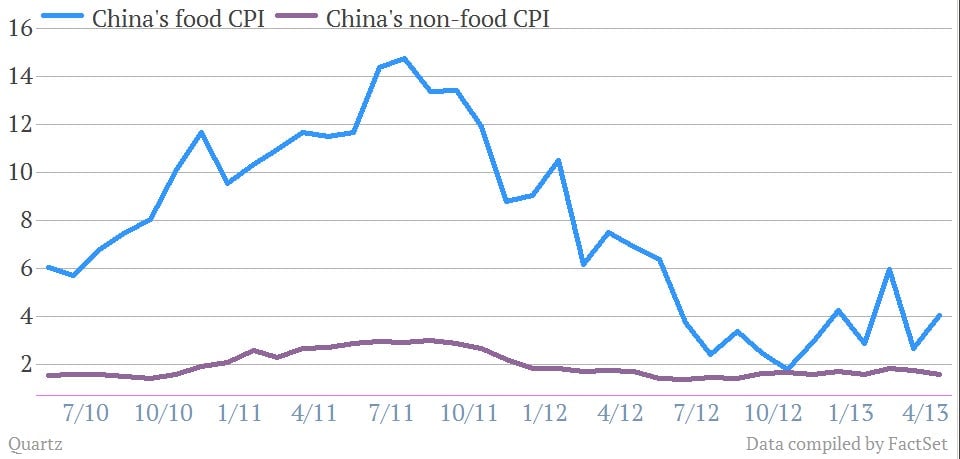

China’s consumer inflation slowly but surely ticked up in April, rising 2.4% from April in 2012, compared with a 2.1% year-on-year increase in March. That was more than expectations, but still far from the 3.5% or more that would prompt government action. Food prices were even higher in April, coming in at 4%—one of the biggest concerns for the government.

China’s consumer inflation slowly but surely ticked up in April, rising 2.4% from April in 2012, compared with a 2.1% year-on-year increase in March. That was more than expectations, but still far from the 3.5% or more that would prompt government action. Food prices were even higher in April, coming in at 4%—one of the biggest concerns for the government.

Reuters noted that the Chinese government could soon face stagflation—in which prices rise even as the economy stalls. China’s export data make it difficult to know by how much growth is slowing: officially, GDP grew a disappointing 7.7% in Q1. But more than half of that growth came from investment. That means Chinese households still do not feel empowered to buy stuff—and rising prices make it even more difficult to rebalance the economy toward the Chinese consumer.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Analysts were all over the map in how they read the data, showing how little is understood about how the new government will respond to China’s unexpectedly slowing growth (paywall). That most of their analysis hinged on whether the government would stimulate investment signals the dearth of plausible options left to the government to make the economy grow.

It might work as a short-term fix, but investment is very clearly the last thing China needs in the longer run. It already has more factories than it needs to meet global demand, which means that much of that lending cycles back into the real estate market, where prices are already threatening to overheat.

Even if the central government used fiscal policy to increase infrastructure investment—as opposed to loosened credit, its primary monetary policy tool—it will only exacerbate the already frightening levels of overcapacity besetting China’s manufacturing and infrastructure.

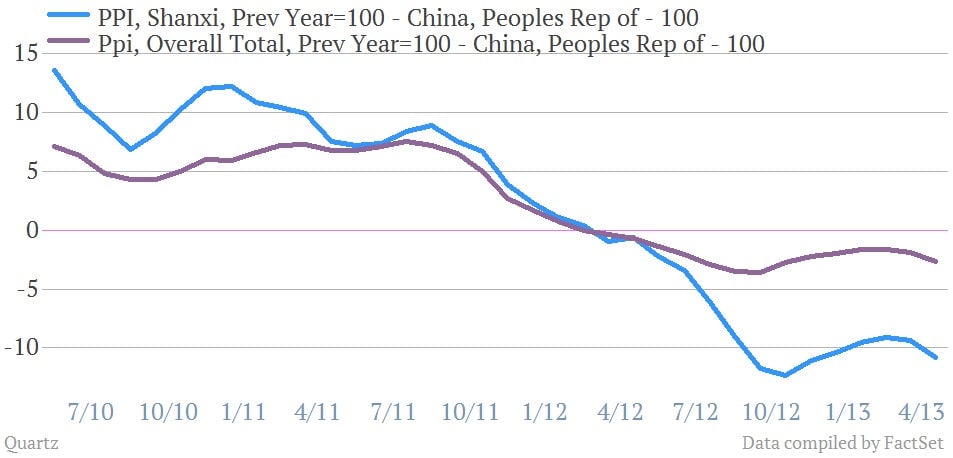

We can see this in the producer price index, which fell 2.6% year-on-year in April, 0.6% lower than in March, marking the 14th straight month of contraction. Prices continue to fall because producer demand for goods has been rapidly deteriorating, as nearly three years worth of profligate lending—from the stimulus years of 2009 to 2011—built up execess capacity. With global demand still anemic and Chinese consumers giving no sign of picking up the slack, there’s no end-customer for what these factories can produce.

Another factor here is falling commodity prices due to China’s unexpectedly slumping growth. Take a look, for example, at the PPI for Shanxi, one of China’s biggest coal-producing provinces.

One reason that’s happening is that coal producers around the world misjudged Chinese demand, causing a glut. As their unsold stocks pile up, miners in Shanxi and other coal provinces are now slashing output.

These are definitely not problems that more investment can fix.