You’ve probably never heard of Yngve Slyngstad, and that’s understandable. As the financial world buzzes around big-name CEOs like Larry Fink, Jamie Dimon, and Steve Schwarzman, this Norwegian bureaucrat slips happily into the background. He flies economy, doesn’t have a personal assistant, and believes his salary of $800,000—around that of a mid-ranking managing director at Morgan Stanley $MS—is unfairly high.

However, Slyngstad runs Norway’s sovereign wealth fund—which, with around $1 trillion in assets, is twice the size of Morgan Stanley’s investment management fund. The fund controls about 1.4% of all global stocks, and when it throws its weight around, it can really move markets. Some call Slyngstad the “$1 trillion man.”

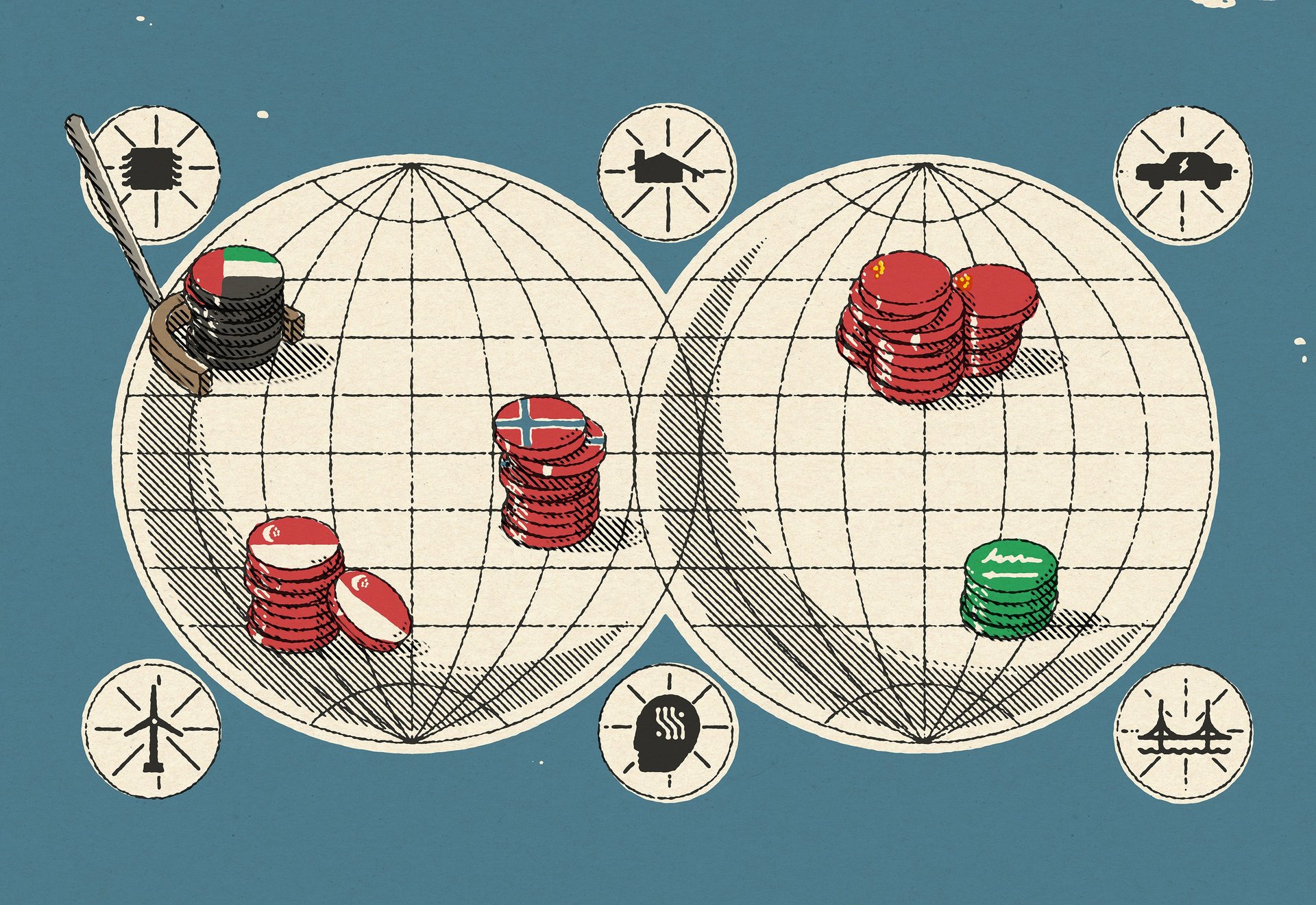

Sovereign wealth funds (SWFs) like Slyngstad’s are major players in finance and venture capital, commanding about $8 trillion in combined assets—equal to around 10% of global GDP. Their goals often diverge from those of traditional private-sector investors, with much longer investment horizons and, as state-backed actors, some ambiguity as to whether their aims are solely financial.

Despite all this, the last time SWFs were really in the news was in 2007, when the Chinese Investment Corporation (CIC) bought a hefty stake in Blackstone (it has since sold its stake in the firm) and helped safeguard Morgan Stanley during the financial crisis.

Founded: 2007

Since then, SWFs’ total assets have more than doubled, and SFWs have started to really put them to work. Once upon a time, moves like CIC’s were far from the norm. Most SWFs were sleepy institutions, safely squirreling the vast proportion of their cash into government bonds, index-trackers, and external funds.

Lately, however, low interest rates have seen SWFs pull money out of bonds, preferring to put it in the more lucrative, and riskier, private markets: they doubled the portion of their assets allocated to alternatives between 2013 and 2018, according to Invesco. Last year, that amounted to 5.5% of all the money invested in private equity worldwide, according to PitchBook.

SWFs have also started actively choosing where to invest cash. In the past, they would generally put that money in a reputable fund and let its managers decide what companies to invest in. “Now they will do it with conditions: I want to co-invest, I want to be a partner on direct investments. I want, I want, I want,” says Tarek Shoukri, a director at PwC specializing in institutional investors.

These changes in strategy have made them ever more active players in the global economy.

Unlike other institutional investors, SWFs have a super-long-term outlook—they’re aiming to secure their countries’ economies for decades. As Matt Whineray, CEO of New Zealand’s fund, told Quartz: “We care about what equity values are 20, 30, 40 years out, as opposed to just what they are the next six months, the next 12 months.”

For many funds, that means identifying the trends that will shape the global economy for most of our lifetimes. While doing so, SWFs—most of which belong to non-Western countries not typically considered global powers—can impact those trends themselves. “When they invest, they really have capacity to influence the whole market,” says Javier Capapé, director of IE Sovereign Wealth Research.

Already, Saudi sovereign wealth (mostly through the kingdom’s investment in Softbank’s Vision Fund) has coursed through Silicon Valley, funding companies like Uber $UBER and WeWork. Norway’s fund recently announced it will pull its money out of 134 fossil-fuel companies that focus on oil and gas exploration.

Founded: 1990

As sovereign capital flows into the world’s burgeoning businesses and economies, it’s time to brush up on where and how men (yes, they’re almost all men) like Slyngstad are thinking about deploying their cash: In technology, renewables, infrastructure, real estate, and emerging markets. Just as pressingly, we need to ask what it means for these often deeply secretive state-run institutions to be playing an ever bigger role in the global economy.

What is a sovereign wealth fund?

As the adage in the industry goes, “If you know one sovereign wealth fund, you know one sovereign wealth fund.” They vary so wildly that the official definition of SWFs is the following, exceptionally vague, maxim: SWFs “are special purpose investment funds or arrangements that are owned by the general government.”

Feel enlightened? Us neither. Perhaps the best way to understand SWFs is to look at one that is succeeding: The case of Chile.

In mid-2006, Chileans weren’t happy. “The streets of Santiago were flooded with protestors,” writes Angela Cummine in Citizens Wealth. The reason for their discontent? Copper prices were booming, and instead of spending cash from the country’s plentiful reserves on fighting poverty, finance minister Andrés Velasco was stashing it in two newly created piggy banks for a rainy day. Effigies of Velasco were being burned on the streets and president Michelle Bachelet’s ratings were at historic lows.

When Bachelet and Velasco left office four years later, however, they “boasted the highest approval ratings of any president and cabinet minister since Chile’s return to democracy,” Cummine writes.

This shift was largely thanks to the SWFs. With about 60% of Chile’s budget coming from copper receipts, Velasco had created the SWFs out of an existing fund—founded in 1985—to avoid wild swings in copper prices. By saving money in good years, they could top up the budget with cash from the SWFs in bad ones.

This paid off very quickly. When copper prices plummeted by 50% amid the global recession in 2009, Velasco and Bachelet dipped into the funds. They had enough cash stored up to give Chileans one of the biggest financial rescue packages in the world at 2.8% of GDP—bigger than any G20 country’s stimulus that year besides fellow SWF-owning Saudi Arabia.

“Chile escaped catastrophe, experiencing only a minor recession despite massively declining government income,” Cummine writes.

Chile’s funds were playing the role SWFs were first designed for; acting as stabilization funds to help commodity-rich countries escape “Dutch disease.” Two other types of SWFs have since sprung up—maximization funds and development funds. These roles may seem divergent, but individual funds often end up combining two or even three of them.

Maximization funds: Where stabilization funds typically invest in very safe bonds and public equities to avoid volatility, maximization funds aim for greater returns with slightly riskier investments. The goal is to secure and grow the country’s wealth for decades. As Slyngstad recently said of Norway’s oil reserves, “It is wealth that was there a long time before this generation existed, and it’s wealth that we should protect for our grandchildren and their grandchildren.”

Development funds: Instead of prioritizing the fund’s growth with international investments, development funds—like Ireland’s ISIF or Russia’s RDIF—direct their cash inwards, aiming to diversify their countries’ economies and often partnering with outside institutions to attract foreign investment into key sectors.

It’s not just commodity-rich countries that have SWFs. Two of the biggest exceptions are China and Singapore. China’s CIC fund was founded in 2007 to manage the massive foreign exchange reserves the country had accrued while keeping its currency low. Singapore has two SWFs (GIC and Temasek), both funded by taxing its citizens more than the government needs for its budget, and paying that surplus into the funds.

Founded: 1981

Number of SWFs worldwide: 78

Number created from 2010-2018: 21

Combined assets: $8.1 trillion

Oil and gas-related assets: $4.4 trillion

Where SWF assets originate by region:

(Data from Preqin and SWFI)

In 2007, weeks after China’s fund had bought its massive chunk of Blackstone, former US Treasury secretary Larry Summers took to the pages of the Financial Times to “register a cautionary note” about SWFs. “It is far from obvious,” he wrote, that maximizing share value “will over time be the only motivation of governments as shareholders.”

They may want to see their national companies compete effectively, or to extract technology or to achieve influence…What about the day when a country joins some “coalition of the willing” and asks the US president to support a tax break for a company in which it has invested? Or when a decision has to be made about whether to bail out a company, much of whose debt is held by an ally’s central bank?

These concerns 1 quickly became the framework for Western capitalists’ fears about SWFs.

But have they come to fruition twelve years on?

Yes and no.

Let’s start with the no. Some SWFs are so secretive we can never be entirely sure, but there’s no evidence that Summers’ most dire concern—that SWFs could play a role in one government strong-arming another—has ever become reality.

In fact, as a whole, SWFs have made great strides in governance and transparency since developing the 2008 Santiago Principles, which aimed to persuade the doubters that they were purely commercial actors, and are implemented by the International Forum of Sovereign Wealth Funds (IFSWF). For the most part, they act as generally passive investors, simply looking to grow their balance sheets.

That said, the only people who will earnestly swear that SWFs’ actions have zero political undertones tend to either work for funds or make money from them. When those people talk on background, the story is often different—ranging from measured statements about “strategic goals” to more extreme mutterings about risks of what one source deeply embedded in the industry called “economic warfare.”

“Politics,” after all, means many things to many people. Gulf funds like Abu Dhabi’s Mubadala and Saudi Arabia’s Public Investment Fund (PIF) openly make investments with an eye to using that expertise to develop relevant sectors in their domestic economies. That’s generally accepted and seen as a legitimate form of “tech transfer.” However, when China is the investor, the term becomes “IP theft.” Given China’s history with that matter, you can understand why.

Governments have become vigilant about protecting intellectual property in recent years, with the Obama and Trump administrations both blocking attempts by Chinese state entities to buy semiconductors. The PIF recently hired lobbying firm Akin Gump, an arch Washington insider, to help it navigate CFIUS, the body tasked with analyzing the national-security threats posed by foreign investments. Meanwhile, Australia and France are moving to set up CFIUS equivalents, and Germany’s finance minister recently proposed a state fund to compete with Chinese tech investments.

There’s also no denying that some SWFs can be used as diplomatic or political PR vehicles. It might be a stretch to claim, as some experts do, that Saudi Arabian crown prince Mohammad bin Salman’s entire resurrection of the PIF is just a geopolitical branding exercise. But heads certainly turned last month when the prince, under a hailstorm of criticism for allegedly ordering the murder of journalist Jamal Khashoggi, flew to India for a hug with prime minister Modi and Saudi Arabia’s fund announced a memorandum of understanding for future investment with Indian hotel giant OYO on the same day.

The prince’s reported control over the fund pushed several of its top Western hires to quit last year, the WSJ reports, and the PIF is apparently struggling to fill those posts in the wake of the Khashoggi murder. (In a statement, a PIF spokesperson said that the fund’s “strategy, governance and operating model are built on global best practice,” adding that its staff turnover rates are lower than the average for the Saudi economy and financial services generally, and that the WSJ story “referenced 3 individuals that departed over an extended period, out of around 450 staff members.”)

As for using shareholder power to further political or ideological beliefs, the most obviously activist funds are, in fact, the Western democracies. Norway has generated a slew of headlines for pushing firms to cut greenhouse gas emissions, overhaul executive pay, and publish data on their gender pay gaps. They have so far paused plans to insist on gender parity on corporate boards for fear of being seen as imposing “Nordic values.”

SWFs haven’t helped themselves by remaining incredibly opaque. Some of the largest funds don’t even disclose the size of their assets, let alone where they’re invested. Their defenders say they’re no worse than many university endowments and other private investors, and that more disclosures could hurt their performance. “I think one needs to be careful about not imposing double standards here,” says Duncan Bonfield, CEO of the International Forum of Sovereign Wealth Funds (IFSWF), adding that calls for transparency are “a bit of a cheap shot” at SWFs.

However, university endowments aren’t trying to persuade people that their investments don’t have geopolitical goals. Nor do New Zealand’s impressive returns seem to be hurt by its openness. Norway, which is radically transparent, got so fed up with other SWFs’ unwillingness to comply with the Santiago Principles that it quit the IFSWF in 2016, saying, it “has not met our expectations as an organization with sufficiently strong progress in the implementation of principles.” (Bonfield declined to comment on the departure, saying Norway had never made that complaint directly to him.)

Perhaps the biggest culprit in all this is Qatar. In 2008, Qatar’s finance minister told his US counterpart that “only five or six people in Qatar know” where the QIA’s assets are allocated, according to a US diplomatic cable obtained by Wikileaks. It begrudgingly signed up to the Santiago Principles, but, six years later, a study dubbed it the only fund to not even be partially compliant with the rules, which have no enforcement mechanism.

When Qatar recently found itself the subject of a blockade by its Gulf neighbors—who, incredibly, received US support—it began making financial overtures to the US. Most blatant was a $100,000 injection to keep the Washington, DC, metro open for an extra hour after its ice hockey team’s playoff last year. More ominously, some onlookers have suggested that, as part of this push, a firm backed by the QIA extended a massive loan to bail out the family business of Jared Kushner, president Trump’s son-in-law and eminence grise. Aside from suspicious timing, there’s no real evidence to support the theory, but a Democratic senator went so far as to mention the funds’ Qatari origins in an ethics complaint about the loan. (The QIA didn’t provide a comment for this story.)

Rumors and suspicion aside, these are generally rather different institutions to the ones Summers warned about over a decade ago. Along with their assets’ dramatic growth, they have professionalized considerably, many of them staffed by deeply intelligent asset managers from all over the world, looking to make smart commercial decisions.

But, ultimately, these are state investors representing their governments, and they’ll always be seen with a skeptical eye from various quarters. As the world turns more protectionist, that’s unlikely to change—and, although there are some protections in place, the threat of these largely passive investors suddenly turning active isn’t one you can ever fully write off. The current trend of SWFs sidestepping asset managers, and becoming direct shareholders with voting power, does nothing to dull such concerns.

Founded: 1971

The specter of Softbank’s Vision Fund looms large over Silicon Valley.

In 2016, Masayoshi Son, the mercurial CEO of the Japanese giant that owns telecoms firm Sprint and many other household names, was reportedly listening to a proposal from one of his executives to create an incredibly ambitious $30 billion venture fund. That would have been several times larger than the biggest one in history. He told the exec to take the number to a round 12 figures: $100 billion. The Vision Fund was born, instantly making Son one of the biggest (if not the biggest) venture capitalists in the world. The fund began raising money from other parties, most notably $45 billion from Saudi Arabia’s Public Investment Fund (PIF). Armed with its unprecedented account balance, the Vision Fund swiftly began shaking up the US tech sector, buying hefty stakes in Silicon Valley darlings like Uber, WeWork, and Slack $WORK.

Try to interview Bay Area professionals about all this, however, and you won’t get far. When, on a recent trip to San Francisco, Quartz asked sources to chat about sovereign capital in the Valley, requests were met with laments about busy schedules, unfortunate travel plans, and, occasionally, deafening silence. The venture capitalists and entrepreneurs who eventually agreed to speak would only do so anonymously. (SoftBank also declined to comment on the record for this piece.)

The reason for the secrecy? Jamal Khashoggi. The outcry over the journalist’s murder last Fall, allegedly on Saudi crown prince Mohammad bin Salman’s orders, made the Valley’s would-be do-gooders suddenly uneasy about having unquestioningly taken a brutal regime’s money.

On top of SoftBank’s purchases, the PIF has made direct investments of its own, dropping extraordinary amounts on stakes in Uber, Tesla $TSLA, the latter’s rival Lucid $LCID, and augmented reality firm Magic Leap. (PIF’s statement to Quartz emphasized the fund’s role in MBS’ attempts to reform the Saudi economy, saying, “PIF acts as the engine for this transformation…participating in, contributing to and shaping the domestic and global economy, with patient capital and a long-term view.”)

It all adds up to an incredible injection of SWF money in US tech—including a tidy $15 billion invested in SoftBank by UAE sovereign fund, Mubadala—that has further engorged a sector already flooded with capital. Despite Valley-dwellers’ professed queasiness about all this, no one Quartz asked there had heard of a company actually turning down SoftBank money since then. However, the PIF itself has been hit: Giant Hollywood talent agency Endeavor reportedly returned $400 million to the fund in recent weeks, and Richard Branson said last October that he had aborted talks with the PIF about a planned $1 billion investment in his space business.

The hubbub has overshadowed a longer-running trend, though. Saudi was pretty late to the party—other SWFs have been investing in US tech for over a decade. As is often the case in the sovereign wealth sector, Singapore’s GIC and Temasek have been well ahead of the curve, making a combined 185 deals just in direct investments since 2008. Javier Capapé of IE Sovereign Wealth Research says his data shows the two funds have made 40 to 50% of all SWF venture capital deals.

Putting aside reputational risk, SWFs are an attractive source of money for founders. As Pitchbook senior analyst James Gelfer puts it, “In large deals, it’s unusual not to see a sovereign wealth fund.” They’re there for the long term, meaning companies don’t have to focus on immediate rapid growth. They tend to be pretty passive investors, meaning firms can get on with what they care about. As direct investors, SWFs don’t tend to bring the business expertise of established venture-capital players like SoftBank. But they can sometimes provide access to new markets, opening doors to what might be tricky regulatory environments in their often-authoritarian home countries.

SWFs’ arrival has been a boon for the late-stage companies they tend to invest in. As unicorns do all they can to avoid the scrutiny and quarterly short-termism of the public markets, SWFs and other institutional investors provide a ready source of money that lets them scale while staying private.

Others in the Bay area are less thrilled. A joke going round is that all this cash is really going to “recruiters and landlords,” one entrepreneur says. Facebook $META and Google $GOOGL have long paid massive salaries, but late-stage start-ups flush with cash can now get close to matching them, rather than relying mainly on equity to attract talent. For younger companies, that can make it tough to find good hires. “It’s like trench warfare trying to get technical talent in this city,” complained the entrepreneur. Firms end up paying stiff fees to recruiters, and the giant wages push up San Francisco’s already exorbitant living costs.

Beyond salaries, it’s not clear what exactly some companies are doing with all this money. Many eyebrows went northward last year when the Vision Fund spent $300 million on a 45% stake in dog-walking app Wag. No one could quite puzzle out why an app that connects people—not exactly a capital-intensive endeavor—needed so much cash.

One theory taps into a concern that many in Silicon Valley have about SWFs: that when there are a handful of competing companies in a space, these massive funds can swoop in, pick one company, and give them an enormous amount of money, artificially juicing them so their competitors can’t possibly keep up. “It’s scary for founders and gives big leverage for large funds,” says one VC. A case in point: In 2015, online lending firm Social Finance was looking for a few hundred million dollars in investment. SoftBank was interested, but not in such small change. It told the firm’s CEO Mike Cagney that it planned to invest $1 billion in online lending—Social Finance could take the check or let it go to a competitor, Cagney later told Bloomberg. He acquiesced.

SWFs first entered Silicon Valley by investing in venture-capital funds, and letting those funds disperse their cash for them. Over time, they’ve become more sophisticated, with several opening offices in the Valley. That growing sophistication has made venture funds’ chunky fees and short 3-to-5-year investment cycles ever more irksome, pushing SWFs to invest directly, which allows them to hold shares much longer.

However, as direct shareholders, SWFs’ new potential to exert influence over tech firms has reawakened among some the old fear that they could be used as a tool for authoritarian or corrupt states to control Western companies. However, there’s little evidence that SWFs have ever tried to directly manipulate companies’ operations to their own ends.

A source who has observed PIF managing director Yasir Othman Al-Rumayyan in board meetings said he is, “A very savvy, straightforward guy and views his role on boards of directors to be about oversight, as opposed to running the companies.” The source continued: “This is in contrast to most SWFs who take a more passive role in their invested companies.”

The bigger concern is over intellectual property. While SWFs largely act as purely commercial investors, few who are familiar with them believe they don’t also have strategic goals. As one VC who works closely with SWFs puts it: “All sovereign funds do carry a national flag.” Open expertise sharing with investors like the PIF and Mubadala doesn’t seem to spook companies in the Valley. 2

A bigger headache is China. Chinese funds tend to avoid making direct investments for fear of seeming political. That doesn’t stop them putting money in strategic sectors like AI, 5G, and semiconductors, says the venture capitalist who works closely with SWFs—instead, they invest “in funds that they know would invest in those sectors.”

Businesses offered Chinese money thus face a dilemma: “[They] worry about IP and tech transfer, but China is such an important market that, if you get into that, you have a much bigger ecosystem to expand your product and sell it,” says Winston Ma, a former managing director at CIC. He points to gaming company Twitch and VR software firm Unity, which took money from a CIC-backed fund and expanded successfully into China.

SWFs’ switch to direct investing also seems to be having a tangible impact on asset managers. As SWF direct investments skyrocketed, the number of active private-equity firms fell for the first time this century in 2017, and again in 2018, which Gelfer of PitchBook attributes in part to a pullback from investors like SWFs.

Despite an environment where 61% of SWFs think private equity is overvalued, SWF tech investments continue to surge. Last year, they hit a peak of $39 billion just in direct venture capital investments (i.e. not money from SWF-backed funds like SoftBank’s Vision Fund), making up 14% of total global VC activity, according to PitchBook.

The sheer size of those investments mean they run the gamut of technologies, but the VC who works closely with SWFs says big areas of interest are “frankly ones that are on some of these lists that the US government has put out as sensitive areas.” He notes several technologies listed by the Treasury’s “critical technology” pilot program, such as AI, 5G, semiconductors, biotech, batteries, and other new-energy tech.

Beyond investing in tech companies, funds are using their exposure to Silicon Valley to develop their internal technologies, says Stanford academic and SWF expert Ashby Monk. Funds like Australia’s Future Fund and Singapore’s GIC are leading the way in using AI and other technologies to process the extraordinary amounts of data gleaned from their massive investment portfolios, and using that to give them an edge across sectors.

As for Silicon Valley, the big question is how its embedded institutions react to the shake-ups brought by SoftBank and sovereign capital. One VC giant, Kleiner Perkins Caufield & Byers, has decided to back off entirely, announcing a “return to its roots” of small, early-stage investments—i.e. ones that won’t compete with SoftBank. By contrast, Kleiner’s longtime foe Sequioa, the creme de la creme of West Coast venture capital funds, is setting up what CNBC called a “$12 billion war chest.”

That would have been an enormous pile of cash a couple of years ago, but it doesn’t hold a candle to SoftBank.

That’s not to say the Vision Fund is necessarily in a great place, either. A recent WSJ report suggested that the PIF and Mubadala are getting fed up with the Vision Fund’s large valuations, its at times chaotic decision-making processes that reportedly see Son unilaterally overrule his executives on deals, and with SoftBank’s reported plan to transfer a huge chunk of its shares to the Vision Fund at a mark-up. A planned $16 billion investment in WeWork was recently cut to just $2 billion, reportedly after the Saudis and Emiratis looked askance at the giant sum. (Mubadala declined to comment to Quartz on the reported tensions; earlier, all three parties told the WSJ their relationship was good, saying they have confidence in the Vision Fund.)

Nonetheless, Son last year told Bloomberg he wants to raise a $100 billion fund every two or three years and deploy about $50 billion per year; all part of a grand plan for the company “to grow as a corporate group for the next 300 years.”

For that, he needs SWFs, which are pretty much the only institutions with those horizons and that much cash. Similarly, they need him, his firm’s expertise, and—crucially for the PIF—his still-sparkling brand.

Founded: 1976

A lot of SWFs are from countries rich with fossil fuels, and were set up with the express purpose of diversifying their economies away from carbon. Where better to put their money than in green energy?

Quite a lot of places, it seems. Whether it be Saudi and the UAE bigging up plans for green cities in the desert, or Norway saying it should divest from oil and gas, SWFs love talking about the environment. In practice, however, “their progress is slow—unfortunately slow,” says Mindy Lubber, CEO of Ceres, an NGO that works with massive investors to get more money into green energy.

The Saudis are only just starting construction on planned $500 billion green mega-city Neom. The UAE’s green city Masdar is, at present, “a lot of dirt and a few buildings,” says a think tanker who recently visited. Meanwhile, the Norwegian government has barred the fund from fully divesting from oil and gas, and is yet to decide on investing in unlisted renewables.

SWFs are not alone in being slow to go all-in on renewables—green experts say all institutional investors are years behind where the planet needs them to be in terms of green cashflow. Institutional investors made up just 5% of new renewable investments last year, and SWFs account for probably only a fifth of that or less, estimates David Livingston of the Atlantic Council’s Global Energy Center.

As of May 2018, SWFs’ total green investments were at $11 billion—just 0.15% of their combined assets, writes Capapé, though he notes that renewables make up a decent chunk of their direct investments in recent years.

The main reason is that companies are still not charged for the environmental cost of the carbon they produce, says Matt Whineray, CEO of New Zealand’s fund, which has been comparatively ahead of the curve on green investments. If you can say, “‘Ah look, the price of carbon is going to be 100 bucks a ton,’ then you will see people starting to allocate capital toward [renewables] because there’s less perceived regulatory risks,” he says. Capapé adds that weak political demand in most countries and the high cost of carbon-footprint analysis don’t help.

SWFs have made some movement on decarbonization, however. While Norway is yet to shift its oil and gas stocks, it has promised to divest from coal (albeit with some large loopholes) and from fossil-fuel exploration firms. Ireland’s fund is divesting from fossil fuels entirely, and the likes of New Zealand and Alaska have significantly shrunk their exposure to oil and gas. Between 2015 and 2017, Norway and New Zealand’s combined fossil fuel divestments were around $2.8 trillion, according to Capapé’s figures.

For New Zealand and Alaska, those moves have been business, not ecological decisions. “The compelling stories are away from fossil fuels right now,” Alaska Permanent Fund CEO Angela Rodell told Quartz.

Just divesting isn’t enough to save the planet, however. “Some other investor has now bought those things that we sold—so how does that change the equation?” Whineray asks. “The change actually comes where you’re applying capital to change things that are going to change the technology, or adapt or mitigate the physical impacts of climate change.”

Despite environmentalists’ complaints, SWFs are slowly starting to move that capital. In 2017, CIC was part of a consortium buying a $3.7 billion majority stake in Ecquis, Asia’s biggest independent renewable-energy firm. ADIA and GIC have invested several billion in Indian renewables, with stakes in firms like ReNew Power, Ostro Energy, and Greenko, which then swallowed up wind power competitor Orange Renewable.

India is an attractive destination for green investments partly because its state-run electricity monopolies are inefficient and expensive—and because renewables projects there make sense without being driven by subsidies. “A subsidy is provided by the government, so it might be there today and then possibly withdrawn at a later point in time. We believe an investment should work without the need for subsidies,” says Khadem Alremeithi, executive director of ADIA’s Real Estate and Infrastructure Department.

ADIA’s Emirati rival Mubadala has perhaps been the most dynamic SWF mover on climate investments. Its offshoot Masdar has, aside from funding its eponymous green “city” on the edge of Abu Dhabi, become a massive investor in offshore wind. Its windfarms now power more than a million British homes, and they have worked with Equinor to develop battery storage for them. Alongside state oil company ADNOC, Masdar has also been at the forefront of carbon capture and storage, the radical technology that aims to trap industrial emissions and pump them underground.

Most funds have found green tech tricky, however. That’s perhaps partly down to several SWFs still smarting from the 2010 clean tech bubble, but also because the technology is still at such an early stage that it’s not ready for the eight-figure checks SWFs are looking to drop.

Ultimately, it remains a question of ‘when’ for SWFs and renewables. At some point, SWF money is going to pour into green energy in a deluge. There are promising signs afoot—not least PIF managing director Yasir al-Rumayyan’s recent claim that “we will be the largest investor in renewable energy”—but environmentalists can only hope that happens soon enough.

One thing is sure, however: To save the planet, “it’s absolutely imperative that institutional capital is in there at much greater scale and in much larger ratios than it is now,” says Livingston.

Founded: 1953

SWFs are, by and large, savvy, sophisticated investors with good—and ever improving—governance structures. That hasn’t always been the case, however, and it certainly doesn’t apply to all funds.

A source, whom we’ll call John, had an eye-opening experience while working in the London office of a major Gulf fund’s real-estate arm in the early 2010s. (John, who signed a non-disclosure agreement with the fund, asked Quartz not to use his real name or to name the fund, so that he couldn’t be identified.)

The fund set up shop in what John estimates was the most expensive London office space available at the time. They had four spacious floors for a few dozen employees, leaving just a couple of people working on their own on the roughly 2,000 square-foot ground floor, he says.

The fund had enormous amounts of cash sitting around and accruing little interest. Its spending strategy was rather simple: Find high-profile properties and sink piles of money into them. The team would often run models on a big-ticket property for the fund, report back that it was a risky decision, and find that the fund wanted to invest anyway. “Investment decisions were made based on prestige,” John says.

Even as the world stumbled out of financial crisis, the hand on the purse strings was not exactly tight. At one point, all staff received an email saying that the fund was cutting back on expenses. An edict was handed down—no director should have more than two drivers. When someone explained that the London office didn’t actually employ a single driver, instead using the Tube and the occasional taxi, the gist of the response, John says, was: “My god! You mean to say you don’t have any drivers? The CEO doesn’t have a driver? You must have a driver.” A driver was hired.

When the government minister in charge of the fund came to London, he would descend with a retinue of half a dozen people and a briefcase full of cash. After sitting through a meeting or two, they would take the briefcase and go on a “mental shopping spree,” John says.

Despite the profligacy, John thinks their general investment strategy wasn’t a bad one. “They had so much money lying around that they needed to deploy it—as a consequence of having billions of dollars in revenue every year, there aren’t enough asset classes in the world in which you can deploy it,” he says. “There’s a limited amount you can do, so buying a site for hundreds of millions in London, the cost of employees, drivers etc is completely inconsequential—its the interest you make off it [that matters].”

Founded: 1974

Infrastructure, real estate, and sovereign wealth are, in theory, a perfect match. The first two need a bunch of capital but promise good returns over decades. The latter wants to invest as much cash as it can and to pay off over a very long time.

It should be no surprise that, as SWFs step up their private investments, infra and real estate—which often overlap—have eaten up the bulk of that cash.

Technology is beginning to cause radical changes in the sector. We saw a glimpse of this in 2017 when the CIC bought European logistics firm Logicor for a jaw-dropping €12.25 billion, beating out Singapore’s Temasek and GIC in a reported bidding war.

The reason the three sovereign wealth giants were going after a dull firm with assets comprised mainly of warehouses? In a word: Amazon $AMZN. This is a bet on “longterm economic changes,” says Capapé of IE Sovereign Wealth Research. “The consumption pattern and behavior among Europeans is going digital,” and e-commerce “needs a lot of brick and mortar, a lot of facilities around big cities.”

The Locigor purchase didn’t come about in a vacuum. The whole logistics sector is “flourishing” among SWFs, says Alremeithi of ADIA’s Real Estate and Infrastructure Department. Asian logistics giant ESR has taken cash from Azerbaijan’s State Oil Fund and recently started a joint venture with another undisclosed SWF, while its main rival GLP has partnered with GIC.

This trend in tech-adjacent infrastructure investing is a sign of things to come. Alremeithi said ADIA has set up a group focused on using its tech portfolio to inform its infrastructure investments. “Tech is a big challenge to understand and anticipate,” he says. “We want to try to interact with tech-related venture-capital companies and…try to understand what next the wave looks like.”

We’re only just starting to see how that will play out, but there are already intriguing signs.

With the automobile industry set to be upended by electric and self-driving cars, Mubadala and SoftBank have invested hundreds of millions in Florida-based ParkJockey, a tech platform aimed at monetizing the changing role of car parks.

The Vision Fund has made several big bets on how technology will shift the real estate industry, most notably through its investments in WeWork and that company’s ostensible potential to fill previously wasted, empty office space to capacity. (Though its faith in the firm seems to have nosedived, with the aforementioned $14 billion cut in investment.) It has also invested hundreds of millions in construction-technology firm Katerra and reportedly encouraged it to collaborate with Plenty, an indoor-agriculture firm also in the fund’s portfolio.

Demographics are also a crucial factor in shaping these investments. Europe’s aging economies have been inundated with SWF investments in “aged care,” also macabrely termed “deathcare.” These range from hospitals, to old people’s homes, to crematoria—the last of which appeals partly due to bodies’ potential to create green energy when cremated, said a source who works with SWFs.

Founded: 2005

The accepted view of sovereign wealth funds has changed dramatically over the past 15 years. Once considered an urgent threat to the liberal world order, they are now often seen as little more than a quirk of the global economy, of note only to those deeply immersed in finance.

Neither analysis hits the mark. While the fear of SWFs-as-authoritarian-threat is a dog that hasn’t barked, few experts will tell you they’re never used to further political goals—whether to invest in strategic sectors or to extend diplomatic olive branches.

SWFs have grown so dramatically in recent years that they’re increasingly difficult to ignore, taking significant stakes in many of the world’s most important and exciting companies. What does that mean for the global economy? We’re in a time of such geopolitical upheaval, and some major SWFs are so shrouded in secrecy, that there’s no clear answer.

We don’t even really know whether they will become mainstays of the world’s economy or brief historical oddities. While SWFs say they invest over a 30-plus year timeframe, most of them are little more than a decade old, notes Adam Dixon, a political economist and co-author of Sovereign Wealth Funds. Their expected longevity “all comes down to the assumption that states are longterm—that the nation state exists in perpetuity,” he says. That is far from guaranteed.

For the time being, however, SWFs are very on trend. Their rise is taking place at a time when governments become ever more active players in markets across the board. State capitalist economies like China are rising, protectionists like Trump are seizing power in the West, and even Germany’s center-right government is pushing for more state involvement in the economy.

Summers noted SWFs’ potential here back in 2007, writing that, as state actors, the question of how they invest “is profound and goes to the nature of global capitalism.”

Well, the future of global capitalism now looks mighty different from the era of pre-crisis neoliberalism that Summers was writing in. Sovereign wealth funds, for the time being at least, look set to play an ever-growing role in whatever we end up with.

Correction (March 12): Saudi Arabia’s Public Investment Fund was founded in 1971. An earlier version of this story indicated the date was 2008, citing incorrect information from the Sovereign Wealth Fund Institute.