What if the government accidentally invented a new industry?

That’s about what happened in 1978, when a US tax bill focused on cutting middle-class taxes also created a new provision of the US tax code, section 401(k), that would become one the most widely-used retirement plans for Americans and create a $4 trillion wealth-management industry. There’s just one little problem: For all the big changes section that 401(k) wrought on American society, more than half of US retirees’ haven’t saved enough to continue their normal lifestyle when they’re done working, even when added to Social Security’s public pension payments.

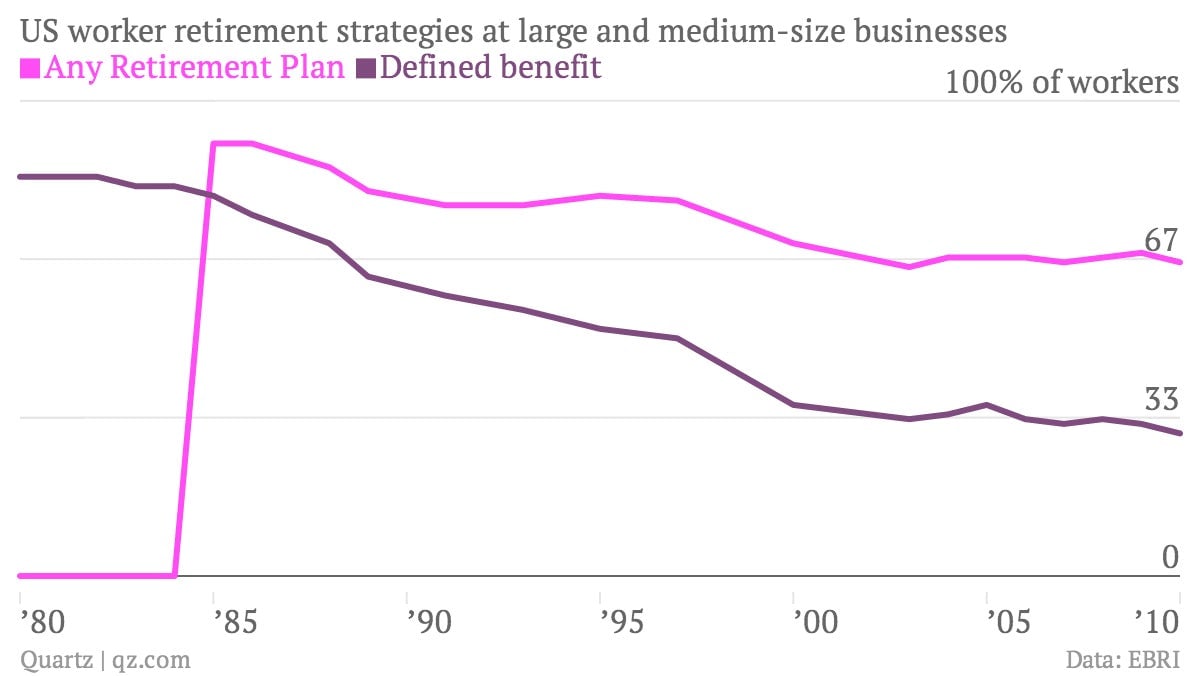

Bloomberg Businessweek found Richard Stranger, the young government lawyer who wrote the provision some 35 years ago, and traced out the consequences, which you can see in the chart below—the end of the traditional “defined-benefit” pension, where employers guaranteed retirement pay-outs to their workers, and the switch to retirement plans such as the 401(k) and the Individual Retirement Account that guarantee a certain immediate contribution but make no promises in the long-term:

The result, besides providing an opportunity for businesses to avoid promising a regular retirement pension, was to put more of the onus on workers to save. Meanwhile, the fees charged by the private wealth managers of these tax-advantaged retirement funds has eaten into workers’ savings; an average two-earner family can pay $155,000, or nearly a third of their investment returns. For these reasons, another official involved in the creation of the law interviewed by Businessweek said “there are certainly times when I think it may have been a terrible mistake.”

What, if anything, is to be done? Last week, President Obama rolled out a pilot program called MyRA—a broader effort to make retirement savings an opt-out feature of the workplace—while others advocate the more direct (and less politically palatable) approach of increasing Social Security payments.

Without broad consensus in Congress, the onus will be on individuals and financial educators to encourage responsible future planning—unless lawmakers in Washington accidentally create another economy-shifting retirement option sometime soon.