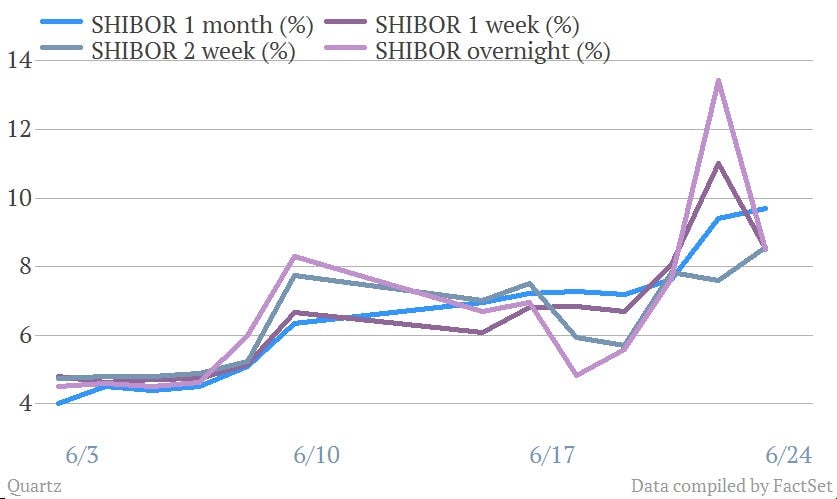

The headlines today were awash with relief that China’s liquidity crisis has subsided, as the central bank, the People’s Bank of China (PBOC), finally came to the aid of banks after a week-long standoff. But it’s hard to look at this chart and see cause for relief:

The headlines today were awash with relief that China’s liquidity crisis has subsided, as the central bank, the People’s Bank of China (PBOC), finally came to the aid of banks after a week-long standoff. But it’s hard to look at this chart and see cause for relief:

“Keep in mind 8-9% is right on the edge of the market breaking down,” says Patrick Chovanec, chief strategist at Silvercrest Asset Management. Even as the overnight rate came down, he notes, the 14-day and 1-month rates spiked today. “It’s kind of like how in Beijing…[the pollution has] been off the charts for so long that when it goes back down to ‘hazardous’ we’re like, ‘Oh, it’s great.'”

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

That’s because the core problem isn’t simply a seize-up in liquidity. Rather, it’s that rolling over the piles of debt amassed over the last few years requires ever-increasing amounts of liqudity, and that’s becoming harder and harder to perpetuate.

“I think what people don’t really grasp is the extent to which this is not a liquidity crisis—it’s a debt crisis, so it’s not something that can go away,” says Anne Steveson-Yang, founder of Beijing-based J Capital Research. “They have a situation now where they’re running the whole economy on debt.”

What that means is that China’s massive stimulus from 2009 to 2011 sunk money into projects that are generating little or no returns. The continuing gush of credit allowed companies to paper over these losses by covering their bad debt with new loans. That combined with the fact that in the last two years, much of those loans haven’t appeared on bank balance sheets, and have instead been issued through shadow lending, has obscured the scale of China’s indebtedness. But whatever the size, it’s now big enough that the system needs colossal amounts of liquidity even to keep above water.

So what can the Chinese government do about this? One thing the PBOC can’t do is use its foreign exchange reserves to bail out the banks. This is often assumed to be an option, but it isn’t. The PBOC’s $3.4 trillion in foreign exchange reserves are denominated in various currencies; selling them for yuan would strengthen the yuan, killing China’s export trade. It would also be massively deflationary, as it would reduce the amount of yuan in circulation. That would worsen the current liquidity squeeze unless balanced by a form of reverse sterilization, like lowering the required reserve ratio (RRR). And that brings us to the next point.

The likeliest tool for increasing liquidity is lowering the required reserve ratio; this would allow banks access to more of their deposit bases. And they’re big—like, $3 trillion big. And many argue that, at around 75%, Chinese banks’ loan-to-deposit ratios are sufficiently healthy to make the move a safe one. By comparison, the US’s eight biggest banks had a combined loan-to-deposit ratio of 84% in Q4 of 2012. Here’s a look at the official data for all Chinese banks:

But this obscures the difference between big banks, whose ratio is somewhere around 70%, and the smaller ones, whose ratios are much higher than the average. That’s not exactly surprising. The big state-owned banks get to collect deposits, which they enjoy at government-set rates that many believe to be artificially low. In order to make money, the regional and commercial banks have to make more—and riskier—loans. And, sure enough, the proportion of loans that are bad is climbing (paywall).

And even assuming banks do have acceptable levels of outstanding lending, untold chunks of it are loans they’re never going to see again. As the Shibor shocks of this and last week suggested, smaller banks need constant fixes of cheap liquidity to prevent them from defaulting on loans. Though big banks are probably somewhat healthier, they’ve been raking it in off shadow lending, too.

So the problem with lowering the RRR is that it would basically rev up the whole cycle of good credit chasing bad all over again. Those loans would also inevitably flow into the property market, driving already stratospheric prices still higher—a major policy worry for the central government right now. Plus, it would eventually gush back into the system, driving up prices for consumers.

In that sense calls for loosening kind of miss the point, as Silvercrest’s Chovanec points out. ”The PBOC isn’t taking away the punch bowl,” he says. “It’s refusing to go get a bigger and bigger punch bowl.”

Even if it was unintentionally severe, the fact that the government has been crackdown on the interbank financing channels showed that government officials are intent on curbing excessive lending sooner. At the same time, a slew of wealth management products mature at the end of the June, which could trigger more interbank mayhem. That might be enough to prompt more loosening.

But even if the PBOC does pump money back into the system, it might not matter, says J Capital’s Stevenson-Yang, since big banks are too spooked to lend to smaller ones. “It will be calm now for a week or two and then there will be another shock—and a pretty big one,” she says. “It could be capital flight, or really bad trade numbers. But you’re going to hear the great sucking sound of money leaving China.”