It’s not even Chinese New Year yet and the hongbao are already humming. (During Chinese New Year and certain special occasions, Chinese people use hongbao, or ”red envelopes,” to give money to relatives, employees and friends.) But the hot item in the Year of the Horse isn’t a paper envelope; it’s the “New Year Red Envelope” app launched on Jan. 28 on WeChat, Tencent’s social media app.

The app’s viral success could prove to be a coup in Tencent’s ability to charge WeChat users. That’s also probably why Bill Bishop, an expert in Chinese tech companies, calls the app “Jack Ma’s nightmare,” referring to the founder of Alibaba, one of China’s biggest e-commerce sites.

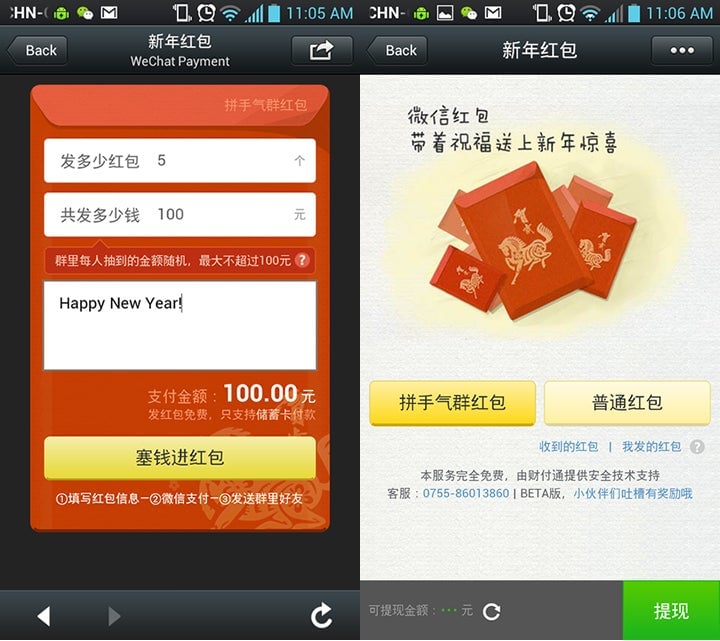

It’s not just that Tencent’s app is more fun to use than Alibaba’s similar app. According to Tech in Asia, unlike Alibaba’s hongbao app, WeChat’s offering allows its users do more than simply exchange money. It also lets users send a lump sum to a group of friends, which the app disburses in five random amounts.

Say a user sends $50 to a group of eight friends. One might end up with $28, while four others get smaller sums, and three get nothing. Letting the app pick a windfall winner and a slew of losers creates a gambling-esque suspense, stoking the sort of emotions that encourage more spending.

But Tencent’s real coup is subtler still. In order to send or receive money in the hongbao app, users have to link up their bank accounts to WeChat. And not just people who want to send money; any of the sender’s friends who want to be in the hongbao running have to sign up their bank accounts too.

This is already bringing in droves of new users for WeChat’s in-app payment service, as the blog Tech in Asia points out. The next time they consider making a purchase in WeChat, they won’t be deterred by the tedium of entering in all that bank account info. And that’s a big deal. Amazon $AMZN and iTunes have long demonstrated the zillions to be made from dissolving the barriers between customers and their online impulse buy.

So, for that matter, has Alibaba, whose e-commerce empire is anchored by Alipay, far and away the most popular third-party payment platform in China. The enduring worry for Alibaba is that it lacks social media channels to encourage even more spending. Against the backdrop of WeChat’s surging popularity, Alibaba took a $586-million stake in Sina last year—perhaps unwisely—in a bid to broaden its social media channels. Alibaba is now squaring against Tencent more directly, launching a trio of mobile games.

Granted, Tencent has a long way to go before it rivals Alibaba’s e-tail dominance. As shareholder Yahoo’s Jan. 28 earnings revealed, Alibaba’s Q3 2013 revenue leapt 51% from the previous year, hitting $1.8 billion (because it’s not public, there’s a quarter delay in its audited financial reports). In the very least, WeChat is giving Alibaba a run for some of that money.