Bill and Melinda Gates have taken on some of the world’s messiest problems, funding projects to improve the design of toilets and condoms and even create urine-powered fuel cells. Now, in their annual letter published today, they’re outlining ambitions to tackle another messy sector: banking.

Bill and Melinda Gates have taken on some of the world’s messiest problems, funding projects to improve the design of toilets and condoms and even create urine-powered fuel cells. Now, in their annual letter published today, they’re outlining ambitions to tackle another messy sector: banking.

The central thesis of the letter, which lays out goals for the 15-year-old Gates Foundation’s next 15 years, is of unparalleled progress ahead for the world’s poor. (Last year’s annual letter predicted there would be almost no poor countries by 2035.) As they put it:

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Our big bet: The lives of people in poor countries will improve faster in the next 15 years than at any other time in history. And their lives will improve more than anyone else’s.

Their argument is predicated on advances in agriculture, health—including progress against youth mortality, polio, malaria, and HIV—and access to education, including online courses delivered to children in the developing world via cellphones.

It’s also based on the belief that mobile banking will transform the lives of the world’s poor. They write:

By 2030, two billion people who don’t have a bank account today will be storing money and making payments with their phones. And by then, mobile money providers will be offering the full range of financial services, from interest-bearing savings accounts to credit to insurance.

The Gates Foundation’s focus is on supporting the creation of mobile-money systems over which financial services can be provided. The foundation has previously provided funding to help the spread of the M-Pesa mobile-money service pioneered in Kenya, and invested in bKash in Bangladesh.

“The thing we’re trying to create is essentially a debit card with your cell phone where you have transaction costs for digital transfers under 2%,” said Bill Gates in an interview with Quartz. ”So whether it’s savings or transferring to other accounts or taking out loans, you have that basic capability, and innovators can do educational or agricultural offerings on top of that.”

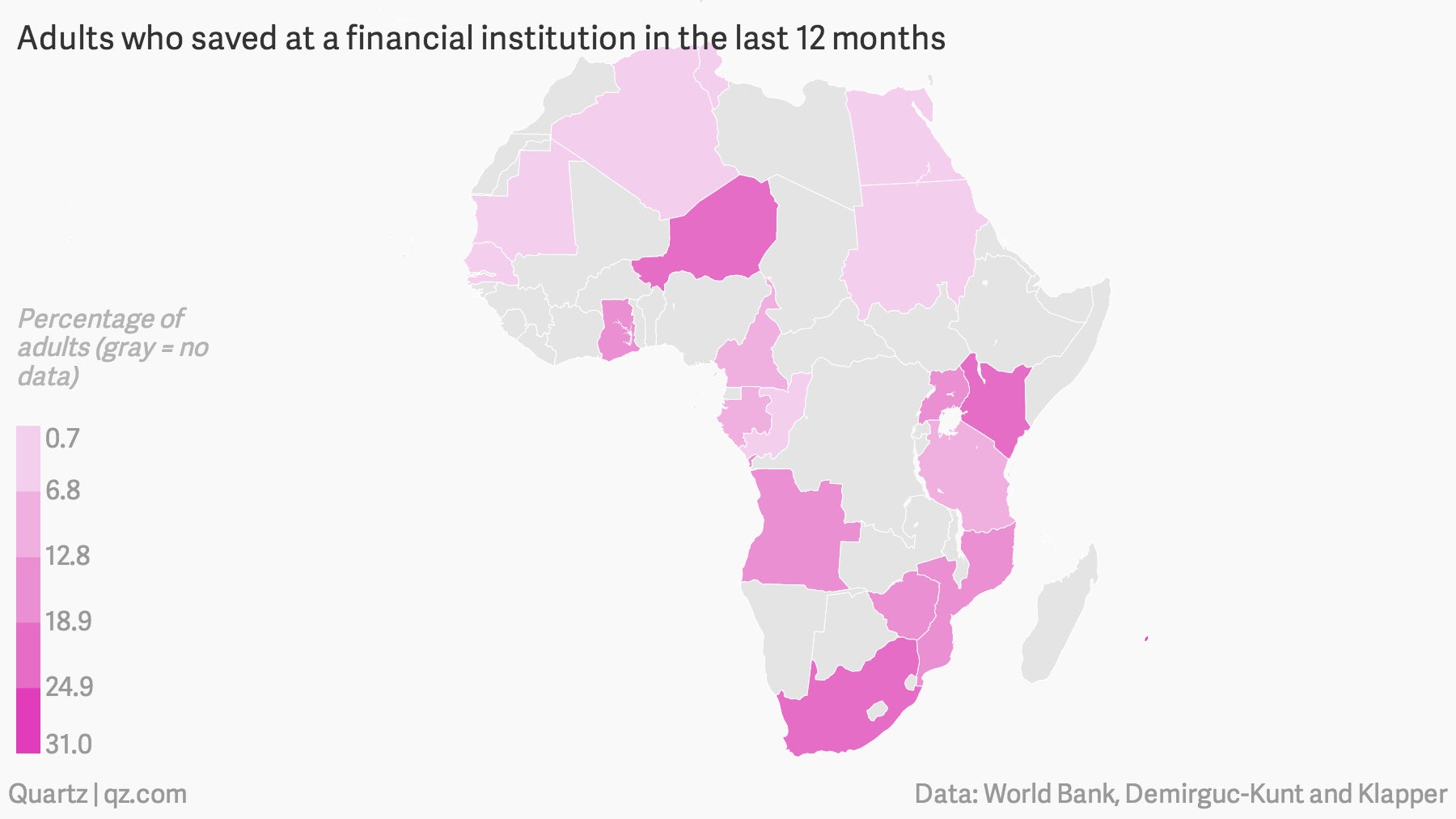

The consumer survey data below for Tanzania from Financial Inclusion Insights show the relatively low usage of traditional banks and high cell-phone penetration.

Having access to savings banks, loans, and cheap money transfers is important for the poor because it allows them to better weather financial shocks—brought on by poor growing seasons, for example—that make it hard to feed their families, get health care, or educate their children.

“It’s the savings piece that we saw as so fundamentally key in this, that people can make these micropayments in their own accounts where they’re saving money,” said Melinda Gates. ”Then when they go through these hunger seasons that happen every year in Africa, they can tide over in the hunger seasons in terms of buying food. But they really talk about then being able to have the school fees, when it comes time in the fall to pay the school fees, they don’t have to sell a cattle or a piece of jewelry or hope that the money is still around under the mattress.

Roughly 2.5 billion adults don’t have bank accounts, according to the World Bank. Mobile banking can be much more efficient for them than doing all transactions with cash. It’s also more cost-effective for financial institutions, since it’s otherwise not worth the overhead expense for them to handle tiny accounts and money flows.

Mobile banking is a shift in focus from the traditional micro-lending that the Gates Foundation and others have supported in recent decades. Traditional micro-finance—which typically requires a network of staff spread out in rural areas to dispense and manage the loans—has higher transaction costs than mobile banking, and can’t scale to reach as many people. Micro-loans can now be offered more efficiently to more borrowers using the mobile money systems.

It’s also not bitcoin. The Gates Foundation is looking to help fund open payment systems that can connect to other ones and allow companies to build services such as savings accounts on top of them. But they say the systems they’re backing, unlike bitcoin, don’t allow user anonymity and do allow transactions to be reversed in case of errors.

Bill Gates predicts that some of the advances in developing countries will “trickle up” to rich-world consumers. But he’s skeptical that an explosion of consumer finance in poorer countries will give rise to serious rivals to the existing global banks, because regulations in the developed world are a big hurdle. He says that Alipay, the digital payment system from China’s Alibaba, could be a competitor in global digital finance, though.

Gates thinks that technology will reduce the transaction costs for financial services and increase competition for banks throughout the world. It will be easier for consumers to buy specific services a la carte, and harder for banks to justify the expense of maintaining branches.

You can view an extended speech by Gates about the future of banking from October below.