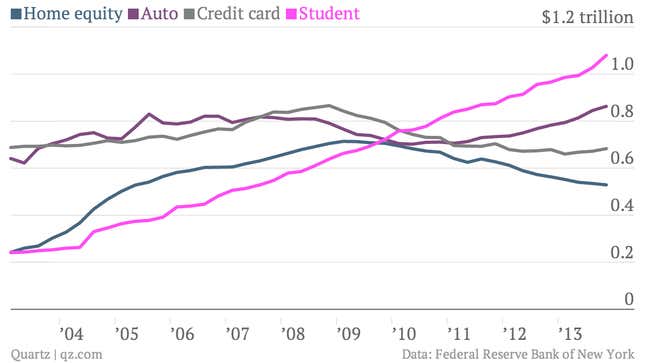

As we all know, US student debt is soaring. With a relentless rise, student debt has become the second-highest form of consumer debt in the US in recent years. In the fourth quarter, the amount of student debt outstanding hit $1.1 trillion. (This chart doesn’t show mortgage debt, which is about a dozen times as big.) But at the same time , there’s a crucial transformation going on. That’s why this chart, below, is important. It shows more people have been availing of a couple of different federal programs that lower the monthly repayments on student loans. The income-based repayment program (IBR) was instituted by the US Department of Education in 2009. It caps monthly loan payments at 15% of the borrower’s discretionary income and forgives loans after 25 years. A separate repayment plan, known as pay-as-you-earn (PAYE), was introduced in December 2012. It is aimed at helping young Americans who graduated into the miserable economy of the Great Recession. (It is only available to those who took out their first loan after Oct. 1, 2007.) It caps monthly payments at 10% of discretionary income and forgives loans after 20 years.

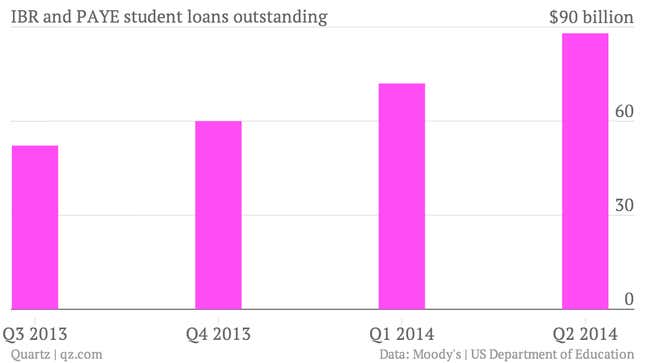

People seem to think these programs are a good deal, as usage of them is growing fast. In a report, analysts from Moody’s noted that the balance of all federal direct loans in repayment—which includes loans that are in forbearance and deferment—under these two programs was about 20% as of the end of March. That’s up from 14% in June 2013.

Some seem strangely horrified by the increase in so-called debt forgiveness plans. It’s true that nobody knows exactly how much these programs will cost the federal government in the end, nor how much of a benefit they’ll deliver to borrowers and the economy at large. (Wonks from the Brookings Institution estimate that the PAYE program could cost the government $14 billion a year.)

But we do know it will make a higher education more affordable to a lot of people. Under one example provided in a White House explainer, a nurse who has $60,000 in federal student loans and earns $45,000 a year would see her monthly payment fall from $690 to $358 under the income-based repayment program. That’s huge.

It seems to be the debt-forgiveness component of these repayment plans that offends the sensibilities of some critics. And it is important that the program doesn’t just become another excuse for colleges and universities to continue to jack up tuition costs, get students to take on more debt and then leave the federal government holding the bag. President Obama’s most recent budget proposed good changes, such as caps to the amount of debt forgiveness. They seem sensible, as many of those with the largest debt loads, such as doctors and lawyers, also have some of the highest incomes. (Republicans are predictably fighting that tweak.)

But there’s an implicit false choice to the framing critics are using, as if the US government would be newly putting itself at risk in the market for student debt, if people don’t pay their loans. The fact is, that train left the station long ago; the government already guarantees roughly 90% of student debt in the US. Even the loans made by private lenders in the now-defunct Federal Family Education Loan program were guaranteed by the government.

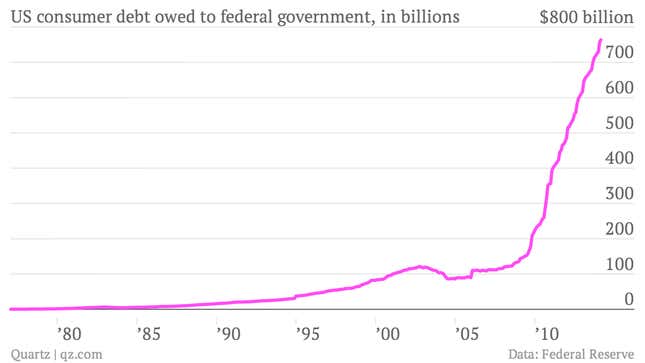

That program was axed in July 2010, as it essentially amounted to a giveaway to banks, who were paid a subsidy to make risk-free, government-guaranteed loans. Since then, the government has done almost all the new student lending directly. That’s why the amount of consumer debt owed to the federal government has gone vertical in recent years. But again, the US government is already on the hook for hundreds of billions of dollars in student debt. That means when students fall behind on payments or stop paying all together, the taxpayer loses. Therefore government programs that help keep student borrowers current for longer period of time, should be a good thing for the government.That’s why income-based repayment plans make sense. (In fact, borrowers end up paying more interest to the government by stretching out the amount of time it takes to repay the loan.)

More broadly the shift toward income-based repayment of student debt is an important, radically sensible and long-overdue move in the US. And it could have real benefits for the economy as a whole, as research indicates that unaffordable student debt loads represent a real burden for young consumers, keeping them from spending on the big items such as cars and houses that are so crucial to US economic growth.