The price of Brent crude oil briefly dipped below the psychologically important $50-per-barrel mark in early trading today, extending its recent rout. And for any suffering oil-producing countries that are hoping that China’s energy-intensive economy might provide some relief: don’t hold your breath.

Analysts at Citigroup $C say that while demand for oil may pick up in China, growth in the country’s oil imports will be slower than usual—just over 3% this year, versus nearly 9% last year. “Anyone hoping for China to drive a rebound in oil prices is likely to be disappointed,” they wrote in a research note.

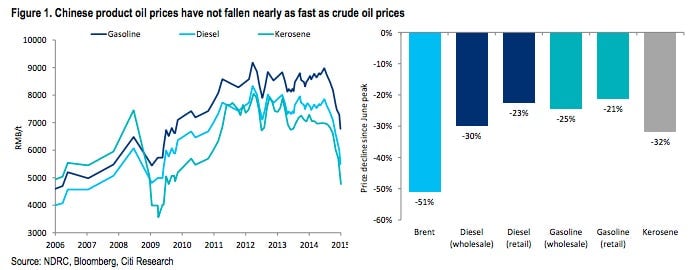

One reason is that China’s oil prices are experiencing a significant lag relative to the global market, due to strategic and commercial stockpiling, along with a slower build-out of refining capacity in 2014. That means that the low global prices aren’t stimulating China’s domestic demand as much as they might have otherwise.

The Chinese government is ultimately responsible for the lag in lowering oil-product prices—unlike in the United States, where lower crude oil prices have quickly translated to lower prices at the pump for consumers. Beijing may be motivated to help the country’s struggling refineries, including those run by state-run oil giant Sinopec. As Quartz reported in 2013 when prices were still high, government controls give state-run refineries a certain amount security in the event of falling oil prices.

Ultimately, Citibank concludes that lower prices will benefit the Chinese economy to the tune of $112 billion, equivalent to a stimulus of about 1.1% of GDP. But by the time lower prices have their effect, it may be too late for beleaguered oil producers.