The Bank of England raised interest rates for the first time in a decade, and it’s not happy about it

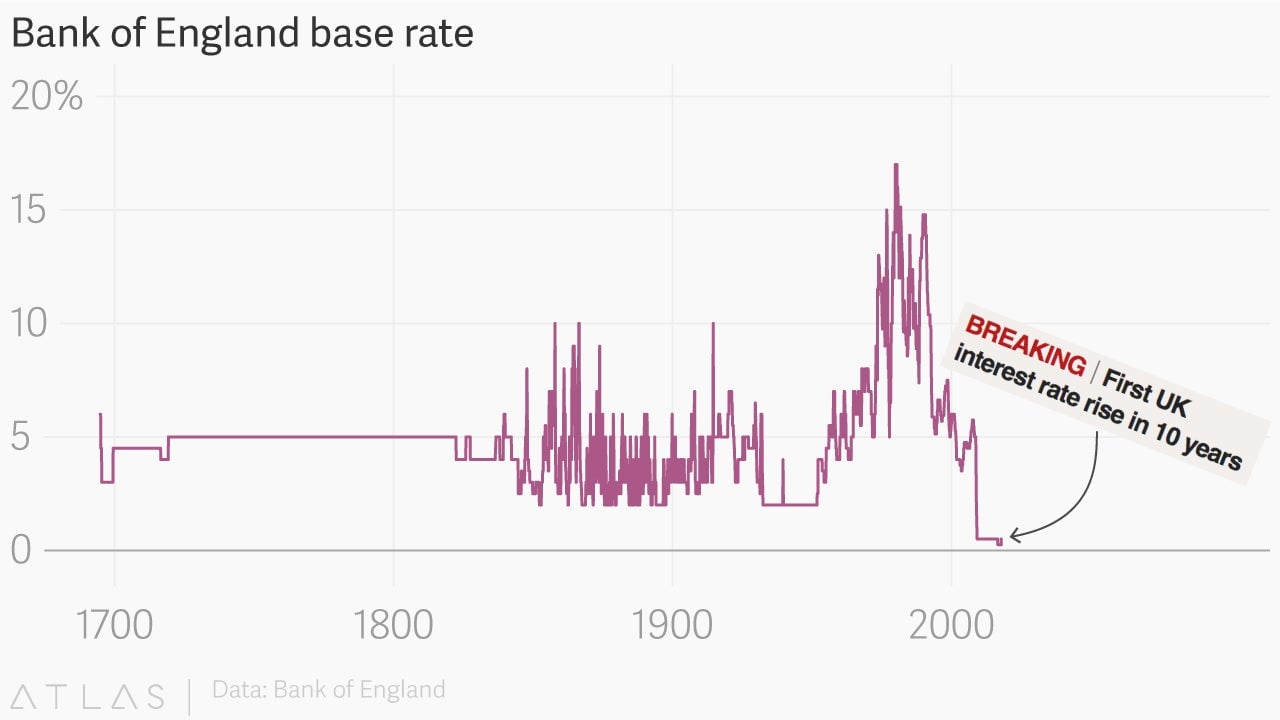

For more than a decade, the UK economy was deemed too weak to withstand an increase in interest rates. Today, for the first time since July 2007, the Bank of England hiked its benchmark rate (pdf) up from an all-time low. (The bank was founded in the late 1600s, so that covers a long time.)

For more than a decade, the UK economy was deemed too weak to withstand an increase in interest rates. Today, for the first time since July 2007, the Bank of England hiked its benchmark rate (pdf) up from an all-time low. (The bank was founded in the late 1600s, so that covers a long time.)

This doesn’t mark the start of a rate-hike cycle, like the one the US. The UK’s vote to leave the European Union last year put the central bank in a tight spot. Today’s rate hike—from 0.25% to 0.5%—does little more than reverse the cut in August 2016, in the immediate aftermath of the EU referendum that officials feared would lead to a recession. The economy has proven more resilient than feared, but has clearly weakened.

The essential business news, delivered fresh every morning.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.