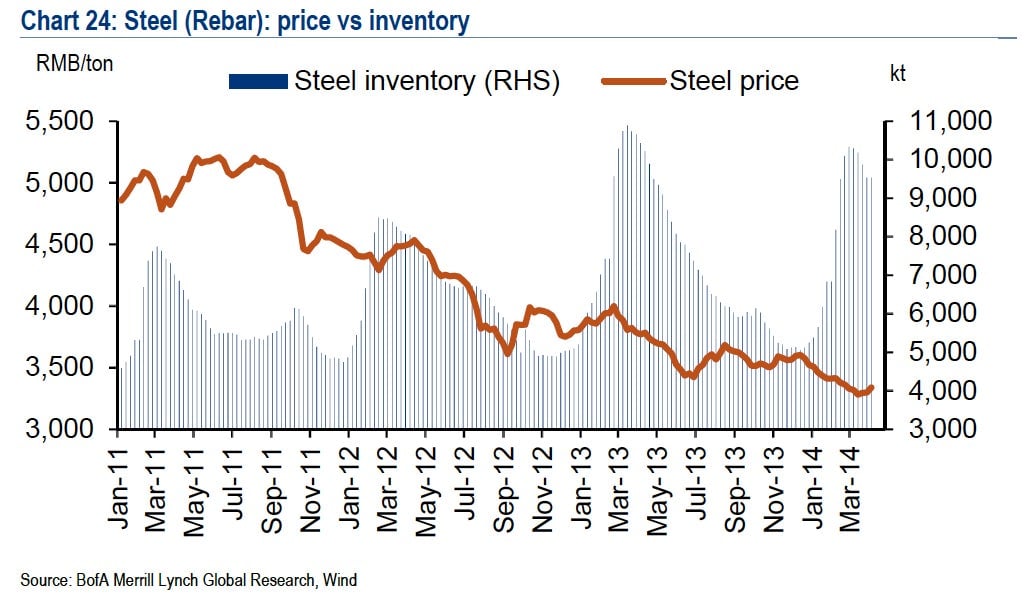

In its boom years, China’s status as the world’s biggest steel maker was an emblem of its industrial might. Now, it symbolizes the dangers of dried-up demand. The sector posted 3 billion yuan ($484 million) in losses in the first two months of 2014 alone, according to Caixin, leaving cash-poor steelmakers scrambling to cover their debts.

In its boom years, China’s status as the world’s biggest steel maker was an emblem of its industrial might. Now, it symbolizes the dangers of dried-up demand. The sector posted 3 billion yuan ($484 million) in losses in the first two months of 2014 alone, according to Caixin, leaving cash-poor steelmakers scrambling to cover their debts.

And they’ve sure racked up a lot of them—3 trillion yuan ($484 billion) worth (link in Chinese), in fact, according to the deputy director of China’s industry ministry. Bank loans comprise 1.3 trillion yuan of the total, and the rest is shadow finance (credit issued off bank balance sheets). Banks are getting nervous: Shanghai courts handled 3,700 steel dispute lawsuits in 2013, 5.5 times more than in 2012 (link in Chinese).

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

What’s happening in China’s steel industry illustrates not only how painful the economy’s inevitable slowdown will be, but also how the country’s complicated tangle of debts are straining the connective tissue of supply chains, endangering the whole system.

China’s largest private steelmaker, Highsee Iron and Steel Group, is a good example. Highsee has shuttered five of its six steel furnaces due to disappearing demand, reports Caixin. That will make it hard for the Shanxi province steelmaker to pay its debts, which are reportedly between 15 billion yuan and 20 billion yuan. It owes Minsheng Bank—a mid-sized bank known for risky lending—more than 3 billion yuan, says Caixin.

Part of the problem is that Highsee itself is owed a lot of money, just like the banks. China’s steel glut has forced steelmakers to extend credit when clients fell behind on payments. Voiding those contracts would risk scaring away other traders. It would also mean holding inventory, making it harder to convince creditors that its business activity make it a good candidate for future loans.

Highsee also reflects another industry trend: diversification. As Caixin reports, company chairman Li Zhaohui has invested heavily in banks—including Minsheng—as well as securities firms and recreational centers.

Whether because of the abundance of cheap credit or a calculated shift away from steel, nearly all of the 32 listed steelmakers have built out non-core divisions, reports the 21st Century Business Herald (link in Chinese). Some, like trading and logistics businesses, are steel-related. Others—notably finance, property and Fushun Special Steel’s diner subsidiary—clearly aren’t.

In some cases, diversification makes a lot of sense. But steelmakers’ involvement in sectors as risky as shadow banking and real estate also exemplifies how fine threads of credit bind Chinese banks, industry and asset markets more tightly together than it might appear at first glance. So, if worsening steel demand forces Nansteel’s real estate subsidiary to free up cash by unloading projects, for example, falling prices could hurt other developers, many of which owe banks billions. Or if shadow banking defaults erupt, Valin Steel’s or Baosteel’s trust company could face big losses—and cause banks to have to pay higher rates on their own trust products. Meanwhile, financial service companies hold significant shares of steelmakers.

State-owned steelmakers can rest assured that, whatever the source of losses, local governments will pressure banks to let them keep rolling over debts. Not Highsee. ”The government has been preoccupied with consolidating local coal miners,” a source close to the provincial banking regulator told Caixin. “It hardly has the time for saving a steelmaker now.”