The search for income is getting harder, and there’s no shortage of suggestions on where to get a little bit more. But what about the cost? We think that focusing on creating a better return sequence can help investors access more efficient income.

The baby boomer generation continues to move from its peak earning years into the retirement phase. As it does, it’s become much more income hungry. This appetite is having a big impact on the demand for income-generating allocations. In target-date solutions, for instance, bond allocations for peak earners are typically in single-digit percentages; for retirement-age investors, bonds can make up as much as half of their overall portfolio.

But the search for income is a challenge today, and isn’t getting any easier. More and more baby boomers will be demanding income-generating bonds, and the income from those bonds is now lower, thanks to years of Federal Reserve quantitative easing, which has shrunk the market and reduced yields.

At the same time, risks inside income-oriented indices are rising. The duration, or interest-rate sensitivity, of bond indices has grown by 30% since 2008. And with the US late in the credit cycle, credit quality is declining. On the equity side, dividend-paying stocks, based on price-to-earnings ratios, are trading at a valuation of 24.8 times earnings.

There’s no shortage of ideas and suggestions on where to squeeze out a little more income today, but there’s not much talk about the cost of that extra income. Many of the areas that people point to for an income boost face large drawdowns if things go wrong. Preferred stocks are a good example: over the past 10 years, the average drawdown in Morningstar’s Preferred Stock category was 8%, and the biggest was about 44%.

It’s clear that simply piling into higher-income trades isn’t the answer.

The logical question is: What’s the perfect income-generating solution?

The answer is… it depends. First and foremost, to identify the best solution, every investor has to determine the appropriate trade-off between generating income and the potential principal cost from losses. That’s because staying the course is by far the most important element.

Other factors matter, too. Taxes are often part of the equation, so you’ll have to decide how important pre-tax income is versus after-tax income. Inflation is a consideration, and so is liquidity—how accessible do you want your savings to be as they generate income? And in today’s world, the income/growth mix is key: do you want pure income or income with an option for capital growth?

The “perfect” income solution doesn’t live on an island—it has to be considered in the context of its role in a broader portfolio.

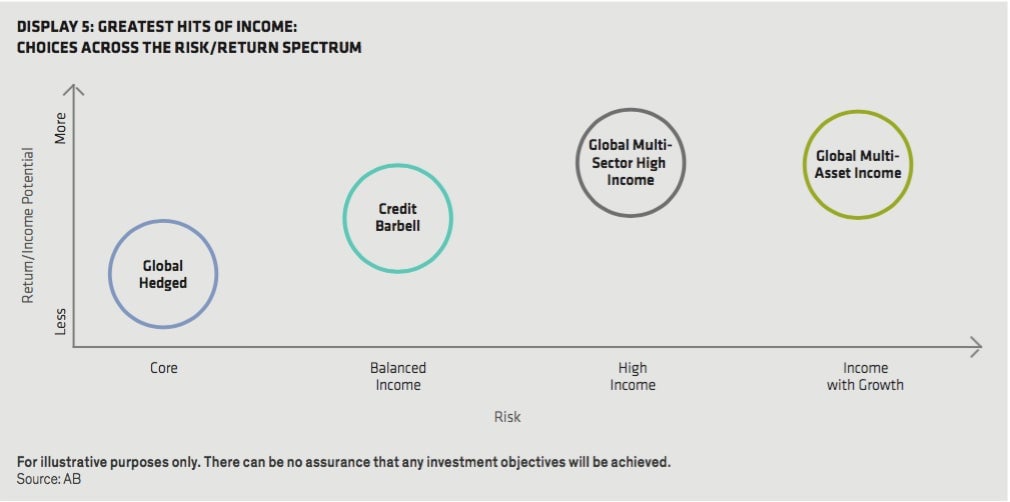

We see four key roles for income: core, balanced income, high income and income with growth. Here are our suggested “greatest hits” solutions for each:

So there’s a lot of flexibility in creating income solutions to fill diverse roles in investors’ portfolios. But good design is critical. Simply investing in broad indices or bolting together different components is inefficient—and can leave portfolios vulnerable to unintended risks.

Well-designed income solutions should reflect the principles of building a better path, with a sequence of returns that aligns with investors’ specific goals and risk tolerances. That requires accessing better beta sources and combining them in more efficient ways. It also means using active management to target higher-probability alpha opportunities and manage risk.

This article was produced by AB and not by the Quartz editorial staff.

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams.