At this month’s 2018 Summit of the Forum on China Africa Cooperation, the cornerstone of China’s investment and lending on the continent, Beijing made a pledge of $60 billion in investment, just like the previous edition.

At this month’s 2018 Summit of the Forum on China Africa Cooperation, the cornerstone of China’s investment and lending on the continent, Beijing made a pledge of $60 billion in investment, just like the previous edition.

It appears, however, that we are in a new phase of Chinese financing. A combination of domestic and international pressures is altering China’s extensive lending program—and African states that have relied on this lifeline must adjust. The new reality could benefit African countries by compelling improved project preparation and implementation, reducing price inflation, and decreasing the role of political over economic considerations in project selection.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

At the last summit, in 2015, China also announced a $60 billion package for Africa comprised of $35 billion in preferential loans and export credit lines, $5 billion in grants, $15 billion of capital for the China-Africa Development Fund, and $5 billion in loans for the development of African small-and-medium enterprises. While the announced $60 billion package seems to be same as the last, there are noticeable differences.

It looks like China is responding to the debt situation in Africa by increasing the portion of the package covering no-interest loans, grants and concessional loans to $15 billion. The government portion of the packages is also smaller. As Lina Benabdallah, assistant professor of politics and international affairs at Wake Forest University, explains, “Of the $60 billion pledged, $10 billion is labelled ‘investments in the next three years,’ which means that Chinese companies—not the Chinese government—are likely to fulfill those investments.”

Between the 1970s and into the 1990s, developing countries’ debt compounded at an annual average of roughly 20 percent, rising from $300 billion to $1.5 trillion. Some of the poorest countries, many in Africa, saw external public debt increased from slightly above 20 percent of GDP in 1970 to almost 140 percent of GDP by 1994. For some, interest payments rose from $230 million to $1.3 billion. In response to campaigners and activists, 41 countries, including 33 in Africa, had their debt waived or restructured.

The current fear is that a significant number of those countries are now at moderate or high debt distress, which may trigger another debt crisis. Africa is at the center of this anxiety, and China’s role in Africa’s emerging debt crisis is attracting significant attention. China is now routinely accused of “debt-trap diplomacy,” (paywall) or intentionally “miring supposed partners, particularly developing countries, in unsustainable debt-based relations.” The assumption seems to be that “China’s own economic and geostrategic interests are maximized when its lending partners are in distress.”

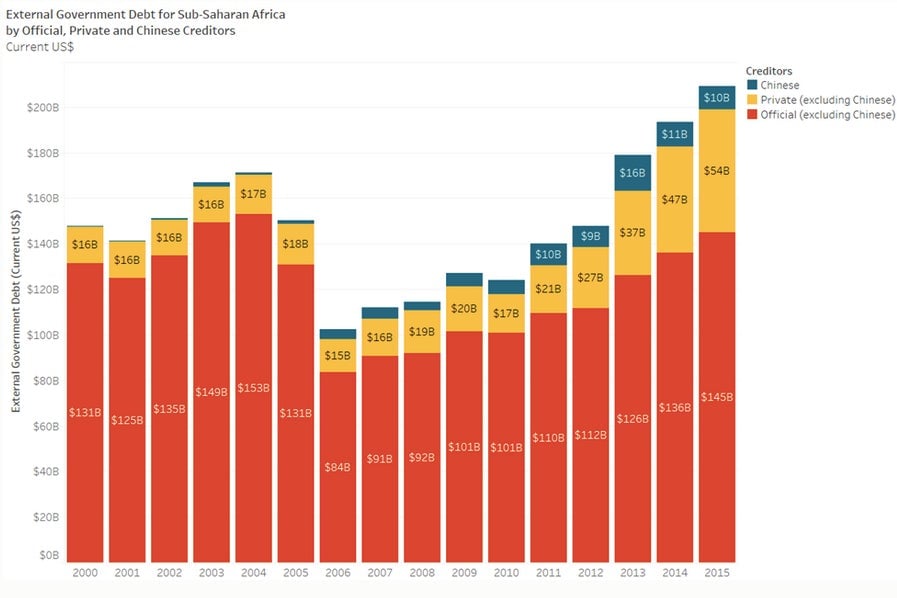

The “debt-trap diplomacy” idea, however, has never been convincingly argued and its application in Africa is, at best, tenuous. The reality of Africa’s debt to China is not particularly remarkable when taken against the aggregate of sources of Africa’s external debt stock (see chart below). A few African countries: Angola, DRC, Ethiopia, Kenya and Sudan account for over half of Chinese lending in Africa. A number of African countries’ (Djibouti, Kenya, and Angola) debt obligations to China are high and many are now alarming—as they would be regardless of creditor. There is a high likelihood that some of this debt will be restructured.

As evidence of China’s putative “debt trap,” the Sri Lankan port at Hambantota where failure to service the loan resulted in a 99-year lease and China’s control of the asset. This evidence, however, conveniently ignores 84 instances (pdf, p. 29-32) over the last 15 years, of China restructuring/waiving loans without taking possession of assets, including Ethiopia’s third such restructuring. The argument for bad-faith Chinese lending also ignores Venezuela—the single largest Chinese debtor country where there still isn’t Chinese takeover of flagship state assets.

The language of “debt-trap diplomacy” resonates more in Western countries, especially the United States, and is rooted in anxiety about China’s rise as a global power rather than in the reality of Africa. As Evan Feigenbaum of the Paulson Institute think tank writes, treasury secretary Steven Mnuchin has counseled countries against taking Chinese money, warning it will lead countries into a debilitating cycle of debt, and asset-stripping. The US Department of Defense accuses the Chinese of predatory economic practices.

For Africa, Chinese financing—and by extension, FOCAC—remains an indispensable option. First there is the history of the West dismissing African infrastructure plans as “uneconomical and unnecessary” and a long history (since the ’60s) of the Chinese stepping in instead. The West has also almost exclusively anchored its engagement with Africa in development—rather than business. European Union President Jean-Claude Juncker himself admitted as much in his State of the EU address last week when he noted, that the EU will “have to stop seeing this relationship through the sole prism of development aid.”

The Population Reference Bureau projects that Africa will be home to 58 percent of the projected 2.6 billion increase in global population between now and 2050. Africa is not creating jobs anywhere near the pace needed to accommodate those numbers. It also lags behind all other regions of the world on every measure of infrastructure coverage. This has led to tepid industrial growth, with Africa’s share of global manufacturing falling from about 3 percent in 1970 to less than 2 percent in 2013.

Across Europe and the United States, nativist political parties and racist politicians, some openly hostile to Africans, are either winning elections or comprising significant parliamentary blocs. Therefore, investment from China is one of the few ways African countries can get financing for the infrastructure it so desperately needs.

China has financed more than 3,000 strategic infrastructure projects in Africa and extended tens of billions of dollars in commercial loans to African governments and state-owned enterprises. China’s export of excess industrial capacity and its model of special economic zones has benefited the nascent manufacturing sector on the continent. An in-depth evaluation of Africa’s economic partnerships with the rest of the world in trade, investment stock, investment growth, infrastructure financing, and aid concluded that no other country matches the depth and breadth of Chinese engagement.

It appears, however, that a combination of domestic and international pressures—both economic and political—will limit Chinese ambitions, at least as expressed through extension of credit.

China watchers have seen “obvious signs of discontent” (pdf) with President Xi Jinping’s policy agenda, including Chinese spending in Africa. Jamestown Foundation’s China Brief editor-in-chief Matt Schrader notes that “BRI lending has already begun to shrink, decreasing dramatically since 2015.” Schrader suggests a link between emerging criticism of the expansive BRI—the Belt and Road Initiative, an infrastructure plan announced in 2013 and spanning Asia, Europe, and Africa—which its domestic Chinese critics have taken to calling “aid,” and the reduced ambition of the program.

As China’s trade war with the United States escalates, the People’s Bank of China is attempting a balancing act between allowing the yuan to weaken against the dollar and intervening to arrest the decline before it leads to a devaluation that would affect the Chinese economy. And this trade war is occurring as China attempts to manage its massive domestic debt (paywall). Even if a crisis does not emerge, managing this debt will remain a prominent focus of Chinese policymakers.

In terms of outside pressure, China is also facing pressure to conform to international lending standards from the International Monetary Fund.

Meanwhile, the narrative of weaponized loans is beginning to spread. For example, 16 American senators wrote a letter (pdf) to Treasury Secretary Steven Mnuchin and Secretary of State Mike Pompeo inquiring “how can the United States use its influence to ensure that [IMF] bailout terms prevent the continuation of ongoing BRI projects, or the start of new BRI projects?” The incident with the Hambantota Port in Sri Lanka is paraded as evidence of China’s bad intent in providing loans to low-income countries. Domestic politics in partner countries is also beginning to affect Chinese lending, with Malaysia canceling two large Chinese projects after elections brought a new government to power.

Under Xi, China has increased its focus on making China’s voice heard on a global level. China is determined to assure its African partners that it remains a stable and dependable ally, particularly as Chinese leadership attempts to contrast itself with its American counterpart.

But the pressures outlined above cannot be ignored. Coming out of FOCAC, Chinese officials “vowed to be more cautious to ensure projects are sustainable.” Using sustainability as a criterion will increase the quality of Chinese lending and limit the scope of projects eligible for lending. Kenya’s inability to secure financing for phase two of the Standard Gauge Railway project amid reports that China wants a study on the commercial viability of the project could be the beginning. While there is now research that concludes that, “Chinese loans are not currently a major contributor to debt distress in Africa,” Chinese lending cannot ignore the numerous African countries facing moderate-to-high debt distress.

Reduced Chinese lending need not necessarily be a bad thing. We now know that Kenyan officials siphoned off billions in Kenyan shillings from Chinese loans for the SGR project. There are still questions about the true cost of the project and whether Kenya overpaid. A set of stricter project eligibility criteria could lead to more competent project preparation and implementation. It could also decrease the incidence of projects selected for funding based on electioneering and politics rather than on social and economic policy outcomes. This might even prompt African states to increase submission of projects that enhance regional integration, trade and commerce.

African states will continue to look toward Chinese lending as a significant component of the suite of tools available to deal with poverty and the gap in infrastructure financing. But the new reality looks set to be one in which the Chinese spigot, while not completely turned off, has slowed as China adjusts to pressures at home and abroad.

A version of this essay was first published on the Center for Global Development blog on August 31, 2018. The author thanks Asad Sami and Kelsey Ross for research assistance.