The proposition is simple: Install a device in your car and allow your insurance company to monitor your driving—how fast you drive, how hard you brake, how sharply you corner, and so on. In exchange, it will give you a discount on your premiums.

The proposition is simple: Install a device in your car and allow your insurance company to monitor your driving—how fast you drive, how hard you brake, how sharply you corner, and so on. In exchange, it will give you a discount on your premiums.

That might sound alarming, but it shouldn’t be surprising. Considering internet users already happily trade data on every online move they make in exchange for free services, the only surprise is tracking-based insurance isn’t already more widespread. Progressive $PGR Insurance, the biggest such insurer in the United States, says it found that

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

After analysis of billions of miles in driving data, Progressive has found that key driving behaviors—like actual miles driven, braking, and time of day of driving—carry more than twice the predictive power of traditional insurance rating variables, like a driver’s age, gender and the year, make and model of the insured vehicle.

The average discount on premiums for a Progressive customer who agrees to be tracked is between 10% and 15%.

In future, if you don’t agree to be tracked, you may not only pay higher premiums; perhaps you won’t even be eligible for insurance from most companies. It could be like having a shady credit history, or failing to provide the basic “know-your-customer” information required to open a bank account. “In the end, serving the ‘naysayers’ may become a specialty market niche for some carriers,” suggests a recent report (pdf) on usage-base insurance programs from Deloitte.

For “specialty market niche,” read: very expensive.

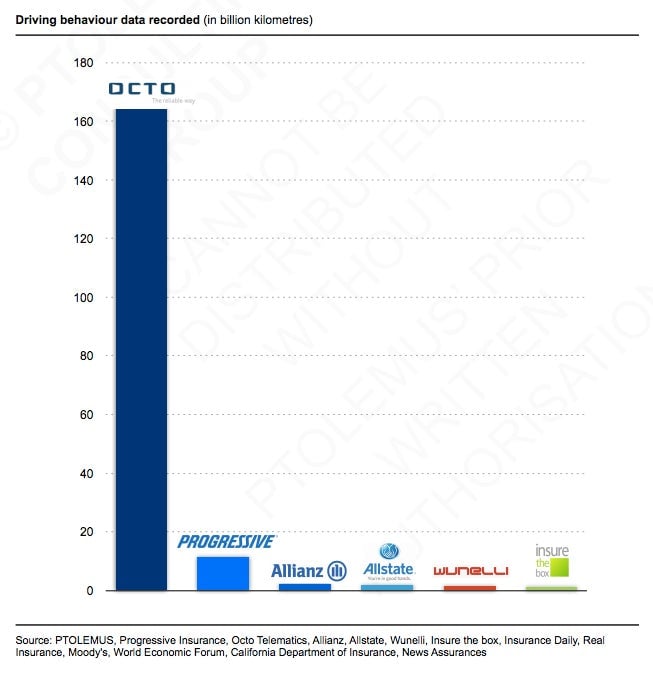

Usage-based insurance (UBI) or telematics-based insurance is not new. One of the oldest companies in the business, Octo Telematics, has been around since 2002. But the idea has never really taken off (though Octo has flourished, and was recently acquired by a large Russian business conglomerate). In the US, Progressive has signed up some 2 million customers to its program since 2008. But there are more than 250 million vehicles on the road, according to IHS Automotive, a research firm.

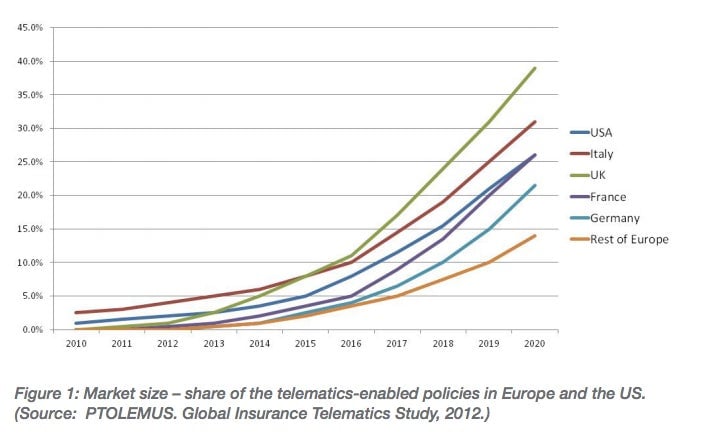

Italy and the United Kingdom have been more enthusiastic adopters; between 15% and 18% of insurance policies there are telematics-based, according to Deloitte. Ptolemus, another consultancy, has lower estimates, but forecasts (pdf) that nearly 40% of British policies will include telematics by 2020.

But a big change may be about to happen, says John Lucker of Deloitte. Telematics-based insurance could finally gain traction, he says, because instead of requiring physical devices that must be manually installed in a car, it can now be done through mobile-phone apps that are much easier to download and install.

An app is less cumbersome for the customer than climbing under the dashboard and fiddling around. It’s cheaper for the company: A telematics device can cost around $100, and it may need to be retrieved and recycled to another customer if the contract ends. Finally, phones are made for communications, while in-car devices need a separate transmitter of some sort. In the UK, a company called Marmalade already sells an app-based insurance product for young motorists who are learning to drive on their family car.

But telematics does involve a big leap for insurance companies. Auto insurance has historically been based on group proxies. Young men drive more hazardously than young women (though gender-based prices are illegal in some parts of the world). Young people are worse drivers than older people. People who drive certain types of sports cars are riskier than those with grandpa cars. And so on. Yet those remain broad-brush categories. “The ability to get down to how drivers drive is a bit of a holy grail for companies,” says Lucker.

Not all insurance companies will benefit from the change. It takes several billion hours of driving data and up to five years of running a UBI program before insurers can extract meaning from the data. Progressive, for instance, has collected over 10 billion miles of data from 2 million vehicles over the past six years.

Bigger firms with lots of customers may be able to gather those data. But smaller ones cannot hope to compete. They will have to pool their data, suggests Chuck Chamness, the head of the National Association of Mutual Insurance Companies, whose members command half of all car and home insurance premiums paid in the United States.

On the other hand, perhaps smaller firms will simply focus their energies on becoming the insurer of choice for people uninterested in telematics-based policies. But they may struggle to compete on price with rivals who benefit from richer data. Or they may find that the customers who shun telematics do so not because of high-minded privacy concerns, but because what the sensors record about their driving would give underwriters fits.

Whatever the outcome for the insurance industry, if telematics-based insurance does take off, it could mean big changes for road safety. Your insurance app might alert you when you brake too hard or drive too fast, and tame your driving. Somewhat more creepily, people may drive more carefully simply because they know they are being monitored. Higher premiums would punish recklessness.

Insurers may also start providing ”value-added services,” Deloitte says, like location-based ads or shopping suggestions. (For “value-added,” read: the advertiser gets the value.) Not everyone will like those, but again, as the internet has shown, people are willing to put up with a lot of noise in exchange for discounts and freebies.

And car insurance may be just the beginning. According to the Deloitte report, ”Before too long the use of sensory technologies that permit behavioral underwriting by insurers is likely to be expanded beyond auto insurance into homeowners, life and health coverages, and perhaps even non-auto commercial lines as well, such as workers’ compensation.” Your whole life could become an exercise in keeping your premiums down—safer and cheaper, to be sure, but a lot less exciting.