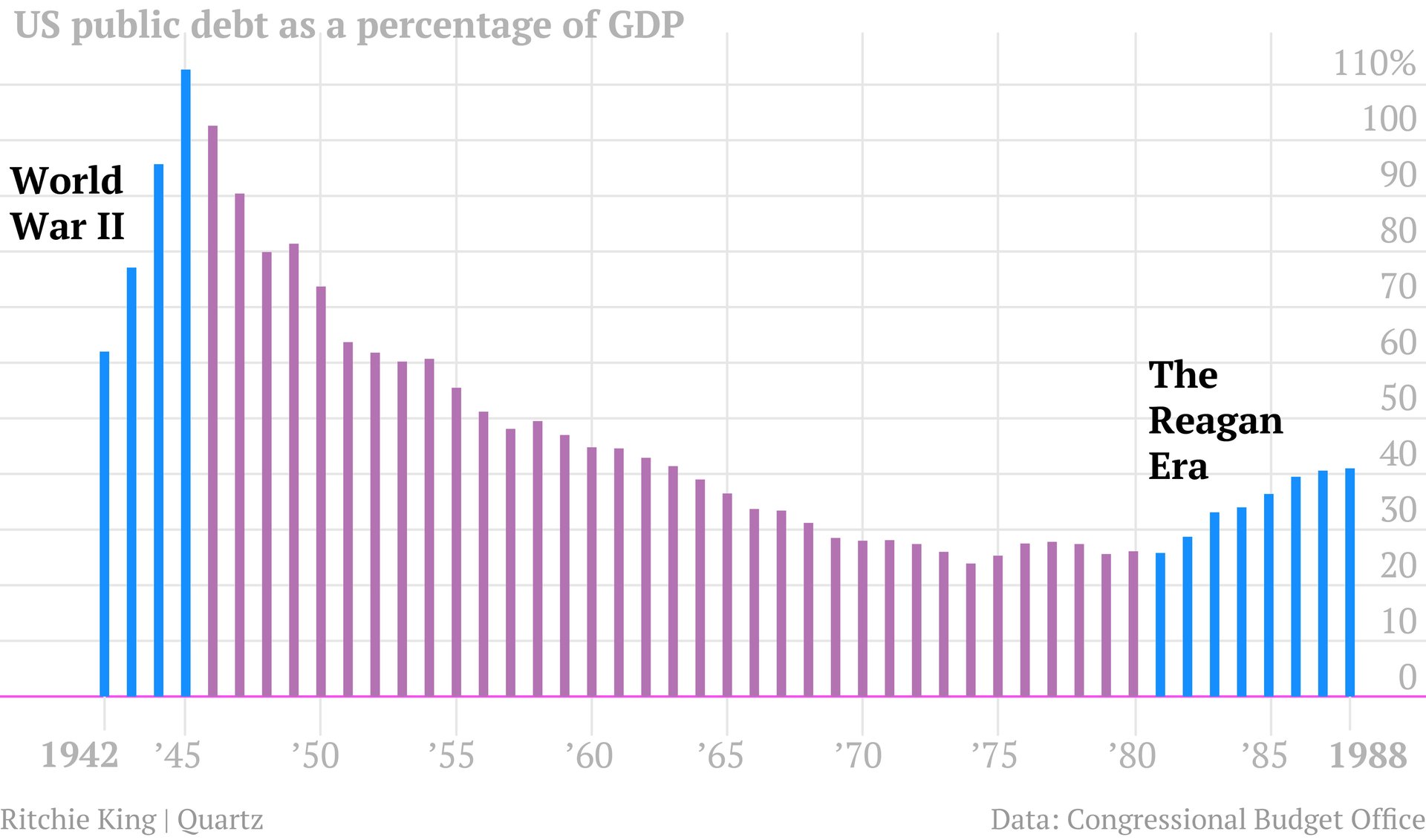

This is really the start of the very familiar political arguments about the role of government spending and economic growth. The chart above shows the relationship between debt and growth. As the size, scope and role of government changed drastically under Franklin D. Roosevelt and his New Deal, the US posted its biggest-ever peacetime debt increase. The debt jumped by 150% from 1930 to 1939, when it was at around $40.44 billion (about $673 billion in today’s money.) At the same time, the economy—the bottom of the formula—collapsed, as did government revenues, which suffered from lower economic activity. The result? A new debt-to-GDP record of 44% in 1934. And this was all before Pearl Harbor.

The debt-to-GDP ratio hit its all-time record of 113% by war’s end. Debt was at $241.86 billion in 1946, about $2.87 trillion in current dollars. Unlike after World War I, the US never really tried to pay down much of the debt it incurred during World War II. Still the debt shrank in significance as the US economy grew. It would take the debt-to-GDP ratio until 1962 just to get back to where the US was before the war. And with some fits and starts the debt load declined until hitting its recent low in 1974 at 24%, when the debt outstanding held by the public was $343.7 billion ($1.61 trillion, in current dollars.)

Debt-to-GDP began another upswing in the early 1980s, when the US fell into a particularly nasty recession, set off by the Federal Reserve under Paul Volcker, who raised interest rates to record heights in order to defeat inflation. Government receipts flattened thanks in part to the large, permanent tax cuts that served as one of the top accomplishments of President Ronald Reagan’s first term. Spending jumped on both defense and social programs. Deficits exploded, breaking with the US tradition of only running large deficits during wartime. Debt-to-GDP began to climb and it hit a postwar peak of more than 49% in the early 1990s. In 1995, the publicly held debt outstanding was about $3.6 trillion (or $5.47 trillion, in today’s money). After that, a surge of economic growth, and increased revenues—thanks in part to the 1990 tax increases that cost the first President George Bush re-election and tax increases pushed through by the Clinton administration —helped bend the trajectory of the debt load back into line.

The debt-load continued to look increasingly manageable throughout the late 1990s, and it hit its recent low of less than 33% of GDP in 2001. At that point, things looked so good on the debt front, that some were projecting the US would be within striking distance of eliminating the entire debt within a decade. It didn’t work out that way.

A recession, combined with tax cuts in 2001 and 2003 championed by President George W. Bush, severely crimped revenue. At the same time, spending surged both on military outlays after Sept. 11 and on domestic programs such as an expensive prescription-drug benefit for senior citizens. As a result. US borrowing shot higher to finance the Bush Administration’s efforts to stabilize the banking system as the economy teetered on the brink in 2008. Total government debt available to be traded publicly rose from $3.41 trillion in December 2000 to $5.80 trillion in December 2008, an increase of 70%; the debt-to-GDP ratio went up from 34.7% in 2000 to 40.5% in 2008.

The great recession was the perfect storm to blow debt-to-GDP ratios skyward. GDP tumbled. That means that even without a spending increase, debt-to-GDP would have jumped sharply. Moreover, government revenues shrank to their lowest level since 1950 — as a percentage of GDP — because business activity declined; that meant that debt levels would have to rise, even without spending increases. And there were indeed spending increases. For instance, in 2009, outlays increased to more than 25% of GDP, the highest level since World War II. That number declined somewhat, to 24.1%, where it rested in both 2010 and 2011. The U.S. started 2012 with $10.48 trillion in publicly traded debt. And by the end of last week, it was $11.42 trillion.

Because on top of the roughly $11.4 trillion in US government debt, which can be bought and sold and is floating around in financial markets, there’s also nearly $5 trillion in debt that the US government owes to itself. Those are largely obligations to the trust funds that are used to pay for programs such as Social Security. These aren’t counted in debt-to-GDP charts published here, and are often excluded from such calculations. But if you did include this debt—and there’s an argument to be made that we should, since the government is on the hook to pay these claims—the US debt-to-GDP ratio was just under 100% at the end of 2011.

So what does that mean? Here’s where we get into some arguments. Some economists say that the empirical record suggests that a debt-to-GDP ratio this high is bad for long-term economic growth because the borrowing costs become a drag on other government spending. Others argue that such observations aren’t that helpful because it isn’t as if large build-ups of debt always come before economic slowdowns. Sometimes large buildups of debt sometimes result from shocks to economic growth—such as massive collapses in the financial system.

Still, many people are looking at Japan as a potential cautionary tale of for the US. Japan suffered its own real-estate bubble, bust, and banking failure in the early 1990s. Its debt-to-GDP has surged to more than 200% in recent years. Back in the mid-1980s, it was around 50%. And for what it’s worth, it’s not as if the Japanese economy shows signs of gathering long-term strength any time soon.