Imagine you’re a doctor and someone hands you the chart of a 60-year-old man, asking you to predict the patient’s health for the next decade. The guy is a probiotic-eating marathon runner and his cholesterol numbers look great. Still, your prediction will likely give more weight to the average health outcomes of sexagenarians than to the patient’s pristine individual health.

Imagine you’re a doctor and someone hands you the chart of a 60-year-old man, asking you to predict the patient’s health for the next decade. The guy is a probiotic-eating marathon runner and his cholesterol numbers look great. Still, your prediction will likely give more weight to the average health outcomes of sexagenarians than to the patient’s pristine individual health.

But when it comes to predicting China’s medium- and long-term growth, economists are chucking that wisdom out the window, argue former US Treasury secretary Larry Summers and Harvard University professor Lant Pritchett in a new National Bureau of Economic Research paper (registration required).

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

As a result, they say, even the more cautious economic forecasts for China are overestimating the country’s growth prospects. Summer and Pritchett’s calculations, using global historical trends, suggest China will grow an average of only 3.9% a year for the next two decades. And though it’s certainly possible China will defy historical trends, they argue that looming changes to its authoritarian system increase the likelihood of an even sharper slowdown.

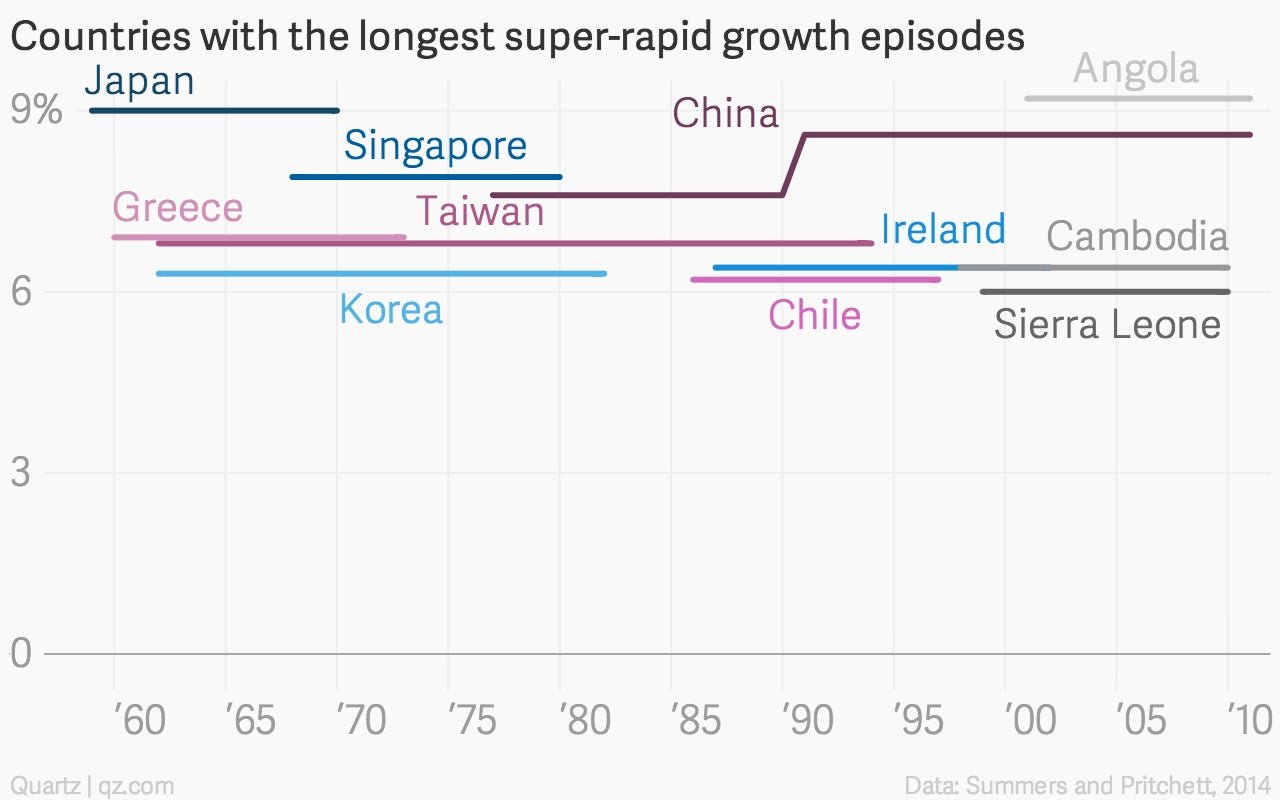

Looking at the predictive power of averages, it certainly seems like China’s time is up. While many countries have experienced what Summers and Pritchett call “episodes of super-rapid growth”—meaning, above 6% a year for at least eight years—they have typically lasted no longer than nine years. China, however, “already holds the distinction of being the only instance, quite possibly in the history of mankind, but certainly in the data” to sustain super-rapid growth for more than 33 years, they write. The country’s streak now stands at 36 years, including the time since the study’s data set ended. Even when you consider “episodes of rapid growth”—meaning GDP growth of more than than 4%—China still takes the crown, beating Singapore’s 30 years at 4.2% growth and Indonesia’s 29 years at 4.7%.

It’s hard to know what drives such periods of unusually high growth, say Summers and Pritchett, because these factors are so rare. Even when economists are able to identify what’s spurring economies, quantifying them in a way that accurately forecasts future super-rapid growth is next to impossible. Yet that doesn’t stop us from believing that our theories do explain China and other countries’ strangely robust growth—and they’ll therefore be able to accurately predict an impending reversal of fortunes.

Of course, this seldom happens. In addition to our failure to anticipate the global financial crisis, we also misjudged the Soviet Union’s economic outlook. And in an example particularly germane to China, in the late 1980s, economists tended to believe that Japan’s industrial policy, high investment levels, and financial repression were propelling its growth. “A decade later, the conventional wisdom held nearly the opposite views,” note Summers and Pritchett.

When periods of rapid growth end, reversals tend to be dramatic. The 28 countries in Summers and Pritchett’s study that sustained eight-plus years of super-rapid growth typically snapped back to the global growth average of around 2.1% a year—a median decline of 4.7 percentage points—and stayed there for quite a while. If a deceleration of that magnitude were to hit China, it would yank its growth rate down to less than 4%.

Though Summers and Pritchett argue that it’s hard to tell what drives super-rapid growth episodes, the economists do note one observable trend: economies where laws bend to favor state-backed firms—guaranteeing them bigger and more secure profits—often boast much higher growth than is typical among countries governed by credible institutions. Investors tend to reward the reliability of cozy state-controlled systems. As long as the government has firm control over these relationships, the lack of rule of law doesn’t much matter; cronyism can be nearly as predictable.

The trouble starts when reforms begin dismantling those relationships, say Summers and Pritchett. This is likely why economic performance usually plunges in countries where democratic transitions follows long periods of robust growth.

You only have to look at Hong Kong to know that “democratic transition” isn’t on China’s docket any time soon. But the political reforms that president Xi Jinping has promised—notably giving more price-setting power to markets and shifting resources away from state-backed enterprises—aren’t so different in their effect.

If these campaigns succeed, they will pry the fingers of the state—and its pet companies—off the economy, shifting control to untested institutions. Xi is also conducting a major anti-corruption crackdown, and it’s as the warp and weft of state corruption begin unravelling that economic growth typically starts getting dicey, according to Summers and Pritchett’s analysis. “While it is possible to envision [China’s] transition [of political power away from organized corruption] not happening for some extended time and while it is possible to envision the transition being made smoothly, neither of these is the outcome typically observed in the data,” they write.

This isn’t necessarily a widely-held opinion. In fact, some analysts cite Xi’s reforms as reasons to expect China to sustain high-speed growth even longer (paywall), as reforms boost efficiency and competitiveness while preserving the Communist Party’s administrative clout. That might turn out to be the case. But Summers and Pritchett make a compelling case that the very reason China’s growth has defied the odds for so is also why it can no longer escape them.