On Dec. 18, the Fed announced that in January it would start tapering its purchases of treasury bonds and mortgage-related securities by $10 billion a month, down from $85 to $75 billion per month. It also hinted that it would keep on tapering, possibly at a rate of $10 billion per meeting of the Federal Open Markets Operations Committee. The Fed also said that interest rates are unlikely to increase before the unemployment rate declines below 6.5%.

The new policy mix seems to have accelerated the outflows of capital from the emerging markets (see here and here). Yet, the initial response of the domestic markets was anti-climatic. The S&P 500 ended the week at record highs. The real economy (that is, Main Street) does not seem to have taken notice of the announcement.

Is that strange? People who supported quantitative easing would argue that nothing is happening because the program has been quite successful. In their minds, this is similar to what happens when, after a successful recovery from a surgery, the patient walks happily away while the physicians dismount the equipment that has kept him alive. Before coming to this conclusion, however, we must ask ourselves, what did quantitative easing do for Main Street? Did it actually help to keep the patient alive?

Unless you believe in Voodoo, you will want to identify the means through which quantitative easing transmitted its possibly beneficial impact to Main Street. We can think of two ways. One is increased availability of credit. The other is lower long-term interest rates. Common sense and economic theory suggest that the two are linked. Larger amounts of credit lead to lower interest rates and lower rates lead to larger amounts of credit. On this basis, we should look only to one of the two variables. Yet, Fed distinguished between the two in its rhetoric, even if the open market operations are based on the supposition that they are linked as the Fed buys credit instruments to lower interest rates. The reason for this distinction seems to be that the Fed controls the short-term interest rates, not the long-term ones, through its conventional open market operations. When the crisis exploded, the Fed was able to lower the short-term rates to practically zero, but the long-term ones remained aloft. Quantitative easing increased the purchases well beyond what was needed to keep the short-term rates close to zero. It also aimed at reducing the long-term rates by purchasing long-term instruments in the market, including agency mortgage-backed securities ($600 billion between 2008 and 2009 and $40 billion per month since September 2012.)

Thus, we can look at volumes of credit and interest rates separately.

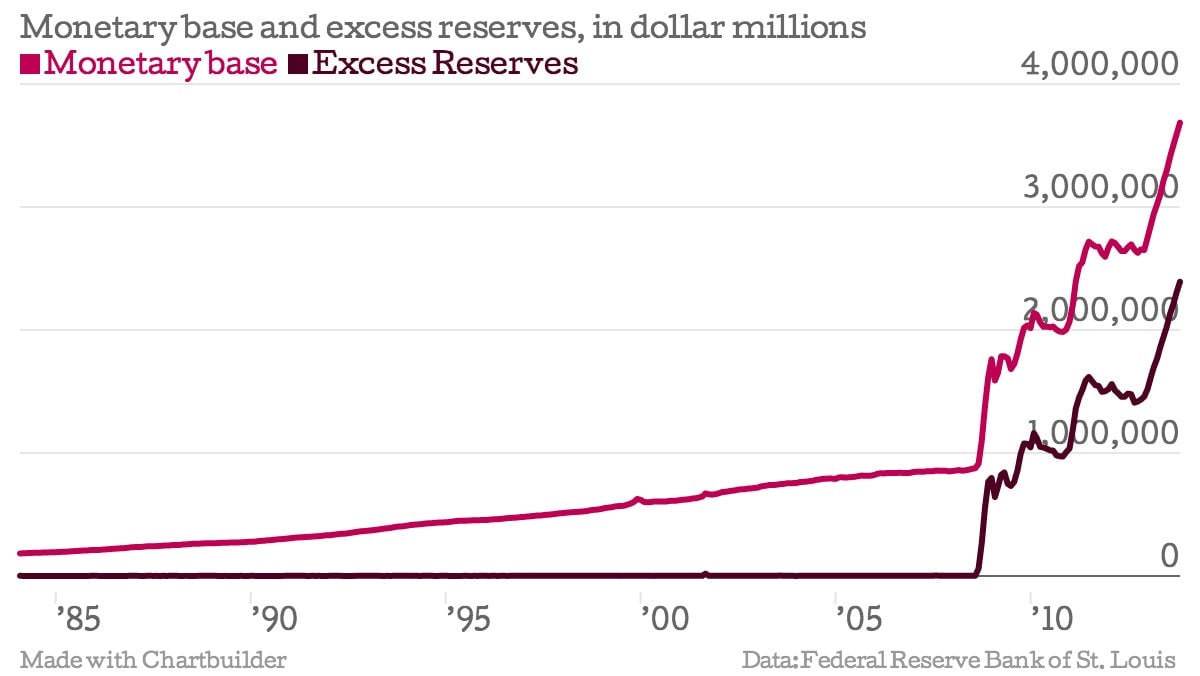

First, we can look at the volumes of credit. The next chart suggests that the help provided by quantitative easing to Main Street in this dimension must have been very scant. Most of the money created by the Fed since the September 2008 crisis through quantitative easing and otherwise has been turned into excess reserves of the banking system (excess reserves is cash that the banks can use to create credit but chose not to and instead deposited it back in the Fed). That is, the cash created by quantitative easing did not become additional credit but, instead, it became excess reserves of the banks deposited in the Fed.

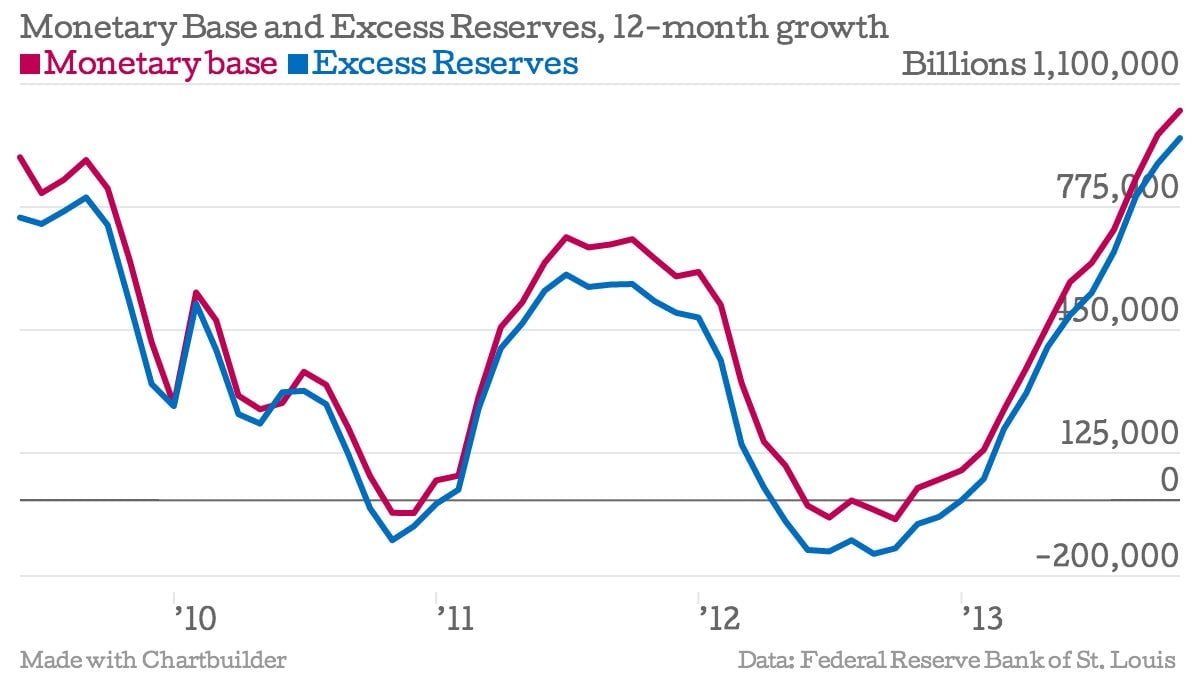

The next chart shows in a more dramatic way that the money created by quantitative easing has been sitting idly in the Fed. The curves plot the 12-month differences of the monetary base (the money created by the Fed) and the excess reserves of the banking system since September 2009 (12 months after the beginning of the crisis). They demonstrate that quantitative easing has worked as a merry-go-round. The Fed created the money only to see it returning as deposits of the commercial banks in the Fed itself.

Thus, we have seen that the money created by quantitative easing did not go to increase credit to the private sector. It had a neutral effect because what the Fed created came back to the Fed. But, what happened to credit? Did it stay put, at the same level?

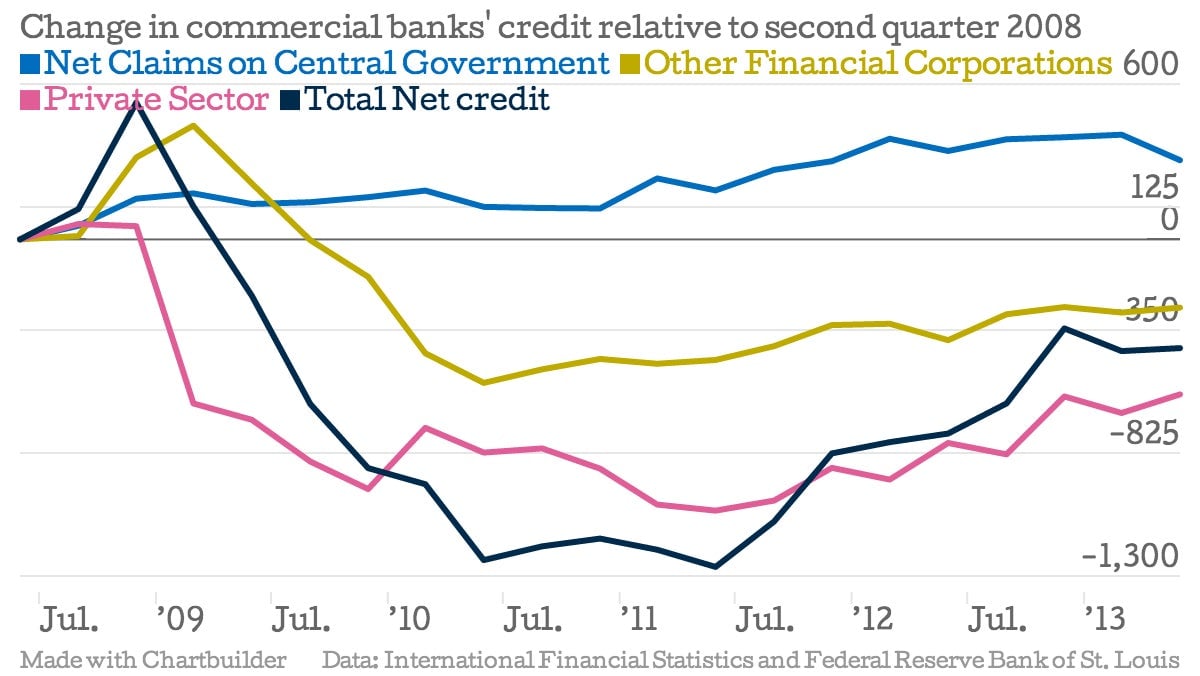

The next graph shows that one major category of commercial banks’ credit increased since the crisis began: net credit to the central government (net of deposits of the government in the banks). However, total commercial banks’ credit went down substantially. By the end of the second quarter of 2013 it still had not recovered the level it had when quantitative easing began. Moreover, credit to the private sector (Main Street) declined and is still $600 billion below its level in 2008. Credit to other financial institutions also went down. Not a nice chart to see.

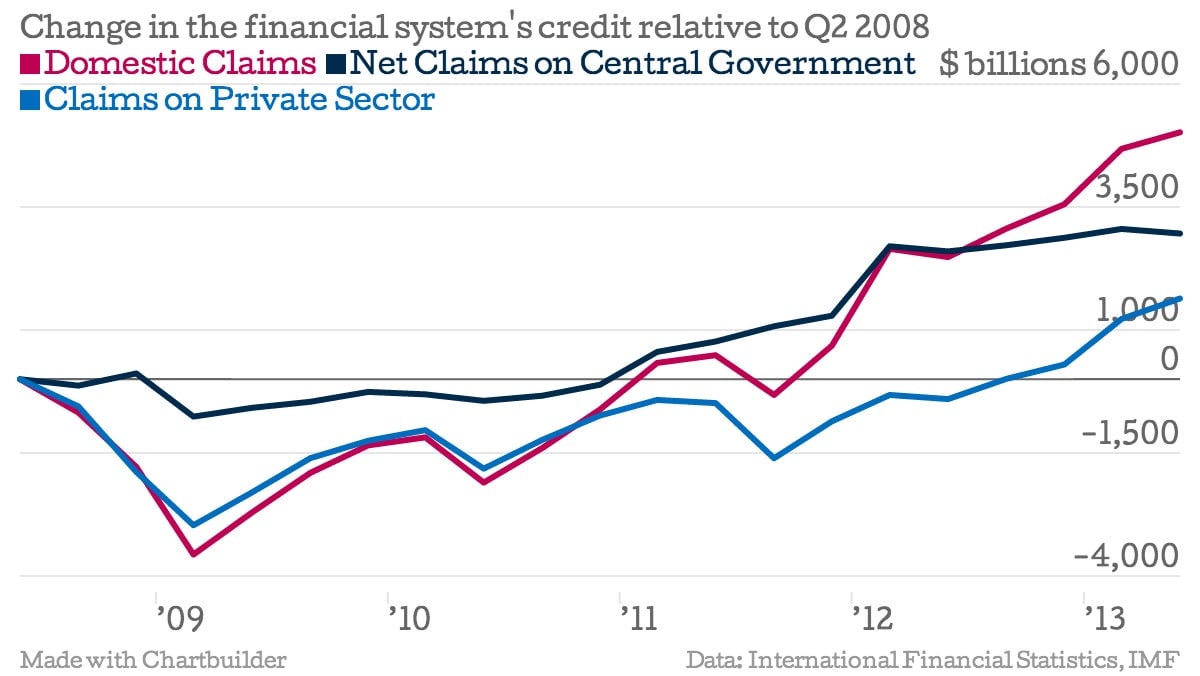

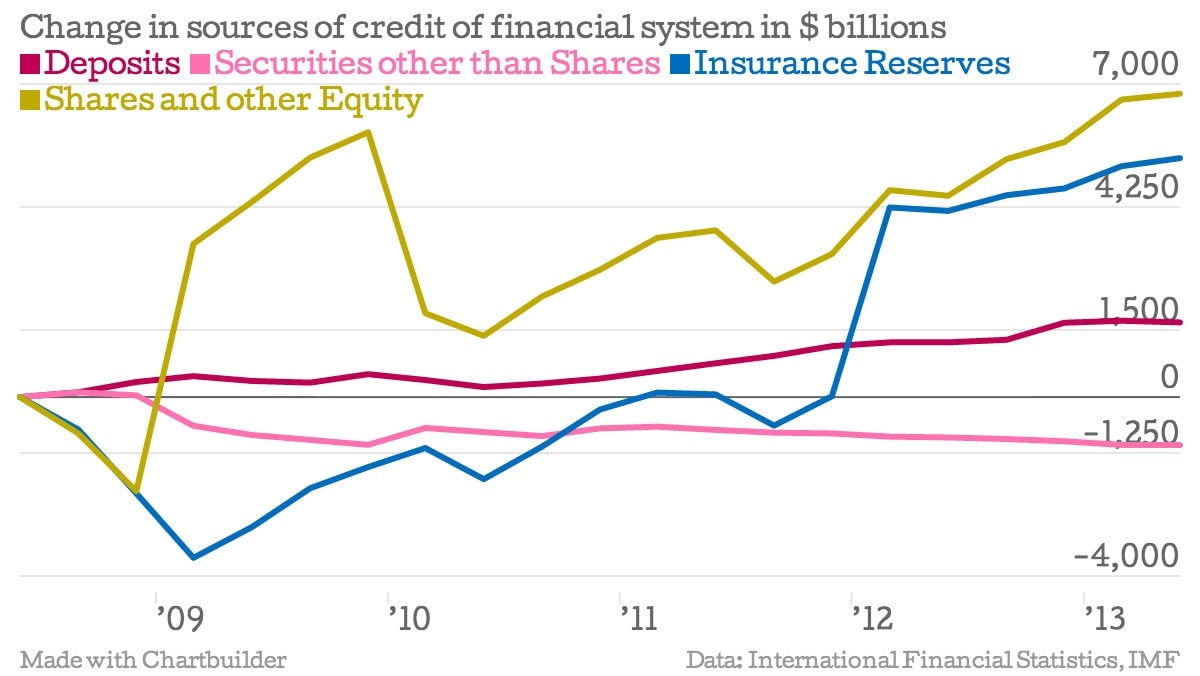

You can argue that this chart does not portray the complete picture because banks are not the only source of credit. Right. The next chart shows that recently the financial system’s credit to the private sector did increase over the level it had at the end of June 2008 (the financial system includes the banks plus all other financial institutions, such as insurance companies).

However, as shown in the next chart, the main source of this credit was not deposits but, instead, the insurance companies’ technical reserves and the financial institutions’ shares and other equities. To believe that quantitative easing helped to increase credit to the private sector you would have to believe that enormous amounts of money sitting idly in the Fed help increasing the technical reserves of insurance companies or lead to larger equity issues by financial institutions. Not very probable.

Now we can look at the interest rate side of our puzzle. You can say that maybe quantitative easing worked not because the money it created became credit to the private sector but because it helped the long-term interest rates to decline and remain low. Certainly, low interest rates, even if they have not increased the volume of credit, may have had a substitution effect in the allocation of financial resources—that is, people who had invested in something not very attractive today (like housing) may have decided to move their resources to invest in equity shares. This lowered the cost of issuing shares to finance companies, including financial institutions (the price-to-earnings ratio has gone up substantially if, as suggested by Nobel laureate Robert Shiller, the earnings are estimated as the average of the last decade).

This seems to have happened. The stock exchange has been in a frenzy of booms since the policies of artificially low interest rates have been applied. The low interest rates did not create new credit to Main Street but diverted resources toward the stock exchange, including the shares of financial institutions that used them to grant credit.

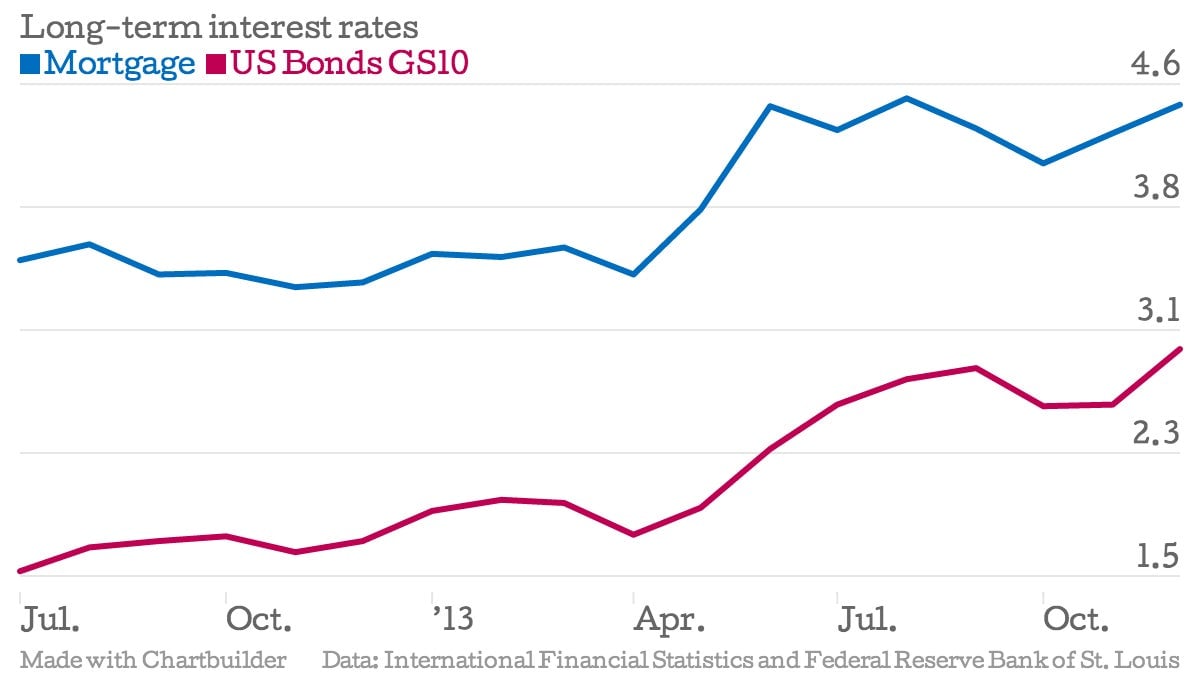

The effectiveness of the Fed in keeping low the long-term rates seems to be waning, however. As shown in the next chart, the long-term interest rates have been increasing as of late (those of the US bonds since June 2012 and those of mortgages since February 2013) even if the short-term rates have been flat and close to zero. The mortgage rate has gone up from 3.4% to 4.5%, and the 10-year US Treasury bond rates from 1.6% to 2.9% since those dates, reversing the trend these rates had shown since the beginning of quantitative easing at the end of 2008. That was embarrassing. Quantitative easing was not able to keep the long-term interest rates low. Maybe it was time to quit before this became too obvious.

But, why did the long-term interest rates increase while the short-term ones remain so low, particularly at a time when the banks are full of liquidity and could increase the supply of credit at a snap? One obvious answer is that the long-term market is expecting an increase in inflation rates. That is a good reason to stop quantitative easing, maybe better than the assertions of its complete success.

Thus, perhaps nothing has happened after the Fed announced the end of quantitative easing because the program didn’t do anything except unnecessarily increase the liquidity reserves of commercial banks and help to keep the long-term interest rate low in the first few years of the program—something that recent evidence suggests it can no longer do.

Of course, the fact that to this date nothing has happened does not necessarily mean that nothing will happen in the longer run. The problem will not come from the amount of money in circulation. The banks have enough excess reserves to submerge the world in currency. Yet, if the interest rates keep on increasing, and everything suggests that they will keep on doing it, many activities that have been profitable at the low interest rates will fail, and this will negatively affect the financial system. Depending on the magnitude of the adjustment, the coming event will be just financial turmoil or a full fledged financial crisis.

Now, you can ask yourself, why getting into all this, risking inflation and financial turmoil just to have money parked in the Fed? Well, keeping the banks artificially liquid may be useful to keep insolvent banks artificially alive. Maybe this was the secret purpose of quantitative easing. Maybe the idea was to keep them liquid while they cleansed their bad loan and investment portfolios. However, for most of the life of the program, the monetary authorities have insisted that the banks were quite solvent.

Were they? Are they? We are going to know the answers to these questions now that tapering seems to have started in earnest. The end of quantitative easing is like the end of Neverland. Only those who learned to live in the real world of free interest rates, as opposed to the fictional lands of artificially low interest rates, will survive. As Warren Buffett said, “Only when the tide goes out do you discover who’s been swimming naked.”