There’s a dearth of cheap living space in the US: the supply of homes costing less than $198,000 fell 17% in June compared to 2013, leaving first-time buyers hung out to dry.

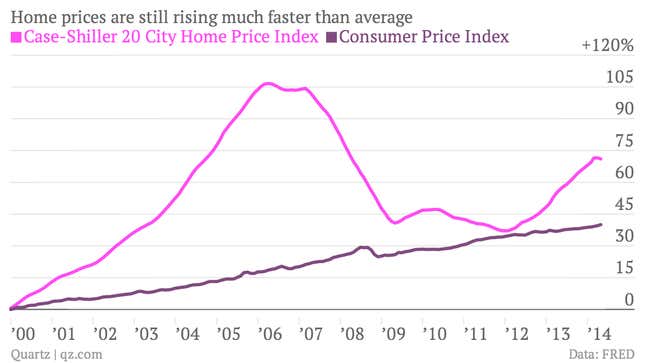

It’s not that inventory for sale isn’t growing—it is, but only on the high-end side. Cheaper homes are being snapped up by deep-pocketed investors to rent, or their current owners are still owe more on their mortgages than their homes are worth, and don’t want to take a loss on a sale. Meanwhile, home prices are still increasing—which isn’t an accident, thanks to subsidies to homeowners and restrictive building regulations:

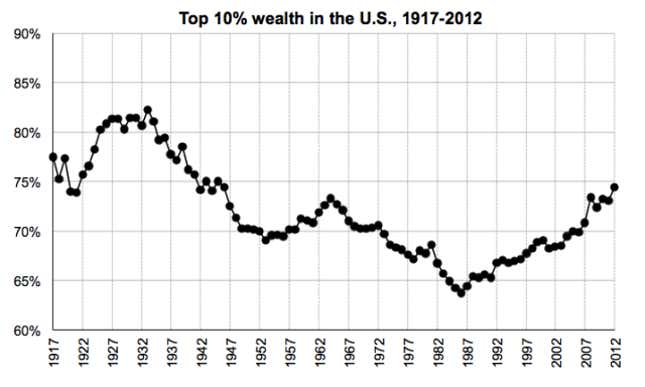

The broader consequences of rising prices can be seen in Thomas Piketty’s research into inequality in wealthy countries. One major contribution of Piketty and his collaborators has been compiling data about the quantity and quality of capital—goods, buildings, financial securities, etc.—in these economies, and how it relates to income. His most controversial finding is that more and more capital is accumulating in the hands of a minority of citizens. Though some have used experimental data-sets to challenge his results, it does seem clear that wealth inequality is at best stagnant and likely worsening. In the US, for instance (pdf), the wealthiest 10% of Americans own about 75% of private capital:

This is especially problematic because Piketty believes the role of capital in the economy will only grow, and that the return on capital will remain higher than economic growth, exacerbating the concentration of wealth in few hands. You’ve probably seen this expressed as “R>G”. But this theory only makes sense if it’s easy to substitute capital for labor; otherwise, the increasingly scarce supply of labor will become more and more valuable. And in the eight wealthy economies Piketty’s research focuses on, several decades of increases in both capital income and the ratio of capital to income can only explained if capital and labor are easy to substitute for one another.

There are plenty of criticisms of this idea, with many of the most incisive (pdf) from Matt Rognlie, an economics scholar at MIT. His primary concern is that Piketty isn’t taking into account the fact that capital depreciates over time, which helps preserve the value of labor—once you build a house, for instance, someone has to clean it, repair it and repaint it, or it will fall into ruin.

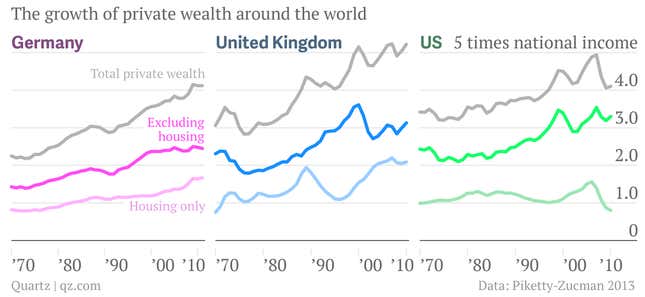

Rognlie has an important empirical point as well: When you look at the actual stuff that makes up all the capital Piketty and his collaborator Gabriel Zucman measured, you discover that a lot of it is housing. In the eight countries in Piketty’s dataset, the increase in the value of housing capital made up 80% of the overall growth in the ratio of domestic capital to income between 1970 and 2010. You can see a rough approximation of this effect by looking at trends in private wealth in these three countries:

When you take housing out of the equation, the increase in capital in recent decades is much smaller—in fact, it is small enough to suggest that capital isn’t an easy substitute for labor, and that diminishing returns on capital mean that R>G isn’t true, and the wealthy won’t just keep getting wealthier. Piketty, in this telling, is tricked by the housing booms in many wealthy economies.

And yet: Rising housing prices have real consequences that people have to live with—just ask the first-time US home-buyers—and returns on real estate investments are meaningful. The explanation for the huge increases in housing prices isn’t embedded in the buildings, but in land.

First, cities have become increasingly important economic hub. The old adage “location, location, location” is still important, and it’s one reason for the UK’s massive property boom, centered on London. Second, regulations on urban land use have prevented the supply of housing from keeping up with demand. That’s one reason San Francisco has wildly high home prices. It’s also why reducing restrictions on land use made our list of ten ways to fight inequality.

But despite the 2008 crash, there’s no sign that home price increases are slowing, and, along with it, growth in capital. Even Rognlie concedes that Piketty could be right about capital taking over even as he is wrong about the specific mechanism. ”The story about the increasing role of capital could be right, but it’s this weird, inverse image,” he told Quartz in June. ”Scarcity of housing will continue to go up, and land it sits on will start claiming a larger and larger share of our resources.”

In other words, housing will eat the economy—everybody needs it, but it will be worth more and more, and land-owners will be the capitalists in command, unless we do a better job increasing the supply of housing.