An astonishing decade-long surge of oil prices is reversing, according to a top energy watchdog. The reason is moderate global economic growth and a spike in oil supply from Iraq, Libya and North America.

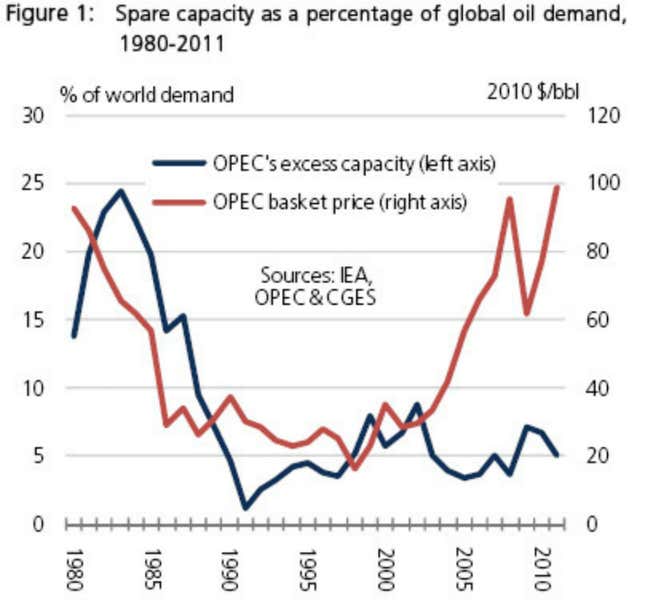

The largest factor in high prices has been the world’s unused capacity to produce oil, what the industry calls “spare capacity.” If you happen to be a chronic buyer of fountain pens, think of oil that way: you will be frequently on edge if the world’s main fountain pen supplier can produce just 1,000 pens a year while demand is 990 and growing; you will offer to pay more for your pen if only you can be guaranteed to get yours. So it has been with oil: for decades, there was plenty of spare oil-production capacity—far exceeding demand. But in 2002 or so, growing demand began to push up against the limits of oil production capacity. Spare capacity became thin, shrinking to just 2 million barrels a day or so, or just 2% of the approximately 85-89 million barrels a day of global demand during the period. Worry-warts pushed oil prices as high as $147 a barrel in the summer of 2008. So the situation remains today, allowing geopolitical crises such as the Arab Spring to push up oil prices as markets worry whether there will be sufficient supply in a pinch. Look at the blue line in this chart, which shows the post-2002 dip in spare capacity (along with a plunge starting in the early 1980s).

But in a new report issued Oct. 12, the International Energy Agency says that spare capacity is set to be restored over the coming five years or so, causing oil prices to fall. The IEA says that global demand will rise to about 95.6 million barrels a day, while production capacity will surge to about 102 million barrels a day, for a comfortable cushion of spare capacity exceeding 6 million barrels a day.

The IEA said that, presuming average GDP growth of 4.3% a year, the world will use much less oil than it previously thought. Meanwhile, new supply will come on line in the US and Iraq, and Libya production will be more reliable.

Because of this shift, the IEA forecasts that Brent benchmark oil prices—used for 70% of the world’s crudes—will fall from an average of $107 a barrel this year to to $89 a barrel by 2017.

But the IEA warns that geopolitical unpredictability will not vanish. Hence prices will also gyrate.