Here’s a tip for those who like to predict corporate takeovers: Look for companies where the chief executive is turning 65.

Here’s a tip for those who like to predict corporate takeovers: Look for companies where the chief executive is turning 65.

Not 63, mind you. And not 67. The magical moment for mergers is specifically the traditional retirement age of 65.

A new paper (pdf) coauthored by , associate professor of finance at Stanford Graduate School of Business, finds that even a two-year age difference has a striking impact on the likelihood that a company will be acquired.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Firms with a 65-year-old at the helm were almost 40% more likely to get an acquisition offer than firms with a 63-year-old in charge. They were also more likely to be acquired.

Does that mean that the 65-year-olds are just selling out their companies, hoping to grab one last big bonus before they move on to golf and piña coladas? Are they putting their interests ahead of shareholders?

That’s the other big surprise. If there is a problem for shareholders, Jenter thinks, it’s not that the retiring CEOs are too eager to sell; it’s that the younger CEOs, many of whom may have just reached the pinnacle of their careers, are too reluctant. They have too much to lose.

“Everybody intuitively thinks that the older guys must be doing something wrong,’’ says Jenter, who collaborated with Katharina Lewellen of Dartmouth’s Tuck School of Business. “But we have no evidence whatsoever that the deals by 65-year-olds are bad deals. Their deals look as good as the deals by the younger guys. So the real question is, why aren’t the younger guys doing more deals like this? From a shareholder perspective, I really like the older guys.”

It’s worth noting that the soon-to-retire CEO isn’t necessarily the person who initiates the company sale. Jenter suspects that the initiative often begins with investment bankers and companies on the prowl for acquisitions. The aspiring dealmakers consciously look for companies where the CEO is at retirement age, because those CEOs have less to lose and will put up less of a fight.

“I’ve discussed this with investment bankers, and they say it’s obvious to think about retirement incentives,” Jenter says. “They look at a younger CEO and say that would be a messy takeover fight.”

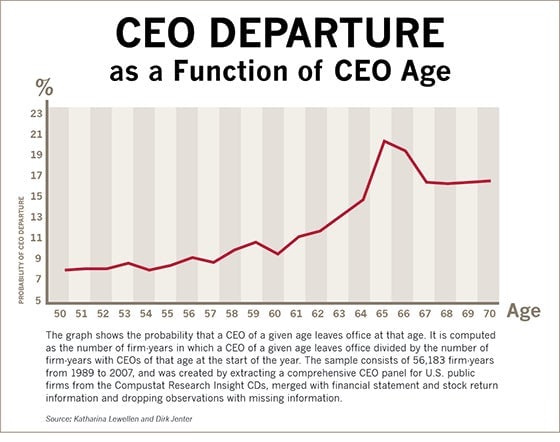

One surprise in the study is that 65 is still such a pivotal year for CEO retirement. All people are living longer, and successful people are especially likely to remain active and healthy long after they turn 65.

But the researchers found that 65 is something like a fish-or-cut-bait moment for many executives. If they are thinking of retiring, that’s the age at which they often do it. The CEO’s likelihood of retiring spikes up very sharply—from about 13% for those at age 63 to almost 21% for those at age 65. For those who hang on past 65, the likelihood of retirement drops back to about 17%.

That retirement spike, specifically at age 65, was what initially motivated Jenter and Lewellen to see if they could find a link to merger activity.

The study has fascinating implications. Consider “golden parachutes,’’ those huge bonuses that go to executives in the event that they lose their jobs because of a merger. Though golden parachutes are often criticized, their purpose is to offset a chief executive’s natural inclination to oppose any takeover bid, even if it benefits shareholders, because it threatens his or her job.

Looking at the age-65 effect, though, Jenter thinks that golden parachutes should be bigger for younger CEOs and become smaller as they age. A CEO who is already likely to retire won’t have as much to fear from a takeover and won’t need as big a counter-incentive.

Jenter’s broader interest is about the role of individuals in corporate decision making. It’s never been a secret that executives have vested interests, separate from those of the shareholders, but the standard models of management have assumed that executives faced with the same financial calculations will make similar decisions.

Jenter looks at decision making in a more personal way, and often comes up with unexpected findings.

In a separate paper, for example, he and a colleague looked at the pattern of CEO firings. They found that executives were much more likely to be fired during industry-wide downturns. That goes against the standard theory of management, which holds that executives shouldn’t be judged on the basis of things they can’t control. If the entire industry is hurting, a company’s bad performance may have nothing to do with the CEO’s abilities.

Jenter says he still isn’t sure about the reason for seemingly illogical behavior. It could be that corporate directors become irrational during bad times and become swept up by the gloom around them. It could be that a CEO’s weaknesses become more apparent in a downturn.

But Jenter suspects that the real explanation is more intriguing. He observes that the CEOs fired during industry downturns are predominantly from firms that were performing worse than their industry rivals. This suggests that the firings may have been justified. The problem may not be that companies are too quick to fire during bad times. It may be that they were too slow to do so in good times.

“It’s possible that boards aren’t paying enough attention when things are going well,” Jenter says. “Maybe there aren’t enough firings in good times. My interpretation of the evidence is that boards are kind of asleep in good times and wake up in the bad times.”

This piece was originally published by Stanford Business and is republished with permission. Follow them @StanfordBiz.