China’s biggest economic woe isn’t its stock market, the yuan’s value, or the size of its foreign reserves. It’s simply that Chinese companies are making way more stuff than anyone wants.

China’s biggest economic woe isn’t its stock market, the yuan’s value, or the size of its foreign reserves. It’s simply that Chinese companies are making way more stuff than anyone wants.

This industrial bloat wastes labor and bank credit, spurs indebtedness, and stifles innovation. It makes “rebalancing” toward a sustainable consumption-focused economic model near-impossible. By pushing down prices both in China and beyond, Chinese state capitalism drives businesses everywhere out of business.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Fixing this problem requires ripping apart the system that perpetuates it: the government’s control of the economy through state-owned enterprises (SOEs). But judging by a just-published SOE reform plan, president Xi Jinping isn’t up to this challenge.

The plan (link in Chinese), published on Sep. 13 after months of delays, falls short of encouraging private competition, let alone shifting wasted state assets to entrepreneurs who can make real money off them.

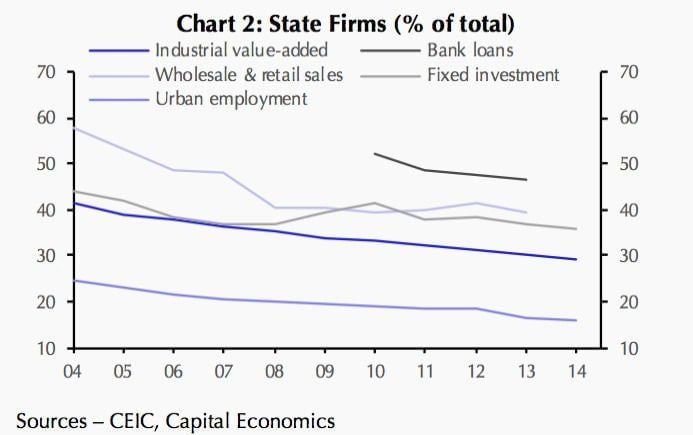

Under the current system, the Chinese government shelters some 75,000 SOEs in “strategic” sectors—e.g. telecom, oil, power, aviation and banking—from private competition. Another 80,000 SOEs operating in unprotected sectors like hotels and real estate also benefit from easy access to cheap loans and land.

Though the state sector’s share of the economy has shrunk, SOEs still gobble up a huge share of bank loans, diverting capital from more innovative private firms. By squandering precious resources and generating less return from them than they should, Chinese state capitalism drags down growth and drives up debt.

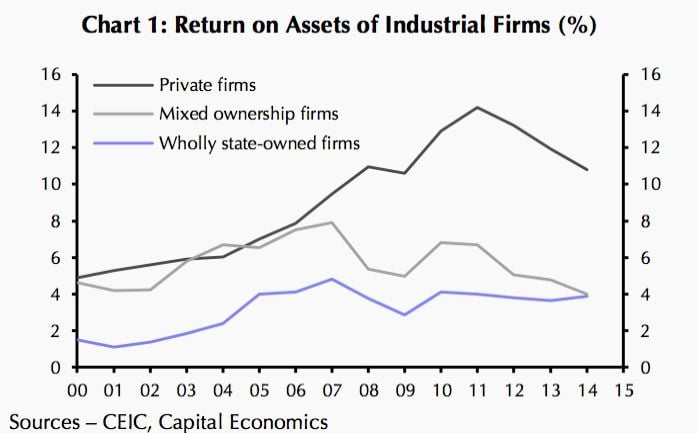

Unsurprisingly, private firms tend to be more profitable than SOEs. So why can’t they compete?

Preferential policies let SOEs hog money and labor without concern for their bottom line. If they sell at a loss, they can always borrow more from state-owned banks. The state also prevents SOEs from failing, creating “zombie” companies kept alive on a steady drip of government support. For instance, when state steel giant Sinosteel tried to file for bankruptcy in 2014, the move was blocked by the government SOE agency’s leaders, reports Caixin (link in Chinese; paywall). Instead, state-owned banks kept on lending to it.

This life support lets SOEs flood the market with artificially cheap goods and services, driving private firms out of business.

And not just in China. The government’s propping up of unprofitable state companies forces down prices around the globe, driving manufacturers everywhere out of business. Until China sheds its slack industrial capacity, allowing investment to generate more returns, the global economy will continue to suffer, Derek Scissors, economist at the American Enterprise Institute, told Quartz.

The solution is—as Xi himself proposed in the agenda-setting third plenum in 2013—to grant the market a “decisive role” in deciding who wins opportunity and resources. Competition for bank credit and other resources would oblige companies to wring much higher returns from their investments. This would add much-needed juice to Chinese growth, and suck the supply glut out of the global economy.

Many economists had hoped Xi would incorporate the ”decisive role” of markets in his approach to reforming SOEs. A promising sign cited was his anti-corruption crackdown, which many China-watchers argue is an effort to cow Communist Party leaders who oppose reform of a system that lets them siphon billions into their own bank accounts.

There is precedent for such change. From 1997 to 2003, the Chinese government shuttered or privatized some 60,000 wasteful SOEs—putting 40 million people out of work—a policy spearheaded by then-premier Zhu Rongji. The threat of being shut down or privatized upped performance of SOEs and galvanized new opportunities for the private sector—an approach that would be effective today, argues Andrew Batson, economist at Gavekal, in a Sep. 15 note. (In a promising sign, current leaders recently consulted Zhu on Xi’s reform plan, reports Bloomberg.)

However, Xi’s reform proposal is aimed at boosting SOE performance through corporate governance—not by exposing SOEs to market forces. In other words, the government, and not the market, will still enjoy the ”decisive role” in allocating resources.

The plan’s twin pillars are encouraging private investment in SOEs and wedging a buffer between SOEs and their supervising agency (which currently appoints top executives, decides asset sales and financing, among other things). Filling this new layer will be ”state capital management companies” (SCMCs) modeled on Temasek, Singapore’s $253-billion state-owned asset manager that uses a Berkshire Hathaway $BRK.B-style approach to its holdings.

The first idea is neither effective nor new, writes Capital Economics in a Sept. 16 note. Thanks to government promotion of “mixed ownership” that began in the early 1990s, four-fifths of SOEs are now partially private-owned—with little improvement in SOE performance.

A bigger problem, though, is that private investors won’t want to take minority stakes in SOEs and state projects, says AEI’s Scissors, citing the government’s so far abortive effort to drum up private investment in rail as an example.

“For the economy, this is as undesirable a reform step as could be taken,” he said. “What the Party is effectively seeking is to prop up SOEs by coopting their private competitors. Not new, still the same terrible.”

As for the Singapore-style asset management plan, it’s unclear what new incentives would encourage SCMCs to put profits over politics. Though tasked with prioritizing financial performance, SCMCs are also charged with protecting China’s national interests.

On the upside, the plan does encourage SCMCs to sell stakes in underperforming SOEs in non-strategic industries, which could allow some privatization, says Capital Economics. However heartening, that twinkle of hope for global growth is nonetheless dimmed by the vast shadow of Xi’s swollen state capitalism.