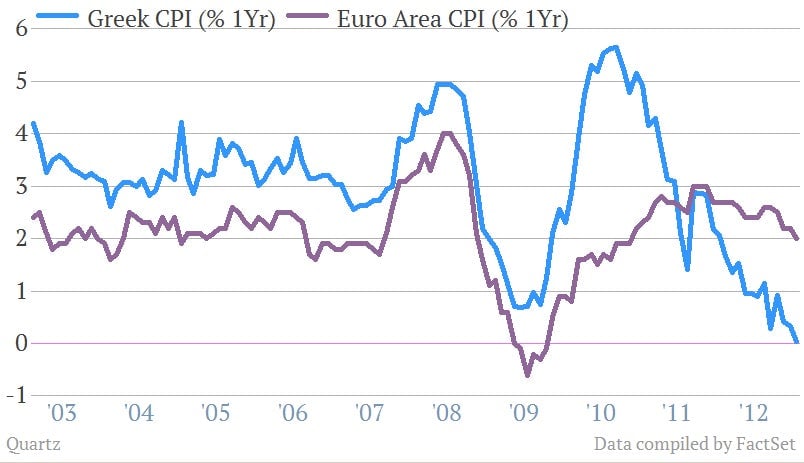

Greece’s consumer prices are the same as they were a year ago, figures last Friday (Feb. 15) showed. Inflation in Greece hasn’t been this low since 1996. Here’s how that compares to the euro area:

Zero inflation might not sound all that scary when you compare it with a 6% GDP contraction for the fourth quarter of 2012 or a 60% youth unemployment rate. But Friday’s data show Greece now teetering on the edge of deflation—something economists generally agree is bad. For one thing, it means people aren’t buying goods, because they lack the money. And though deflation makes things effectively cheaper, it also encourages deferring consumption. With sources of revenue dwindling, Greece needs all the consumption it can get.

Deflation also makes debt more expensive relative to GDP. And that wouldn’t be good. Greece now boasts a debt-to-GDP ratio of 170%, compared with 120%. On top of that, two-fifths of households can’t pay their debts.

Perhaps the biggest trouble with deflation, though, is that once it sets in, it’s extremely hard to shake (see: Japan).

Mind you, the International Monetary Fund saw this coming. In its January report on Greece, it projects “mild deflation” in 2013. What’s more, Greece’s deflation has been part of the plan all along (pdf, p.81):

Large external liabilities ultimately require large trade surpluses in order to service them, and achieving these surpluses requires a more depreciated level of the real exchange rate. In a currency union the depreciation has to be achieved largely through deflation, which necessitates a larger negative output gap…

Translation from IMF-speak: Permitting deflation is the only way to make Greece’s economy sustainably competitive without devaluing the euro.

Translation from abstraction: Instead of making exports competitive by via cheapening its currency (see again: Japan), Greece must achieve this through falling wages and paring down pension obligations. And, lo, another sign the plan is working: Nine in ten Greek households have seen their incomes fall since the crisis began—and, on average, they’ve fallen by 38%.

The IMF report forecasts a Greek recovery starting in late-2013/early-2014, with its current account balanced by 2014. That seems optimistic. Greece’s 2012 trade balance from January up until November was a not-at-all-small deficit of €19 billion. Exports rose 19%, more than the 7% rise in imports (pdf, p. 4). But that’s still going to be a tough gap to close.

Perhaps the worst part about this, though, is that the IMF’s plan is exclusively theoretical and its consequences are untested, as Greg Ip has noted:

[M]ost, if not all, resolutions of balance of payments crises involve devaluation. For Greece to pull this off without devaluation will require a brand new template. It will almost certainly mean almost unimaginable wage and price deflation…. And even if it does happen, it will restore Greek competitiveness far more slowly than a devaluation would, so unemployment will be higher for longer.

If Ip and the IMF are right, then Greece’s bad news signals the IMF’s “deflate it ’til you make it” plan is working. But the thunderhead sitting smack in the middle of that silver lining is that even if deflation balances its trade, Greece still has to get itself out.