When the People’s Bank of China (PBOC) recently began clamping down on unruly banks, the assumption was that the PBOC was intentionally cutting off liquidity to teach banks a lesson. But it’s entirely possible that the central bank’s actions were merely a shot in the dark.

When the People’s Bank of China (PBOC) recently began clamping down on unruly banks, the assumption was that the PBOC was intentionally cutting off liquidity to teach banks a lesson. But it’s entirely possible that the central bank’s actions were merely a shot in the dark.

Here’s why: Much of what’s traded on the interbank market are trust funds and wealth management products (WMPs) that “never appear on anyone’s balance sheet,” says Anne Stevenson-Yang, founder of J Capital Research, a Beijing-based research firm. ”Every single bank is a net lender. The regulators don’t really know how much credit is out there. And that’s pretty dangerous.”

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

For that reason, both the PBOC and the banking regulator have for years been trying to rein in wealth management products and, more recently, the interbank market. But only at a very gradual pace. That is, until the PBOC’s foreign currency arm cracked down on the use of bank credit letters for use in WMPs, which set off the calamitous contraction in liquidity.

It could be that the PBOC didn’t realize that plugging up capital inflows would trigger a liquidity crisis, which would also imply that it didn’t know how much off-balance sheet lending was taking place. The PBOC obviously realized there was a problem, but its lack of clarity in the last week suggests that it didn’t anticipate the scale of it.

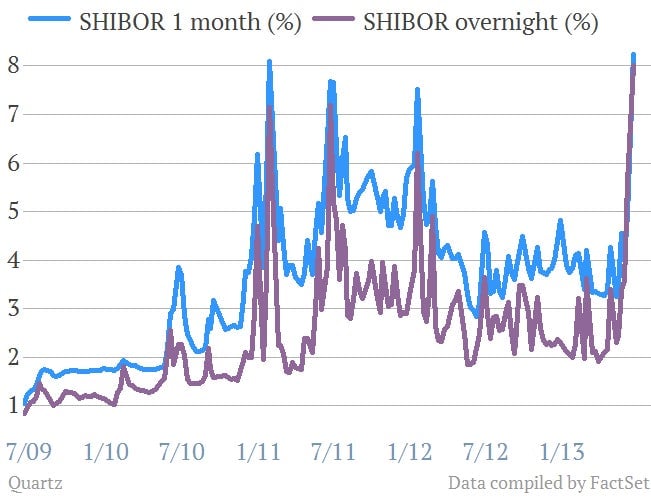

And, in case you needed reminding, the scale is big:

Interbank rates might have come down for the moment, but they’ll have to come down a whole lot more for things to return to normal. And that could take a while. “Every big company is incredibly dependent on credit,” says Stevenson-Yang. “We got over the one big bump. But when you have a Shibor hanging around at 8% it means costs are going up across all the debt instruments in society.”