The Chinese central government may be gearing up for its first comprehensive attempt to take control of the trillion-yuan-plus industry around extending off-balance-sheet loans, known as “shadow banking.” And this could have all sorts of destabilizing knock-on effects.

The Chinese central government may be gearing up for its first comprehensive attempt to take control of the trillion-yuan-plus industry around extending off-balance-sheet loans, known as “shadow banking.” And this could have all sorts of destabilizing knock-on effects.

The sign the government wants to act comes in a set of guidelines known as Document No. 107, which was leaked to the Chinese media today (link in Chinese). What they boil down to is that the government wants to clean up debt.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

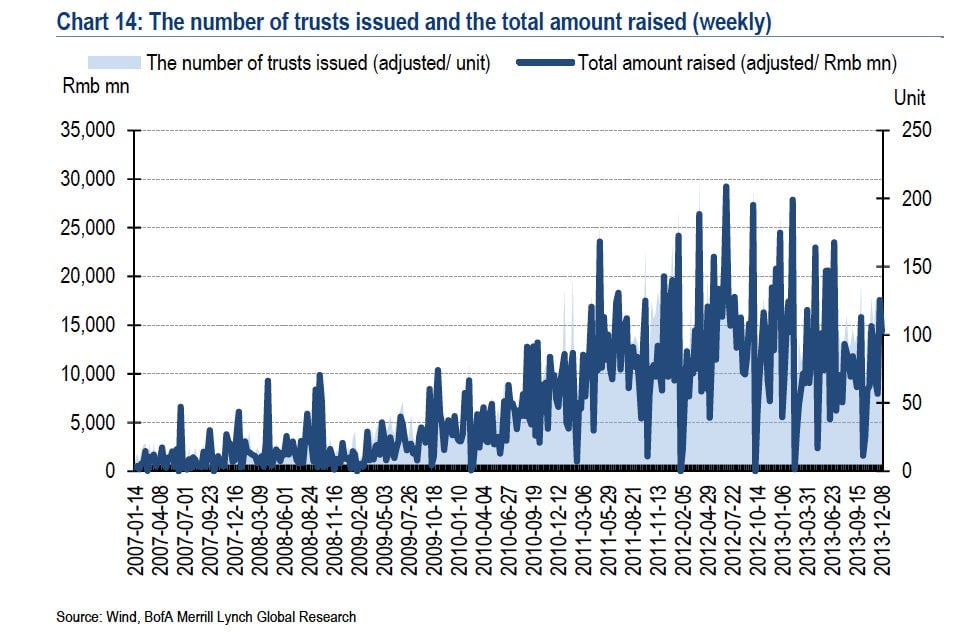

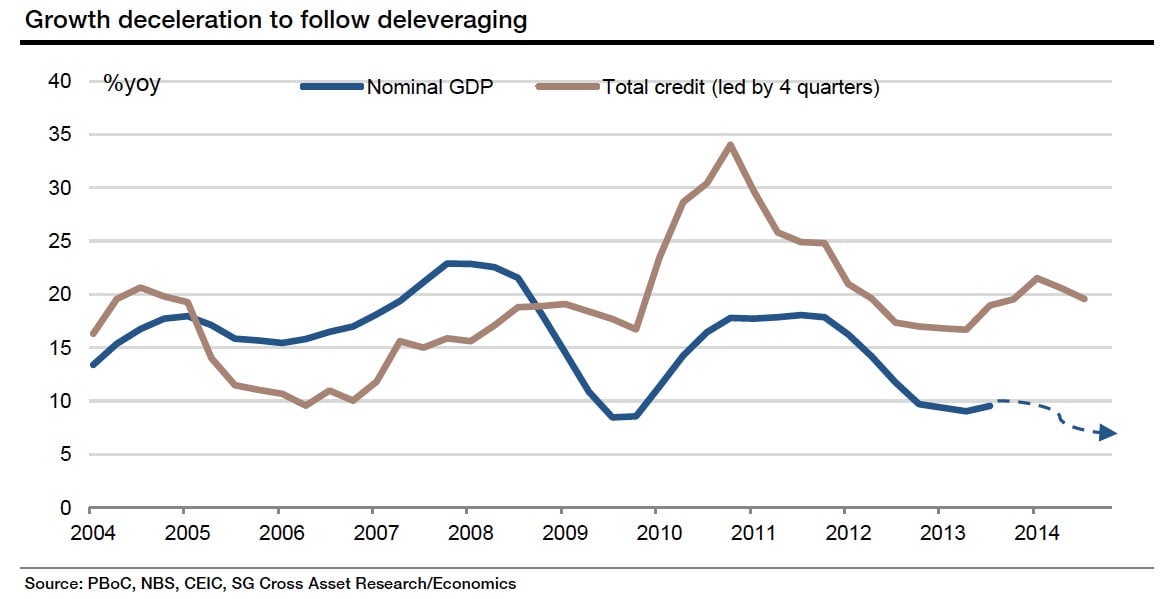

And there’s a lot of debt. The government weathered the global downturn by lending like crazy to juice growth through investment, often in projects that won’t make a return for years, if ever. The slowing economy has left more and more companies insolvent, paying off existing debts with shadow loans (more on that here and here).

Which is why it won’t be easy, argues Wei Yao, an economist with Société Générale. ”This development, if confirmed, [suggests] the central government is (very) serious about deleveraging…,” she writes. “The short-term impact on economic growth will almost certainly be unpleasant.”

Here are some reasons why if the guidelines are implemented, 2014 will likely see a surge in cash crunches and even defaults:

It all comes down to enforcement, however. The banking industry has consistently worked around past government crackdowns on shadow channels.

Plus, Document No. 107 actually applauds shadow banks for their “positive role in serving the real economy and enriching investment channels for ordinary citizens,” as the Financial Times reports (paywall). That hints that it might not want to regulate the industry too heavily, as doing so would crimp growth. If that’s the case, 2014 won’t be much wilder than last year. 2015 though? Absolutely pear-shaped.