A blogger dared to question the Singapore miracle, and now the prime minister is trying to bankrupt him

The Lee dynasty that runs Singapore has always been touchy about criticism. Like his father, the late Lee Kuan Yew, prime minister Lee Hsien Loong and his People’s Action Party (PAP) have a habit of suing their detractors for defamation or for “scandalizing the court,” leaving many of them in financial ruin.

The Lee dynasty that runs Singapore has always been touchy about criticism. Like his father, the late Lee Kuan Yew, prime minister Lee Hsien Loong and his People’s Action Party (PAP) have a habit of suing their detractors for defamation or for “scandalizing the court,” leaving many of them in financial ruin.

Their latest target is a social worker-turned-blogger, Roy Ngerng, who has been asking awkward questions about the fate of billions of dollars worth of workers’ savings in Singapore’s secretively managed investment fund. In July, Lee’s lawyers argued that 34-year-old Ngerng should pay the prime minister unprecedentedly steep damages of more than S$400,000 (US$282,000) for defaming the prime minister. (Not that Lee really needs the money. The prime minister commands a S$2.2 million-a-year salary, making him the planet’s highest-paid world leader by a factor of four.)

Though Ngerng is the first blogger to be taken to court by Lee or his father for defamation, he joins a long list of opposition politicians, journalists, and political cartoonists attacked for discussing subjects that embarrass the PAP. As he and other bloggers have brought the pension fund into the spotlight, Singaporeans have started asking questions and even demonstrating. They want to know why retirement payouts are inadequate for many despite the unusually large share of their wages the government forces them to save; why their pension funds seem to get back a lower return than the state itself earns on that investment; and why the state investment fund, which the prime minister himself heads, declines to publish detailed numbers. The fund’s opacity makes it impossible to know the answers for sure. But estimates by several bloggers and economists suggest that as much as S$800 billion in reserves managed by the state investment fund may have gone missing.

If quelling these questions was the goal of Lee’s defamation suit, however, it hasn’t had the desired effect. The pension fund controversy continues to hog the spotlight as Singapore prepares for parliamentary elections on Sept. 11. For the first time in history, all seats are up for grabs. Coming on the heels of the 2011 elections—when the ruling party won its smallest victory in history—the PAP faces a small but real risk of losing the exclusive control of the country it has enjoyed since Singapore’s first independent election in 1959.

The PAP will very likely win on Friday. But its inability to extinguish outrage about the pension moneys illuminates a shift now underway in Singapore. As its population ages and Singapore’s economic engines sputter, the PAP’s famed fiscal conservatism increasingly comes at the expense of its citizens’ well-being. And as Ngerng’s story shows—and as the election results may too reveal—those citizens are less and less willing to be silenced.

How Singapore’s pensions work

Funding retirement is ever-trickier in Singapore, where plummeting birth rates and longer life expectancy are causing the population to age at an alarming pace. In 2035, nearly a quarter of Singapore’s population will be older than 65, according to the UN—compared with a world average of 13%.

The engine of retirement savings is Singapore’s Central Provident Fund (CPF), a mandatory savings plan started in 1955. These days, Singaporean workers contribute about 37% of their wages (21% by the individual, 16% by the employer, though the latter ultimately comes out of potential wages). This is the highest contribution rate in Asia (pdf, p.23-29). However, 7% goes toward a special sub-account for health care payments (this plan is in lieu of providing universal health care). Workers can also use a large portion of their CPF savings to buy homes (and to a much lesser extent, to pay for education).

Each year, Singapore residents pony up a total of around S$29.7 billion. Despite the fast clip at which Singapore’s population is graying, contributions well exceed withdrawals each year:

To invest that money, the government channels most of that CPF money to a company called GIC Private Ltd, one of the government’s two sovereign-wealth funds. (It does so by issuing a special type of non-tradable government bond to the CPF board.) GIC invests this money exclusively outside of Singapore.

Those pension savings are by no means small. As of July 2015, they totaled S$290 billion in members’ accounts (pdf)—about three-quarters of Singapore’s annual GDP, and nearly double the amount it held eight years ago. Again, most of this is managed by GIC.

A raw deal for Singaporean savers

Ngerng (pronounced “Gnn-ng”) first began blogging about the CPF in 2012, around the time he noticed the conspicuous number of elderly working menial jobs like cleaning toilets, or scavenging for cardboard to recycle for money.

Though this sort of penury defies popular notions of the Singapore economic miracle, it wasn’t exactly alien to Ngerng. His father was a carrot cake vendor, while his mother worked in a factory and picked up cleaning jobs on the side, eking out just enough to raise Ngerng and his two sisters in a two-room flat in a poor, predominantly Chinese enclave of Singapore. After graduating from National University of Singapore (NUS), Ngerng taught autistic children before entering the civil service, where he worked on HIV awareness. This ultimately led to a job in a private hospital educating clinicians about the stigma of HIV. No longer bound by his role as a government representative, Ngerng started blogging—his way of untangling why, despite his country’s wealth, so many Singaporeans seemed to be slipping through the cracks.

One of the more startling things he found was that despite this uniquely high obligatory savings rate and GIC’s healthy rates of return, Singapore’s pension system fails to provide many retirees with an adequate flow of cash.

One problem is that the rates of return promised savers ignore inflation. The government guarantees a nominal 2.5% per year on savings held in the main CPF account (which can be taken out early to spend on housing and education) and 4% on two smaller accounts earmarked for health care and retirement. It offers an additional 1% on the first S$60,000 saved. Though the government reports a weighted average return of 4% (pdf), calculations from the CPF Board’s data indicate an historical average of just over 3.6% (pdf, p.89).

On the face of it, 3.6% guaranteed return isn’t bad at all. But here’s what happens once the rate is adjusted for inflation:

This complaint isn’t new. Between 1987 and 2011 the rate of return on CPF balances averaged just 1.4% a year (pdf, p. 20) once you account for inflation, according to Mukul Asher, an NUS economist—a sixth of the real rate of annual GDP growth during that period.

But even adjusting for headline inflation fails to capture the rapid rise in the cost of living. Consider that, within a couple of generations, Singapore has gone from being a developing country to one of the world’s wealthiest. Upgrading infrastructure, stores, restaurants, and real estate to fancier versions has jacked up costs across the board.

Home ownership for all

Another core problem is, paradoxically, one of the very things leaders are proudest of: Singapore’s unusually high rate of home ownership.

After Lee Kuan Yew took Singapore’s helm in 1959, he zeroed in on home ownership as a way to foster national allegiance, family, and wealth. Formalized in the “Home Ownership Scheme” in 1964, the government created a sweeping public housing program, through which it develops and sells public-housing flats to residents on parcels from its enormous land bank (more than three-quarters of land is state-owned). It also provides the mortgage for these purchases, pegging “concessionary” interest rates at 0.1 percentage point above the CPF rate of return. Since these “sales” are actually only 99-year leases—the homes will ultimately revert to the government—within a few decades of the lease’s end, these homes will start falling in value.

Lee’s home ownership policy proved dazzlingly successful. By the 1990s, nearly nine-tenths of Singaporeans lived in public housing, the majority of the flats self-owned.

Through its public housing scheme, the Singapore government became realtor, landlord, and banker to its people—and, of course, pension fund manager. This latter role was affirmed in 1968, when the government began letting people use a large portion of their CPF savings to buy public housing flats, extending that right to the private market in the 1980s. Since 2002, 57% of the value of CPF withdrawals have gone toward home purchases, compared with typically less than 40% withdrawn each year for actual retirement.

Unlocking retirement savings for property purchases sent money gushing into real estate. The government then launched a slew of programs (paywall) to boost property values—for instance, building ”executive condos” for Singaporeans too wealthy to want public housing flats but not quite able to afford private-market apartments. The government also scaled back overall public housing construction. Home prices, unsurprisingly, skyrocketed.

Flocks of foreigners drive up prices even more

Then things got even worse. By the late 1990s, the economy was sputtering due in part to the shrinking supply of young Singaporean workers caused by declining birth rates. To boost growth, the government set out to recruit foreign workers. These droves of white-collar foreigners upped demand for housing all the more.

Nowadays, Singapore’s median home price is “seriously unaffordable,” according to Demographia International Annual Housing Survey, at five times the median household income (pdf). That compares with Japan’s 4.4 and the US’s 3.6. (This is all the more remarkable considering most Singaporean households have two earners.)

The problem is not housing prices alone. Singapore is now the most expensive city in the world, according to The Economist—pricier than even Zurich or London. Adding foreigners hasn’t solved the puzzle of how to sustain Singapore’s long-term growth. Yet the PAP is doubling down: its recent economic plan revealed that by 2030, more than half of the nation-state’s population will be foreign, piquing mass outrage. In other words, Singapore’s odds for hanging onto that most-expensive city title are looking better than ever.

Asset-rich, cash-poor

However, there’s a big downside to the government’s long-term initiative to drive up home prices and encourage home ownership. While ultra-high home prices make Singaporeans seem wealthier on paper, many retirees don’t have enough liquid savings to ensure a comfortable retirement—what Hui Wen Tat, professor at NUS’ Lee Kuan Yew School of Public Policy, calls being “asset-rich, but cash-poor.” Property now makes up around 75-80% of Singaporeans’ net retirement wealth (pdf, p.10).

The only way households can benefit from those higher prices is if they sell their homes, either on the secondary market or to the government via its lease-buyback scheme, and either rent or buy a smaller flat. But most Singaporeans don’t want to leave the homes they worked their whole lives to own, says Hui.

“A large majority of [those living in public housing] are one-property owners who are likely to want to retire in their current homes without the need to downgrade to lower quality dwellings,” he says. “Higher property prices therefore represent only paper value without any corresponding real benefits.”

In other words, for the vast majority of Singaporeans who only own one home, the government’s policy of encouraging the use of CPF funds to buy property hasn’t truly increased their wealth.

The infamous ”minimum sum”

There’s one other key reason that Singaporean retirees are cash-poor, though: The government has been locking up more and more of the savings that Singaporeans are allowed to withdraw. The biggest tool it has used to achieve this is called the “minimum sum.” It might sound innocuous, but these two words are a flash-point for outrage in Singapore.

When the CPF was first set up, savers could cash out all their pension savings when they turned 55, whereupon they might invest it in stocks, use some of it to pay for Umrah (a trip to Mecca), or do with it whatever else they wanted.

Then the government began to worry that, thanks to rapidly climbing life expectancy, people would run through their savings before they died, leading them to depend on government support in their final years. So in 1986, the government introduced a “minimum sum”—a S$30,000 threshold would-be pensioners had to have in their accounts before they could withdraw lump sums. It’s from this pool that the government began disbursing monthly retirement income when they turned 65. These days, the minimum sum works this way: a Singaporean 55-year-old can withdraw S$5,000 on or after his birthday, plus any savings in excess of the minimum sum. The rest stays in the account and is invested in an annuity called CPF Life, which begins issuing monthly pension payments when he formally retires.

A first source of disgruntlement is that the government has steadily hiked up the age at which would-be retirees can actually retire. In 1986, when the minimum sum was rolled out, Singaporeans could begin getting monthly payments when they turned 60. These days, anyone born after 1954 has to wait until they turn 65.

But even with those additional years to work toward meeting the minimum sum, many—possibly most—still fall short. Though the government doesn’t release this data on a regular basis, it does say that in 2012, more than half of the CPF members who turned 55 in 2011 and 2012 failed to meet the minimum sum.

And it’s likely much higher now. To adjust for inflation, the government has steadily upped the minimum sum each year starting in the mid-1990s.

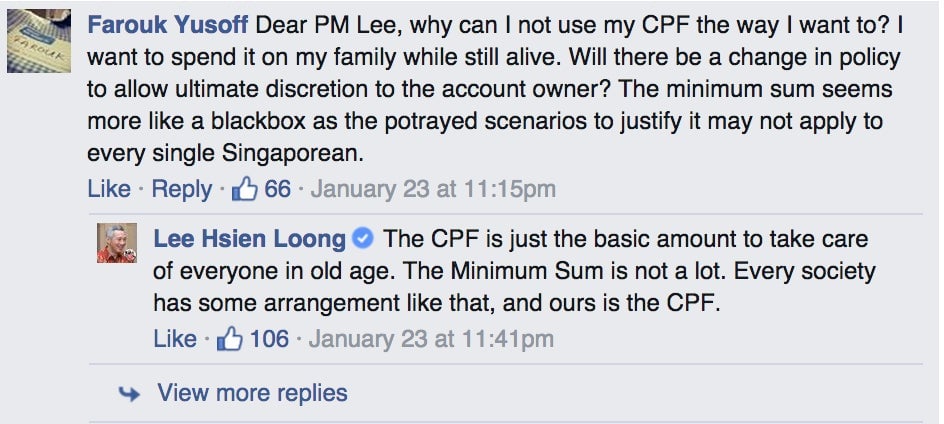

In 2015, it totaled S$161,000. Though that minimum sum is still around three and a half times the resident worker’s median annual wage, in a Facebook $META chat in January, prime minister Lee assured Singaporeans that it’s “not a lot.”

Empty nest eggs

What rankles Ngerng and other Singaporeans is that the government cites inflation adjustment as the reason for raising the minimum sum. (A government debunker of CPF “myths” explains that the minimum sum is arrived at each year by taking the minimum sum in 2003 dollars, adding between S$1,000 and S$4,000 to that 2003-dollars-adjusted amount, and then adjusting that total for inflation—essentially controlling for inflation twice.)

Yet it still refuses to protect the rate of return it offers on CPF savings from inflation or rising living costs. So despite the government’s constant ratcheting up of the minimum sum, more and more seniors find that their monthly income—which includes other sources besides the CPF payouts—isn’t meeting their needs, as you can see from this government survey of elderly and future elderly (i.e. those aged 55 to 64) living in public housing:

That’s even more remarkable given that most older Singaporeans depend on other income sources besides CPF payouts. The previously mentioned government survey found that contributions from children were a bigger source of financial support than their CPF savings. That doesn’t seem likely to change; some two-thirds of Singaporeans plan to rely primarily not on their pensions, but on their cash savings to get them through their retirement, according to HSBC.

It’s unsurprising, then, that more and more seniors are continuing to work in their twilight years.

This brings us to the biggest source of outrage for many Singaporeans: Though the pension payouts clearly aren’t enough, GIC—that’s the government investment fund that manages CPF funds—seems to be making higher returns on pension funds than it actually returns to savers.

How GIC grows reserves

Founded in 1981 for the “sole purpose of managing Singapore’s foreign reserves” (pdf, p.33), GIC has long been a cornerstone of Singapore’s strategy of boosting government savings through prudent management of reserves. Its lone shareholder is the ministry of finance. Since his father, Lee Kuan Yew, resigned in 2011, prime minister Lee has chaired GIC (Lee’s wife, Ho Ching, has been CEO of Temasek, Singapore’s asset-managing sovereign wealth fund, since 2004).

The company declines to state how much money it manages beyond that it’s “well over $100 billion.” Though GIC doesn’t report its annual return on investment, it does publish its 20-year average annual rate of return: 6.5% a year, in nominal US dollars, from 1994 to 2014. Accounting for exchange-rate fluctuations, that equals about 5.5%.

This means that while GIC says for the last 20 years it has earned 5.5% annually, it has paid CPF savers an average of around 3.4%, reinvesting in its reserves the difference between what it pays out to pensioners and what it earns investing their retirement savings.

So for instance, assuming that in 2014 GIC’s investment of the CPF funds returned that 20-year average of 5.5%, it would have kept around S$4.5 billion after disbursing S$9.9 billion in interest. Over the last two decades, this has added up to about S$80 billion, says Chris Kuan, a retired banker who is one of the more prominent commentators on the CPF and government reserves.

Some economists frame that extra money that GIC keeps as a tax on Singaporeans’ earnings. You could also see it as a (rather hefty) management fee, says Christopher Balding, a Peking University finance professor who wrote a book on sovereign wealth funds and has been tracking GIC and its sister fund, Temasek, ever since. Balding says it adds up to a commission fee comparable to what hedge funds command.

However, the Singapore government argues the spread is the consequence of GIC’s taking on all the risk, as Singapore’s deputy prime minister and finance minister, Tharman Shanmugaratnam, explained his remarks to parliament in July 2014:

“[W]hile the Government expects to earn returns through the GIC over the long term that exceed what it pays on SSGS [meaning the special government bond that CPF funds are technically invested in], and has done so in the past, there is no assurance of GIC’s returns exceeding SSGS interest rates over shorter periods, much less every year…. How then is the Government able to meet its SSGS obligations in the years when the markets are weak and GIC’s returns fall below what the Government has to pay SSGS? The reason is that the Government has a substantial buffer of net assets, which ensure that it can meet its obligations.”

This sounds like it makes sense. Then again, CPF funds come with their own reserve base of S$290 billion, which should help plug up any of said shortfall periods. Plus, GIC’s reported rate of return is the average of a solid two decades, says Chris Kuan—meaning, that 5.5% already reflects shortfalls.

“Let’s put it this way,” says Kuan. “If the government were to pay out the returns on the CPF based on the average 20-year rate of return, it’s pretty safe.”

Kuan adds that another problem with the pooling-of-funds-in-GIC approach is that it’s one size fits all. Being forced to invest in a single type of government bond throughout your career prevents the diversification of risk based on an individual’s age and earnings outlook.

“The thing is that if you receive this government bond yield over 35 years of your working life it means that your investment may be risk free—that’s what the government likes to say. But what is risk-free?” says Kuan. “Risk-free is not free of risk of government default. The risk is whether the government pays you enough.”

Sustaining retirees… or the reserves?

It’s true that some of the CPF system’s problems result from the fact that workers simply made a lot less a few decades ago. And of course, you’d expect the government of any country aging at such a fast rate to salt away more money for its swelling throngs of retirees. That might explain why Singapore’s government only pays out some of the returns GIC makes on workers’ savings.

However, the Singaporean government explicitly rejects such pooling of social risk in the design of its pension system. Workers must fund their own retirement—meaning, they are only eligible to receive the money that they put in, plus that average of 3.6% interest (there are, of course, exceptions, such as those who outlive projected life expectancy, and recipients of government top-ups). Instead of spreading the risk of caring for the chunk of any population that will inevitably duck out of the workforce—due to illness or a sluggish economy, or to care for children or return to school—across all members of society, Singapore’s system foists much more of these risks onto individuals and their families.

Unlike many other national pension funds, money isn’t amassed and redistributed so that the poor can count on income to survive. Some might argue this is preferable to systems like the US, where today’s workers fund today’s retiree pensions, an arrangement that aging will soon render unsustainable. That’s not something Singapore’s leaders intend to flirt with. And as deputy prime minister Tharman made clear in his 2014 speech, it’s not the balance of payers and payees that prevents it; rather, it all comes down to how the government manages its reserves.

“Our CPF system is… sustainable, so long as the government continues to run prudent budgets, and invest the reserves wisely,” said Tharman.

In other words, the “sustainability” that Singapore’s officials boast about refers to the government’s ability to pay the obligations it agrees to. Whether the pension system is sufficient to sustain poor, sick, uneducated, and just plain unlucky Singaporeans isn’t at issue.

However, there’s something else illuminating in Tharman’s argument. If growing the reserves is all-important, it’s easier to grasp the government’s reluctance to part with more interest on CPF payouts. The steadily swelling volume of CPF contributions is an increasingly important share of the pool of funds the government—via GIC and other agencies—invests:

The PAP reacts to a peeved public

With Singapore’s media owned or closely tied to the PAP, the task of raising these questions—and looking for answers—has fallen to Ngerng and a handful of other bloggers. Thanks to their efforts, public outrage about the pension fund’s inadequacy has crescendoed in the last year or so. A July 2014 survey revealed that more than half of Singaporeans thought the CPF did not give a fair return. Along with immigration, it is now perhaps the most contentious political issue the ruling party faces as it heads into the Sept. 11 parliamentary elections.

In Feb. 2015, the government announced a suite of changes to the CPF policy. Starting in 2016, savers aged 55 and older will get an extra 1% a year for the first S$30,000 of their CPF balances. It will also grant would-be pensioners more flexibility in when they can withdraw that first lump sum.

Lee’s administration also kept the minimum sum—which it rechristened “retirement sum”—stable for 2016, at S$161,000; it will increase at annual rate of only 3% thereafter. The government also will allow retirees to pledge their homes to meet as much as half the minimum sum, which means they can withdraw cash balances above S$85,000.

Bigger questions loom

However, that problem of the pension payout’s inadequacy is likely to linger. Starting in 2016, someone who has that S$161,000 minimum sum when he hits 55 can count on a modest but manageable S$1,220-1,320 a month when he turns 65. Those who can only meet the minimum sum by pledging their homes will get just S$660-720. That compares with a monthly median wage for permanent residents of S$2,160 (after taxes and CPF deductions).

A genuine effort to help savers would need to do four things, says NUS’ Hui: raise the annual rate of return for CPF funds; protect the CPF Life annuity from inflation; lift the limit on the amount savers can contribute to CPF Life (the annuity’s 4% annual return is higher than that for the other CPF accounts); and bring down property prices.

The last two of Hui’s recommendations are complicated since they could have a macroeconomic ripple effect. However, the government clearly has the means to up the CPF rate and adjust returns for inflation. So why doesn’t it act?

In response, a finance ministry spokeswoman directed Quartz to the following remarks on its site:

“There is also no link between CPF interest rates, and the returns earned by GIC. The CPF Board invests CPF savings are [sic] entirely in risk-free [special bonds] issued by the Government. CPF members receive fair returns as described above, with no investment risk.”

The search for other answers has been taken up by a hodge-podge of bloggers, academics, and opposition politicians. Over time, that investigation has broadened from CPF policy into questions that rattle the very core of the PAP’s strategy for developing Singapore. It’s this hunt for clues and airing of suspicions that landed Ngerng in trouble: Lee argues the blogger defamed him in a blog post that insinuated that the government has criminally misappropriated Singapore’s reserves. However, Ngerng is not the only one with questions about where CPF savings have gone.

Singapore’s secret reserves

To understand why, it helps to have a handle on the Singapore government reserves—or, more specifically, on how they grow. Each year, the government usually runs a budget surplus, collecting more in taxes than it ends up spending on things like teachers’ salaries, defense, transportation, or public welfare. Those surpluses have added up to nearly S$370 billion between 1974 and 2014, according to Peking University’s Balding. However, in the last decade or so, that surplus has more or less disappeared.

On top of that is government debt, which totaled nearly 100% of GDP in 2014. Unlike most other countries, Singapore doesn’t use the money it raises to spend on its people—in fact, its Constitution bans the government from spending funds raised from bonds, or any other reserves. Instead, the Singapore government invests that money as reserves, profiting from the spread between what it earns on those investments and what it owes to lenders—similar to how it does with the CPF money it effectively borrows from its citizens. Paradoxically, Singapore’s minimal fiscal spending has won its sovereign debt the highest rating possible, allowing it to borrow huge sums cheaply and profit all the more.

Then there are land sales, one of the most opaque parts of Singapore’s finances. All told, those sales tallied up to what looks like a little more than S$25 billion a year in both 2013 and 2014 (pdf, p.85).

Much of these surpluses have likely flowed into GIC’s coffers (smaller streams are sometimes given to the central bank and Temasek). But it’s hard to know, says Kenneth Jeyaretnam, an economist and head of the opposition Reform Party. “We don’t have any sense of what they’re doing with the surpluses they make every year, where that’s going, how it’s reinvested,” he says.

At least some of this mystery is intentional. The Singapore government declines to reveal the size of GIC’s reserves—it reports those held by the central bank and Temasek—because it views these as a “strategic asset” and a “key defense for Singapore in times of crisis,” according to the finance ministry’s website, to which a government spokeswoman directed Quartz. This is also a way of discouraging and, should it come to it, combating currency speculation; Singapore’s heavy reliance on trade and foreign business means swings in the currency’s value could shatter the economy. Since a country’s reserves are the ammunition it holds to fight such outflows, the government is understandably secretive about what they’re truly worth.

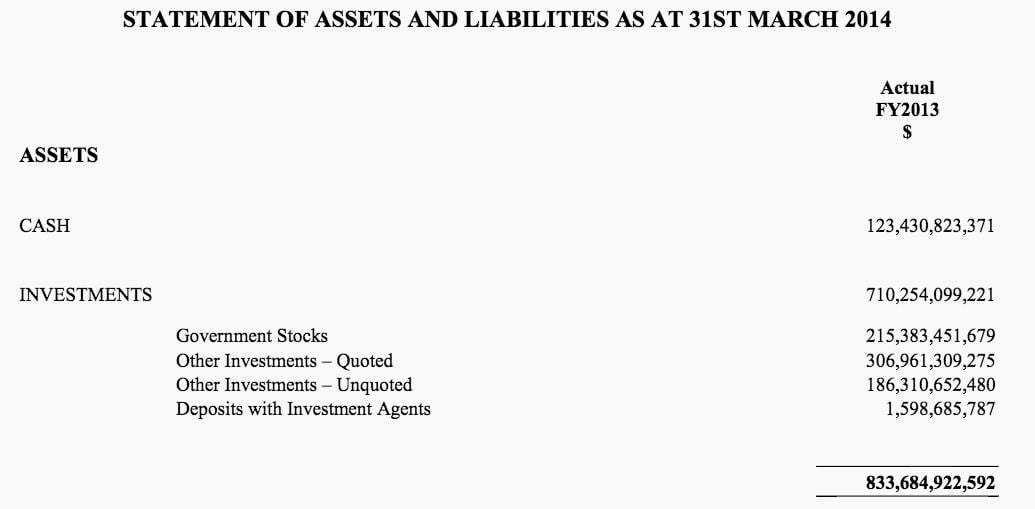

The government’s published data do offer some clues. “Every year the government publishes a balance sheet which is two years out of date even though the Constitution says it should be only a year out of date,” says Jeyaretnam, referring to a single page in the appendix (pdf) of its annual budget.

As of March 2014, it reported S$834 billion in government assets. The lack of itemized description of what “assets” actually tallies makes it impossible to know whether it includes the holdings of GIC and Temasek (due to accounting conventions, it’s unlikely to include holdings of the central bank, though).

The case of the (maybe) missing billions

Here’s where the plot thickens: Jeyaretnam calculates that the Singapore government’s historical accumulations of surpluses implies more reserves than that S$834 billion that shows up in that “assets” column. That jibes with what Peking University’s Balding has concluded. Combing through reams of official data, Balding added up the operational budgets, proceeds from debt sales, and the CPF funds. Using historical rates of return and subtracting interest payments, he calculated that the Singapore government should have amassed nearly S$1.7 trillion over the last few decades—a lot more than that reported S$834 billion.

In other words, many hundreds of billions that should be there, simply aren’t.

Though he cautions that calculations shouldn’t be taken as exact, Balding says the gist still holds.

“We have records on how much money went in, and how much money went out, and how much that money was earning,” he says. “We should come to a reasonable idea of how much money is there. And it’s clearly not anywhere remotely close to what should be there.”

There are a few possible explanations, he adds. Perhaps the government channeled some of the funds into public spending that was never recorded. Or maybe Temasek or GIC—or both—aren’t making the rates of return they report. It’s also possible that some of those reported surpluses somehow didn’t make it to national accounts.

Both Balding and Jeyaretnam also say the funds that seem to be missing may have been lost covering up bad investments. GIC and Temasek both count more than a few disastrous bets littering their histories. For instance, GIC lost upwards of $8 billion on a stake in UBS, while Temasek took a huge bath on investments in Barclays and Bank of America $BAC. That wasn’t necessarily just a global financial crisis fluke; Singaporean blogger Phillip Ang has documented a slew of recent instances of GIC buying at the top.

For its part, the Singapore government responds that its so-called surpluses shouldn’t be considered missing. It seldom actually runs budget surpluses, according to a finance ministry webpage to which a spokeswoman directed Quartz; the surpluses that economists so often cite involve funds that the government is forbidden by the Constitution from spending. A more precise picture of the budget, it argues, should only include revenue that the government is legally permitted to spend.

That’s one interpretation, at least. Chris Kuan, the former banker, has another theory of how the reported numbers add up. The calculations by Jeyaretnam and Balding assume that Temasek’s and GIC’s assets are included in that statement of assets and liabilities—which, says Jeyaretnam, Singapore’s Constitution holds they should be. However, Kuan is skeptical that Temasek’s portfolio is included as part of the S$834 billion listed in the statement. By his calculations, the government’s total reserves (which the Constitution defines as its net asset position) are a little over S$560 billion—GIC manages S$254 billion, Temasek S$266 billion, and the central bank S$41 billion. Kuan notes that untold sums of the reserves have been siphoned off to buy land and other physical assets. Since the finance ministry classifies these as investments, they fall outside the Constitutional ban on spending of reserves, he says.

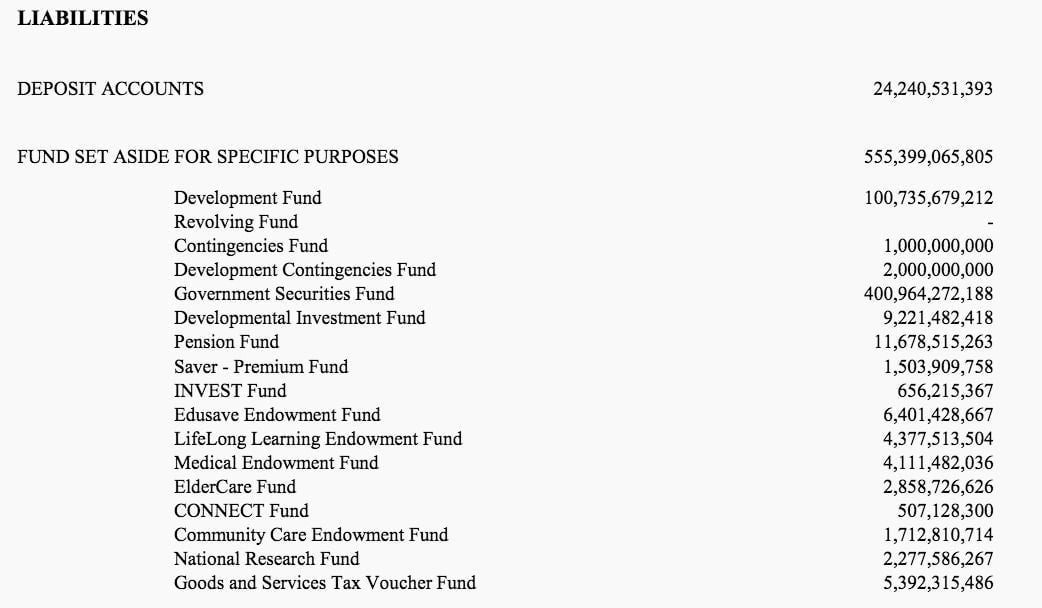

Those mysterious land assets may explain the apparently missing funds. Kuan points to a S$101-billion entry in the liabilities side called the “Development Fund,” which is earmarked for land acquisition and development.

Some of the drawdown of reserves that Balding and Jeyaretnam have documented likely occurs when the government shifts its reserves into this “Development Fund,” says Kuan. Before being spent, those planned investments are perhaps recorded as “liabilities.” (Kuan also notes that expenditures announced as increased social spending for things like community education go into these funds. However, due to the Constitution, only the returns earned on these funds can actually be spent.)

But even if some of Singapore’s assets are “disappearing” into land purchases, says Balding, it would be unusual for such a huge amount of money—as much as S$800 billion, by his calculation—to be invested, even in state projects, without attracting notice.

“Shielded from risk”

In any case, the reserves ultimately lead back to the controversy over CPF rates, says Kuan.

“The way I see, it is kind of a transfer of value from household balance sheets to the government balance sheet through sale of pretty expensive public housing and holding a relatively low rate of return on long-term savings,” he says. ”The government pays what interest rate it would like to pay on the debt. Those rates are always lower than what they can make from investing those funds.”

The government argues this is necessary to protect the pension savings. Last year, deputy prime minister Tharman revealed that in eight of the last 20 years, GIC’s investments returned less than its promised CPF rate—meaning it had to dip into its reserves.

“It is this role of the Government, with its significant net assets, that ultimately allows the… CPF members to be shielded from risk,” said Tharman.

Though Tharman’s “significant net assets” are technically the government’s, they’re also the stockpiled sum of decades of locked-up wages, squirreled-away taxes, and revenue reaped from renting out homes to its own citizens—money households would otherwise have spent or saved as they pleased. The government bears the risk of managing those forced savings when it’s making 5.5% returns; however, should it lose too much money, says the Reform Party’s Jeyaretnam, it’s Singapore citizens that will be left on the hook.

“Singaporeans ultimately have to bear the risks for GIC speculation,” he says. “You know, [if] GIC goes bust, who picks up the tab? Singaporeans have to repay themselves.”

Change on the horizon?

The Singaporean government hoards not just money, but also information—and as a result, the calculations in this article are guesswork, as we have stressed throughout. Official published data are too few and too vague to give much more than a hazy shape of state finances—let alone decisively to confirm or disprove analysis by Balding, Jeyaretnam, and Kuan. (And again, the Singapore government didn’t reply directly to Quartz’s questions on these matters.) However, the fact that such arcane arithmetic sleuthing is necessary to fathom the finances of an advanced economy is startling.

As for Ngerng, a court will announce in a few weeks—after the Sept. 11 general election—how much he must pay the prime minister for defamation. Chances are good that the final bill will drive Ngerng into bankruptcy.

These impending financial straits seem to have little dented Ngerng’s quest for a better deal for Singaporeans. Urged by his blog readers, Ngerng is currently running for parliament on the Reform Party ticket—and he’s even oddly upbeat about the defamation suit fracas.

“I’m just glad that over the past year, because of what has happened to me, it has caused a chain reaction where the government has finally responded to Singaporeans about our CPF,” he says. “The government has made piecemeal changes, and they do not go far enough. But it is a start.”

The essential business news, delivered fresh every morning.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.