In May 2013, Google soft-launched a straightforward scheme for sending money to other people. It lets you connect Gmail with a Google Wallet account and send money to a friend for free (from a linked bank account) or for a small fee (from a credit card).

In May 2013, Google $GOOGL soft-launched a straightforward scheme for sending money to other people. It lets you connect Gmail with a Google Wallet account and send money to a friend for free (from a linked bank account) or for a small fee (from a credit card).

While the service has been available since last summer to anyone who had a Google Wallet account or had already been sent money via Gmail, Google now seems to be starting to push it out to the broader public. (The company declined to comment for this article; in May it said the rollout would happen “over the next 18 months.”) I seem to be one of the earlier people to have been offered the new feature unbidden, as a promotion in Gmail, and it provides a glimpse of how Google plans to pitch its e-money service to the masses.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

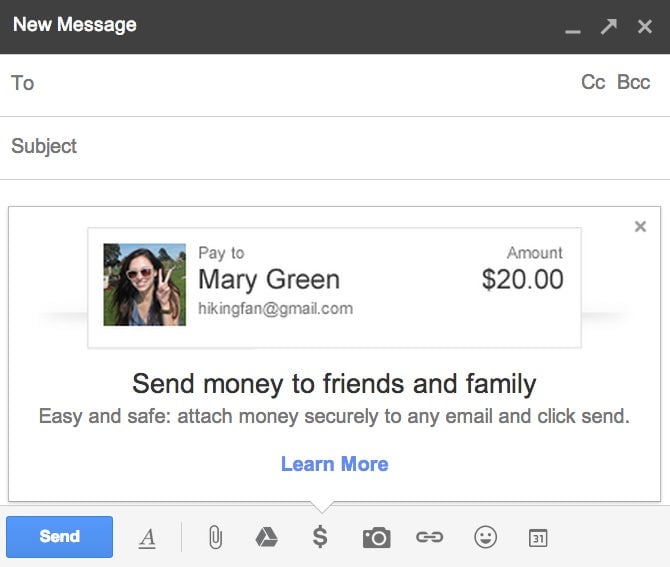

Here’s a screenshot of the all-important process of first contact and initiation for new users, most of whom will almost certainly never have heard of the service:

Once a person has signed up, that little dollar sign at the bottom of Gmail is—on the desktop version of Gmail at least—a permanent feature. (If you’ve signed up and don’t see it, it’s under the “+” symbol on the same bar as the “send” button.)

Here’s what’s brilliant about offering the ”send money” feature: Google almost certainly doesn’t care whether you use it to send money. What it cares about is getting you to sign up to Google Wallet and capture your bank account and credit-card information. And it’s using Gmail, which has a reach comparable to that of Facebook $META—425 million as of June 2012, the last time Google released numbers—to do it.

That allows Google to leapfrog many of its competitors in payment services, like Square $SQ, Venmo and PayPal $PYPL. None of them owns an enormously popular email platform on which to advertise the service and into which it can be integrated. PayPal, the biggest e-payments service, has 143 million ”active” accounts.

The company really in Google’s sights, though, may be none of these, but rather Apple $AAPL. It currently has more active accounts than any other payment processor on the planet—575 million in total, thanks to the popularity of iTunes and the iOS app store. That’s led to speculation that Apple could become a player in payments in general, not just for Apple products—even in retail, and perhaps in the form of an Apple credit card.

The long term play here for both Google and Apple is obvious. First you get users to hand you a link to your credit card or bank account. Then you start multiplying the ways they can use your software and hardware to pay for things and send money. If either company can make even a tiny margin on those transactions, they can tap a whole new revenue stream. And they’ll then be in position to do what Square and others have been trying to do—take a bite out of the entire global credit-card payments system, with its trillions of dollars in annual transactions.