Life in the military isn’t easy, but if you serve long enough the financial rewards, at least, are great.

Life in the military isn’t easy, but if you serve long enough the financial rewards, at least, are great.

The US military offers very generous pension benefits—after 20 years of service, members can retire with 50% of their final salary for the rest of their lives. Since that allows most to retire around age 40, the payouts may last for a very long time (and they are also adjusted for inflation). In 2015, the US military paid out $57 billion in pension benefits (pdf) to more than 2 million veterans, or nearly 10% of its annual budget.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

The military estimates that the net present value of its pension at retirement is around $200,000 for an enlisted soldier and $700,000 for an officer. (Recall, however, that the payouts are guaranteed for life, so the risk-adjusted value is worth much more.) This is enough for a basic living on its own, or more commonly used to supplement veterans’ earnings in their second careers. But only 17% of active duty members stick around long enough to collect it.

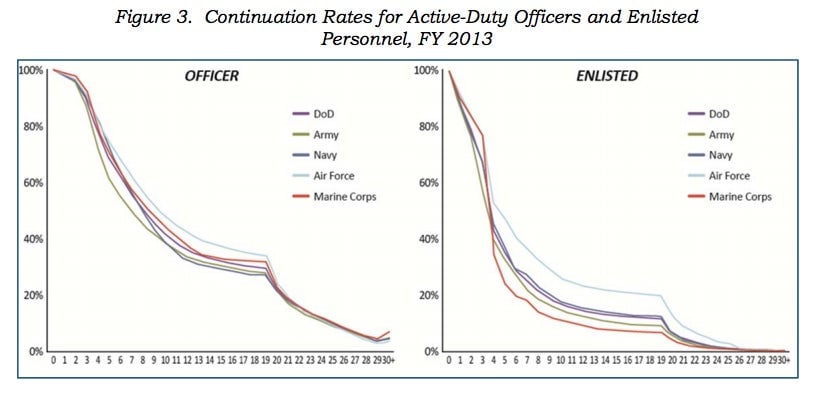

Until recently, if military members left before 20 years of service, they didn’t get any pension benefit. This leads to what’s known as “cliff vesting” around the 20-year mark. Given the obvious dangers inherent in the service, and the stress it puts on families, attrition is steep in the early years. Things get interesting near the 10-year mark, when leaving rates flatten out. Then, a large share of those who reach 20 years of service retire at the first opportunity and collect their pensions. The 20-year point also often corresponds to a crucial up-or-out promotion point; members who stick around longer can retire after 40 years with a pension payout worth 100% of their final salary.

According to Major Brandon Archuleta, an expert on military retirement policy who teaches political science at West Point, the pension serves as “golden handcuffs” for soldiers and officers once they reach the halfway-to-a-pension point of 10 years of service. “Once they get to that point, service members end up taking less desirable assignments [instead of leaving the military] like Ft. Polk Louisiana, Korea, or Alaska,” he says.

For this reason, the pension is a powerful tool. It offers predictability of re-enlistment for a certain group of service members and leverage over them once they are locked in.

But the pension also exacerbates inequality within the military, namely the gap between the share of officers and enlisted soldiers who end up collecting the benefit (49% of officers versus 17% overall). This may not be the most efficient way to spend military resources because, arguably, officers—who account for around 20% of active duty personnel—have less need for such a generous pension. They tend to be more skilled and better educated, which means they have stronger earnings prospects after they leave the military.

The military, too, isn’t immune to the demands of millennials who aren’t as loyal to employers as some older generations. Citing the pressure from younger, more mobile service members, a 2015 commission suggested adding 401(k)-type accounts to military pay packages, which lawmakers approved last year.

Starting in 2018, the payouts after 20 years of service become a bit less generous, at 40% of a member’s final salary instead of 50%. But there is also now a defined contribution plan that everyone can join, with some of the funds they put in matched by their employer, like most traditional corporate pension plans. This means all members of the military can leave with some retirement savings, regardless of their length of service.

This has the potential to dramatically alter how the military operates. Enlisted service members now have an incentive to stay on for longer, but aren’t compelled to stay after they pass the symbolically important 10-year milestone. Archuleta says it is too soon to tell if the reforms will have any impact on career progression.

At most private and public organizations, employees aggressively resist cuts to pension benefits. But the military pension reforms were well received, with more than half of service members in favor of them. No doubt that’s because for the bulk of the force, namely the 83% of enlisted soldiers who quit before their retirement benefits kick in, gain from the reforms.