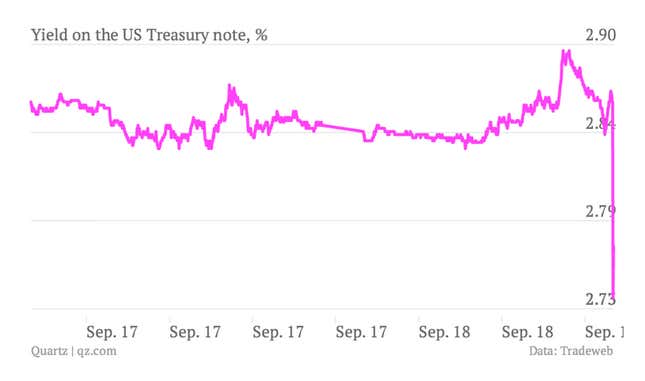

The minutes of the most recent Federal Open Market Committee meeting in September are out. In case you’re not hip to Fed pow wows, that was the get-together in which the Fed’s monetary policy-making body decided not to cut down (or taper, in Fed parlance) its purchases of US government bonds and packages of mortgages. As we pointed out at the time, the markets freaked. But anyway, the markets found themselves pretty much completely unprepared for the Fed’s decision. And as a result, buyers surged back into the US government debt market, buying bonds and pushing yields—which always move in the opposite direction of bond prices—sharply lower. Here’s what the immediate reaction looked like:

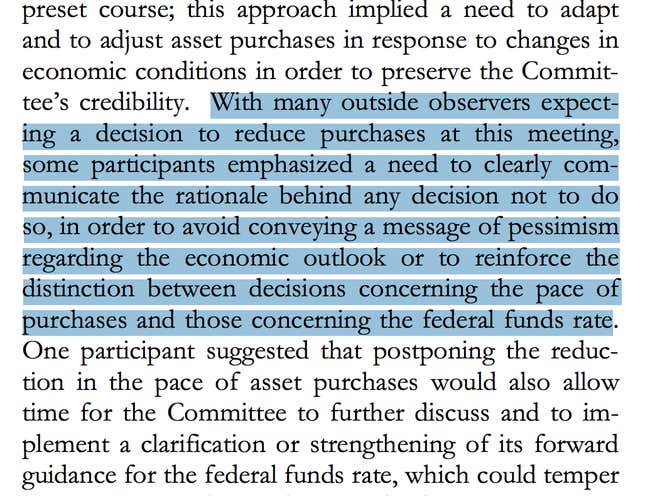

And, as we know from today’s meeting, Fed officials had a feeling that the markets would throw a tantrum if it held onto its bond-buying program weeks of hinting that it would taper. For instance, the camp within the Fed that wanted to hold off on the taper had this to say:

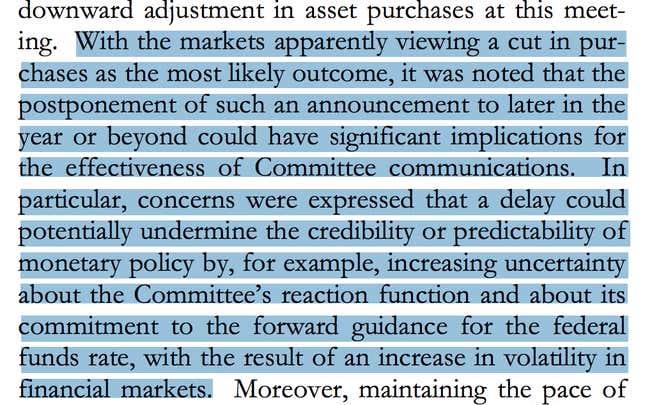

Those in favor of tapering argued that not doing so would risk damaging the central bank’s credibility:

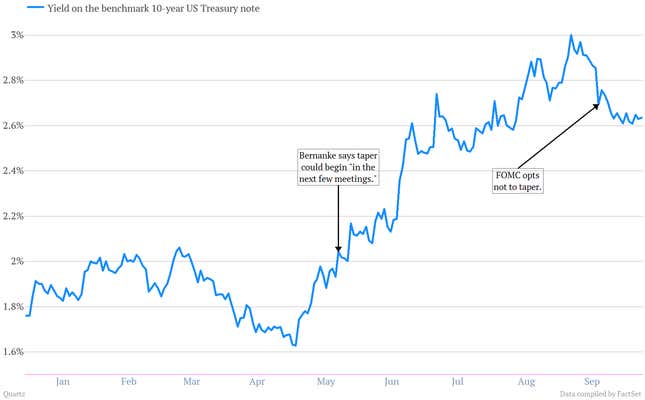

As we now know, the Fed decided to postpone tapering and the markets reacted sharply. But it’s worth noting that markets haven’t fallen that far since the non-taper decision. Here’s a look at the yield on the US 10-year note, with a few annotations. If the Fed was hoping rates would fall back to their pre-taper-hinting levels, it’s surely disappointed. If that’s the case, it might be because the markets have grown leery of taking their cues from the Bernanke Fed.