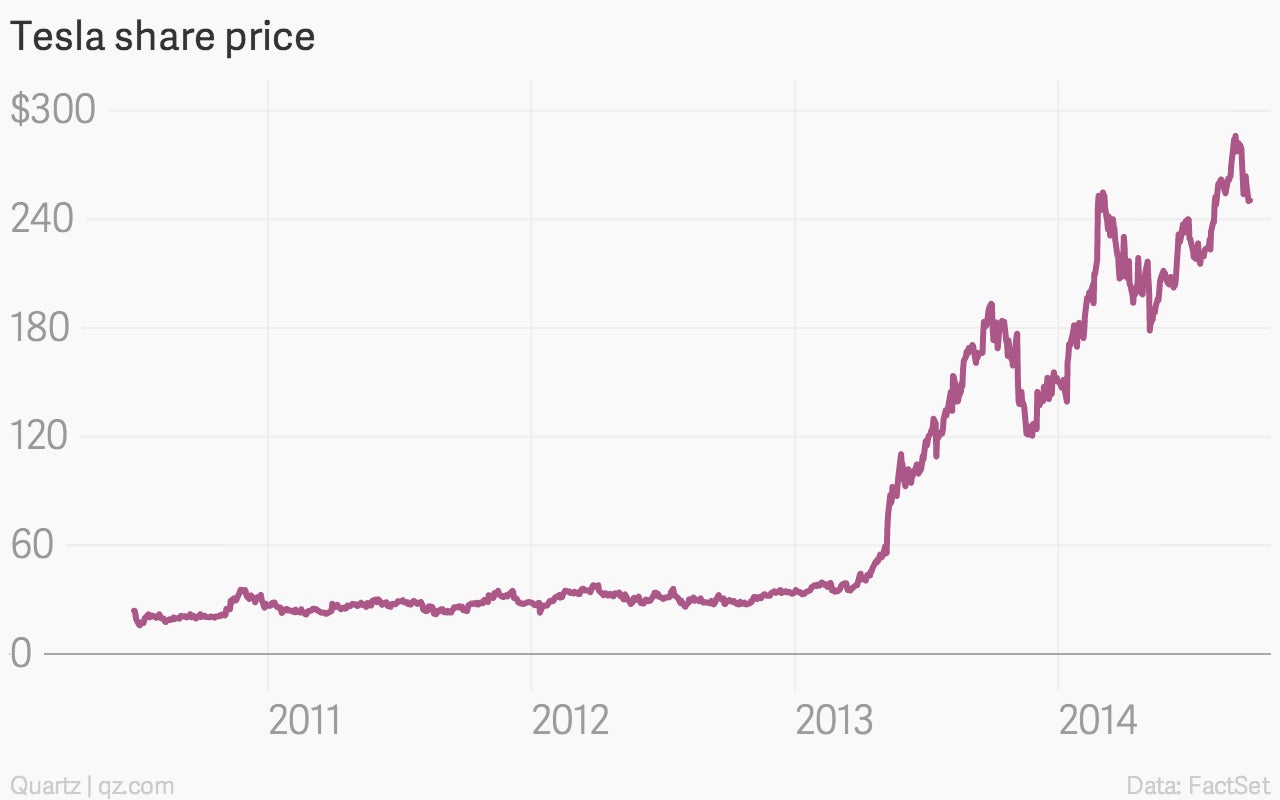

Despite Elon Musk’s warnings about Tesla $TSLA’s meteoric stock rise, the company can do little wrong in the eyes of investors. Though down from its recent all time high of $290, the company is still on a spectacular run, up over 60% this year after rising more than 300% last year:

Goldman Sachs $GS went on a tour of the company’s Fremont, CA factory, and came away confident that Tesla will at least meet its 2014 production goals. But analysts came away concerned that Tesla has a huge list of things it needs to do just about perfectly, according to a note from analyst Patrick Archambault:

What keeps us more guarded is the aggressive timetable of the gigafactory as well as a potential escalation of capital needs given the planned capacity ramp, model and derivative expansion, service expansion as well as other undisclosed projects. So with 3Q likely to be a noisy quarter and shares seemingly baking in flawless execution at present, we remain sidelined for now.

Goldman stuck with a price target of $210.

Having more demand than you can meet is an enviable problem—but one the company needs to solve, given its big future plans. Here are some of the things investors expect Musk and his company to pull off without a hitch:

The big risks are slackening demand, and problems with the gigafactory timing or the Model X launch.

Of the five scenarios that go into Goldman’s price model, the three ”disruptive” upside scenarios model Elon Musk as changing industry as much as the advent of home appliances, Henry Ford $F, and Steve Jobs did.

The “Henry Ford” scenario currently estimates a long term potential share price of $469.