Some time before November, when the major annual Communist Party meeting is convened, the Chinese central government will announce the amount of debt taken on by local governments. No one knows what that amount will be, but preliminary findings were ugly. Standard Chartered now estimates that it will total around 24.4 trillion yuan ($3.95 trillion), reports FT Alphaville (registration required). It isn’t the size of the debt that’s worrying so much as the proportion of it that local governments can’t pay—particularly given that more than half is owed to publicly-listed commercial banks, according to Ting Lu of BofA/Merrill Lynch.

Some time before November, when the major annual Communist Party meeting is convened, the Chinese central government will announce the amount of debt taken on by local governments. No one knows what that amount will be, but preliminary findings were ugly. Standard Chartered now estimates that it will total around 24.4 trillion yuan ($3.95 trillion), reports FT Alphaville (registration required). It isn’t the size of the debt that’s worrying so much as the proportion of it that local governments can’t pay—particularly given that more than half is owed to publicly-listed commercial banks, according to Ting Lu of BofA/Merrill Lynch.

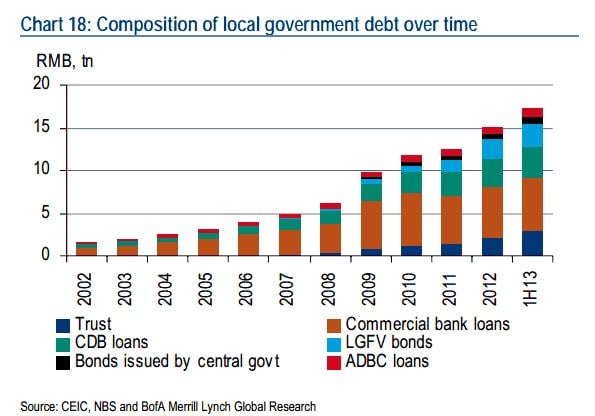

But here’s one way the government is helping free commercial banks of this (probably) toxic debt: It’s getting China Development Bank, (CDB), China’s biggest government-backed bank, to buy them off commercial banks. As Lu flags, local government loans from CDB have climbed steadily, totaling 3.6 trillion yuan at then end of June. Here’s a look:

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

CDB’s role is curious. By asset value, CDB is the world’s most powerful policy bank. The World Bank had $313.9 billion in total assets at last count. CDB’s assets come in at $1.22 trillion. It’s also China’s largest bond issuer in Hong Kong. And because it’s basically sovereign debt, its bonds are considered incredibly solid—CDB ranked 27th on Global Finance Magazine’s “World’s Safest Banks” list, ahead of BNY Mellon.

Loaning to local government infrastructure projects has long been among CDB’s mandates, but what’s interesting is how much the CDB has been lending for those projects lately. Until recently, its portfolio was increasingly commercial. Last year, CDB loaned e-commerce giant Alibaba $2 billion, financing the bulk of the Hong Kong stock exchange’s purchase of the London Metal Exchange a few months later.

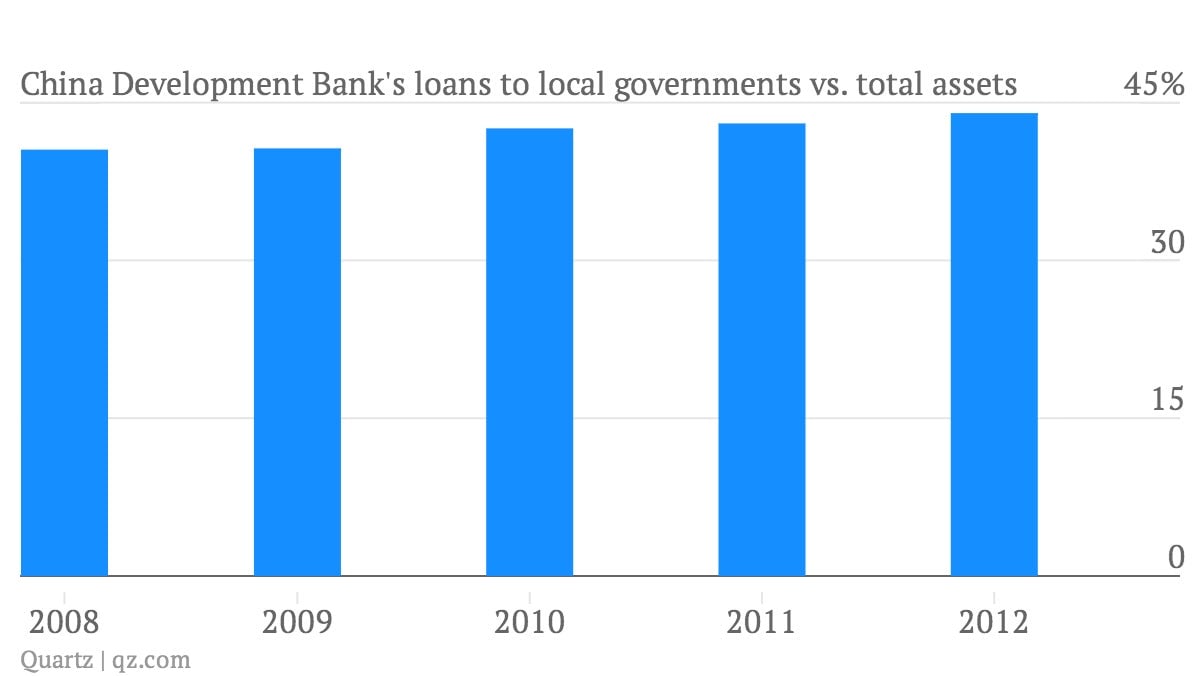

No longer. CDB has been increasingly been restructuring short-term debt that local governments owe to commercial banks, issuing long-term loans of its own, as Fraser Howie and Carl Walter, two experts on China’s financial system, highlighted earlier this year (paywall). And as the Wall Street Journal recently pointed out, CDB’s been forgoing deals like the $8 billion that Alibaba took out in May, which included refinancing of CDB’s existing loan, and the purchase of Smithfield Foods by Chinese pork giant Shuanghui International Holdings. The data bear out this shift in focus:

CDB’s restructuring of local government debt might help reduce shadow lending, much of which is taken out to cover short-term loans for long-term projects that aren’t making money. That might help reduce the risk to China’s financial system.

But it doesn’t do much to solve the problem of China’s credit addiction. Chinese commercial banks own a good chunk of CDB’s bonds. Normally a commercial bank would make more money lending at a higher interest rate than it would holding CDB bonds. The banking regulator compensates for this by allowing them to treat CDB’s bonds as zero-risk, meaning they don’t have to set aside capital against those investments. However, if a commercial bank’s investment in CDB debt ends up funding the purchase of that bank’s own non-performing loans, that bank will have more money to lend out.

Meanwhile, CDB’s central government guarantee means it can borrow on the cheap from Chinese commercial banks and, increasingly, international investors (ratings agencies rate its debt the same as sovereign debt). In essence, it passes artificially low borrowing costs on to local governments in the form of new loans. And that creates one more reason for local governments to continue blindly spending on valueless projects.