Berkshire Hathaway shareholders this weekend voted down a proposal that would have prodded Warren Buffett’s conglomerate to pay a dividend. It’s no wonder.

For one thing, Buffett himself controls a hefty chunk of the shareholder voting power. “Now, you may think that I stuffed the ballot box,” he said during the question-and-answer session at this weekend’s shareholder meeting, the New York Times reported. “I did.”

But the other reason that shareholders squelched the proposal is simply because they trust Buffett, the world’s most accomplished investor, to put their money to good use. That’s why they gave it to him in the first place. They don’t want it back.

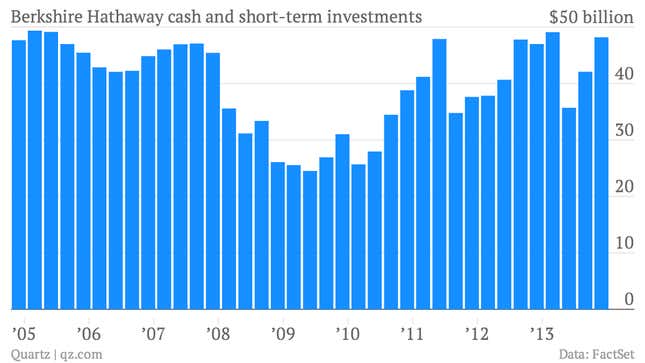

On the other hand, they don’t want it just sitting in Berkshire’s bank account either. And finding a productive place to put all that money is no easy matter. Berkshire Hathaway’s cash hoard has surged 30%, to more than $48 billion, since the end of 2011.

You can see from the chart above that Berkshire’s cash pile has returned to heights not seen since before a notable decline during the worst of the Great Recession starting around 2008. And that’s just classic Buffett.

During the market meltdown and recession of that period Buffett was buying, using cash to help make a spate of giant deals. He gobbled up preferred shares in blue chips like Goldman Sachs and General Electric. He made Berkshire’s largest ever acquisition, the $26.7 billion purchase of the Burlington Northern Santa Fe railroad.

Those deals were enabled by the fact that Berkshire had an ample supply of dry powder. ”It’s been an ideal period for investors: a climate of fear is their best friend,” Buffett wrote in his annual shareholder letter recounting the story of 2009, when the company’s cash balances fluttered around recent lows of around $26 billion.

A similar dip in Berkshire’s cash came in late 2011, as the company announced large investments in chemical maker Lubrizol and Bank of America. And the cash pile shrank in early 2013, as Berkshire bought American ketchup giant Heinz.

But as the mood of the financial markets improved in recent years, it’s been tougher to find the bargains that are the foundation of Buffett’s value investing strategy. (Value investors emphasize buying assets that are significantly undervalued because of market conditions, and then holding those investments for long periods of time.)

Buffett has said that the company will maintain a cash cushion of about $20 billion. Cash in excess of that amount is available for acquisitions. Investors would be silly to force Berkshire to give that cash back now. Buffett is merely rebuilding his supply of dry powder and waiting for the buying opportunity the market might offer. And as long as the 83-year-old Buffett is in charge at Berkshire, shareholders should be patient too.