The private equity firm Kohlberg Kravis Roberts just put the capstone on its recent Japan hiring spate, appointing turnaround specialist Hirofumi Hirano as its managing director and CEO. That team will have some of KKR’s $6 billion new Asia fund to play around with, reports DealBook.

The private equity firm Kohlberg Kravis Roberts just put the capstone on its recent Japan hiring spate, appointing turnaround specialist Hirofumi Hirano as its managing director and CEO. That team will have some of KKR’s $6 billion new Asia fund to play around with, reports DealBook.

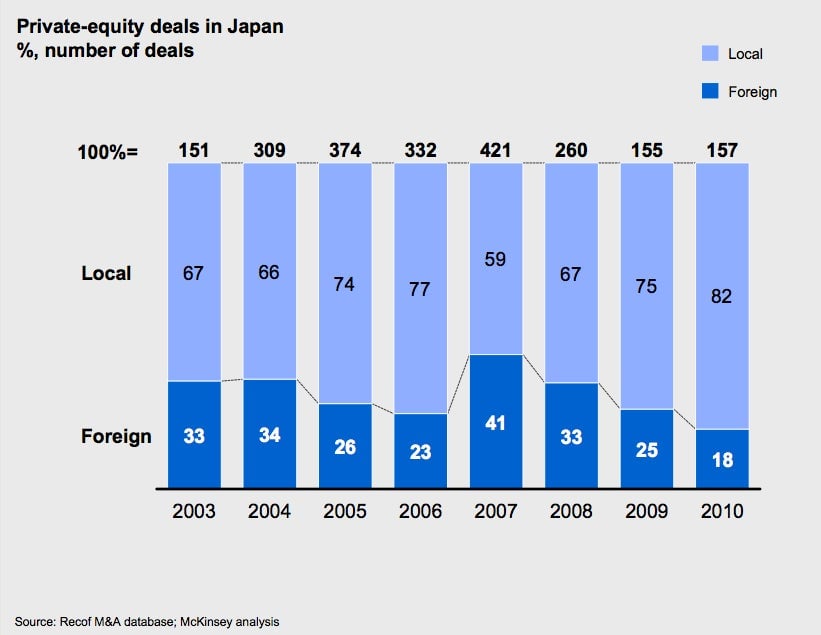

This might seem odd given that Japan’s PE market is notoriously difficult for foreign firms. In its Asia-Pacific private equity outlook report for 2013, Ernst & Young found that Japan tied with China as the toughest major Asian market for acquisitions (pdf). In fact, it’s so unrewarding that some, like Cerberus, have up and left.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

The tough environment is even worse for buyout firms, which the Japanese often refer to as “vulture funds” (paywall), reflecting a widely held distaste for the layoffs that buyouts often require. In addition, the family-run firms that are so common in Japan typically aren’t big fans of ceding managerial control.

And then there’s the fact that Japan’s massive state-backed funds tend to crowd everyone else out. For instance, Innovation Network Corporation can plunk down $19 billion when in needs to, while Enterprise Turnaround Initiative Corporation of Japan can scare up nearly $18 billion, according to Reuters. As it happens, KKR’s failed effort to buy Renesas Electronics, a failed chipmaker, offers one of the most recent examples of this (paywall).

But at least some of KKR’s Japan hiring frenzy can probably be chalked up to the hope that those conditions are changing, thanks to Abenomics, as new prime minister Shinzo Abe’s aggressive economic policies are widely known. For one thing, the weakening of the yen—it has fallen more than 16% against the dollar so far this year—implies that that foreign PE firms’ billions will go a lot farther than they would have, say, a year ago.

And from the perspective of Japanese companies, the surging Nikkei—up 53% since mid-November 2012, when Abe looked set to win—hints that valuations, which the E&Y report cites as a stumbling block in the past, will rise as well. Plus, the public companies that continue to founder might offer another opportunity for PE firms, says private equity firm Carlyle.

Industry experts also expect that, as they search for growth, small- and mid-sized Japanese companies will start looking to acquire in developing markets, exchange rate be damned, and will need PE partnerships to finance those investments and bring experience.

Although it’s not yet clear what government action might prompt reform of Japanese corporate behemoths, one of the core tools of Abenomics is structural reform. If that’s to take place, it will entail consolidation and restructuring—another potential source of opportunities for foreign buyout firms.