A spate of ponzi schemes has come to light in recent years. All of them typically involve legal wrangling with regulators, public assurances by company officials that they are being unfairly targeted and every investor will get her money back, and eventually, the inevitable happens—hapless millions are parted with their life’s savings.

A spate of ponzi schemes has come to light in recent years. All of them typically involve legal wrangling with regulators, public assurances by company officials that they are being unfairly targeted and every investor will get her money back, and eventually, the inevitable happens—hapless millions are parted with their life’s savings.

The recent bust-ups include Sahara, Saradha Chit Fund, Rose Valley Hotels and Entertainment and most recently, PACL. In an order against PACL, the Securities and Exchange Board of India (Sebi) estimated that the company had managed to collect close to Rs 50,000 crore ($8.27 billion) from investors.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

A Ponzi scheme is essentially a fraudulent investment scheme in which money brought in by new investors is used to pay returns to existing investors.

Most of these Ponzi schemes were running what Sebi calls a collective investment scheme, though they tried to portray it as something else.

PACL, for instance, told people they were actually buying rights to a plot of land when they deposited money with the company. When they wanted the money back, the company would sell the land. But apart from this underlying fiction, it worked very much like a place you could walk in and deposit money for a high return.

These Ponzi schemes managed to raise thousands of crore over the years. How do these schemes collect such large sums of money? A June 2011 report in The Economic Times had estimated that PACL had managed to collect Rs 20,000 crore ($3.30 billion) from investors at that point of time. This means that since then the company has managed to collect Rs 30,000 crore ($4.92 billion) more from investors. An April 2013 report in Mint, quoting state officials had put the total amount of money collected by Saradha group at Rs 20,000 crore ($3.30 billion). Sahara is returning more than Rs 20,000 crore ($3.30 billion) that it collected from investors over the years.

While these ponzi schemes have been ballooning, household financial savings, or the money invested by individuals in fixed deposits, small savings scheme, mutual funds, shares, insurance etc., have actually been declining.

The latest annual report by the Reserve Bank of India (RBI) points out that “the household financial saving rate remained low during 2013-14, increasing only marginally to 7.2 per cent of GDP in 2013-14 from 7.1 per cent of GDP in 2012-13 and 7.0 per cent of GDP in 2011-12 … the household financial saving rate [has] dipped sharply from 12 per cent in 2009-10.”

While the household financial savings have dipped, the money collected by Ponzi schemes has grown by leaps and bounds. What explains this dichotomy? Some experts have blamed the low penetration of banks as a reason behind the rapid spread of Ponzi schemes in the last few years. K C Chakrabarty, former deputy governor of the Reserve Bank of India, in September 2013 had pointed out that only 40,000 out of the 600,000 villages in India have a bank branch.

Hence, investors find it easier to invest their money with Ponzi schemes, which seem to have a better geographical footprint than banks. The trouble with this reasoning is that the bank penetration in India has always been low. So, why have so many Ponzi schemes come to light only in the last few years?

Another explanation is that the rate of return promised by these Ponzi schemes is high and investor greed gets the better of them. This claim needs to be understood closely. Take the case of Rose Valley. The return on the various investment schemes run by the company varied from anywhere between 11.2% to 17.65%. PACL offered returns of 12.5-14% on investments. Saradha reportedly offered returns of 17.5-22%.

It is clear that returns promised by these Ponzi schemes have been significantly higher than the returns available on fixed income investments like fixed deposits, small savings schemes, provident funds etc., which ranged between 8-10%. The lower band of the returns offered by such schemes were not a whole lot higher than fixed income investments. Rose Valley was paying 11.2% on one of its schemes. PACL was offering 12.5%. Also, investment made in fixed income investments like public provident fund and employees provident fund qualifies for a tax deduction, thus pushing up effective return to greater than 10%.

The classic ponzi schemes of course offer much greater returns. Charles Ponzi, the Italian–American con artist after whom the scheme is named, had offered to double investors’ money in 90 days. The Russian Ponzi scheme MMM, which came to India sometime back, offered to grow Rs 5,000 ($83) to Rs 3.4 crore ($562, 567) in a period of twelve months. Speak Asia, a Ponzi scheme which made a huge splash across the Indian media a few years back, promised that an initial investment of Rs 11,000 ($182) would grow into Rs 52,000($861) at the end of an year. This meant a return of 373% in one year. Another Ponzi scheme, Stock Guru, offered a return of 20% per month for a period of up to 6 months.

In comparison, the returns offered by the likes of Rose Valley, Saradha, Sahara and PACL are very low. But investors have still flocked to them. In fact, in its order against PACL, Sebi estimated that the company had close to 5.85 crore investors. Why, indeed, are so many people flocking to such schemes?

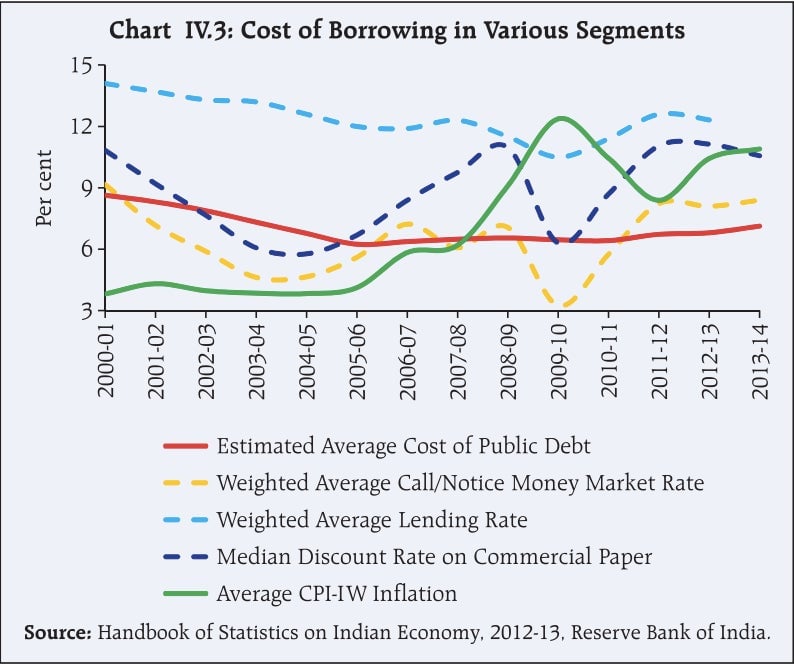

The answer lies in the high inflation that has prevailed in the county since 2008. For most of this period, the consumer price inflation and food inflation have been greater than 10%. In this scenario, the returns on offer on fixed income investments have been lower than the rate of inflation. Hence, people have had to look at other modes of investment, in order to protect the purchasing power of their accumulated wealth.

A lot of this money found its way into real estate and gold. And some of it also found its way into Ponzi schemes.

This is where we need to ask why India’s fixed income instruments offer returns lower than inflation. And the answer lies at the doorsteps of the state.

The government of India since 2007-2008 has been able to raise money at a much lower rate of interest than the prevailing inflation.

How has the government managed to do this? Because India is a financially repressed nation. Currently banks need to invest Rs22 out of every Rs100 they raise as deposits, in government bonds. This number was at higher levels earlier and has constantly been brought down. Over and above this, Indian provident funds like the employee provident fund, the coal mines provident fund, the general provident fund etc. are not allowed to invest in equity. Hence, all the money collected by these funds ends up being invested in government bonds.

As the Report of the Expert Committee to Revise and Strengthen the Monetary Policy Framework points out: “Large government market borrowing has been supported by regulatory prescriptions under which most financial institutions in India, including banks, are statutorily required to invest a certain portion of their specified liabilities in government securities and/or maintain a statutory liquidity ratio (SLR).”

This ensures that there is huge demand for government bonds and the government can get away by offering a low rate of interest on its bonds. “The SLR prescription provides a captive market for government securities and helps to artificially suppress the cost of borrowing for the government, dampening the transmission of interest rate changes across the term structure,” the Expert Committee report points out.

The rate of return on government bonds becomes the benchmark for all other kinds of loans and deposits. The government has managed to raise loans at much lower than the rate of inflation since 2007-2008. And if the government can raise money at a rate of interest below the rate of inflation, banks can’t be far behind. Hence, the interest offered on fixed deposits by banks and other forms of fixed income investments has also been lower than the rate of inflation over the last few years.

This explains why so much money has founds its way into Ponzi schemes, despite not offering outrageous returns. They offer returns that are higher than inflation and that is, naturally, an attractive rate of return. It is through this artificial suppression of interest rates that the government of India has contributed to the success of Ponzi schemes.