Is it time to slow down high-frequency trading? A new study says yes (pdf). Despite arguments that it provides liquidity in markets, researchers from the University of Michigan argue that it harms the average investor.

Although the term “high-frequency trading” (HFT) is often used loosely to describe trading at high speeds by computers, in this case we mean something specific: high-volume arbitrage activity, which plays on small, temporary differences in price between, say, a security trading both on the New York Stock Exchange and DirectEdge.

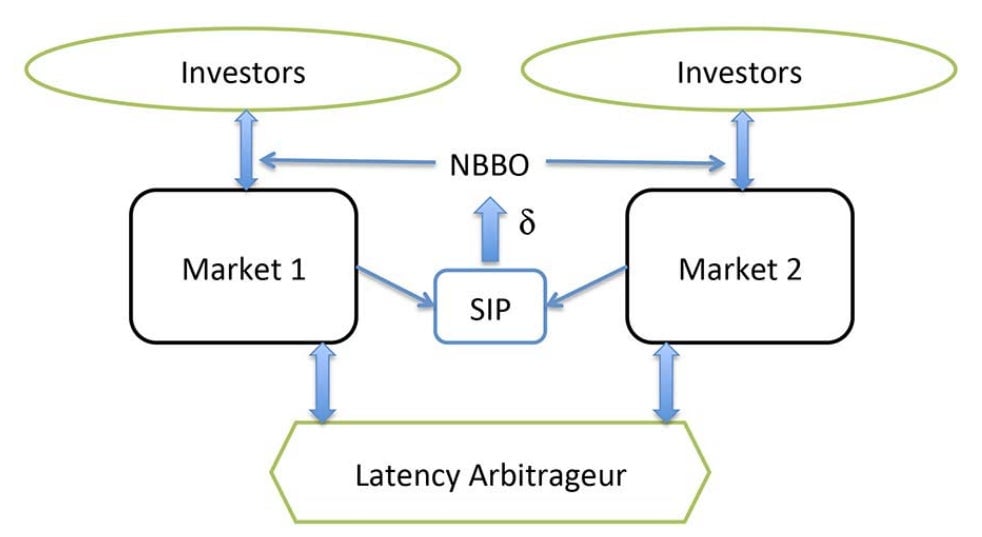

Orders can be placed on one exchange to transact with orders on another exchange. A central system called the Security Information Processor (SIP) takes information from the two exchanges and calculates a price for the trade, called the National Best Bid and Offer price (NBBO). Doing that takes a few milliseconds, however, and high-frequency traders can go on trading while the calculation is being made, taking advantage of the temporary disparity between the price on the two exchanges. The report’s authors, Elaine Wah and Michael Wellman, explain how:

Given order information from exchanges, the SIP takes some finite time, say δ milliseconds, to compute and disseminate the NBBO. A computationally advantaged trader who can process the order stream in less than δ milliseconds can simply out-compute the SIP to derive NBBO*, a projection of the future NBBO that will be seen by the public. By anticipating future NBBO, an HFT algorithm can capitalize on cross-market disparities before they are reflected in the public price quote, in effect jumping ahead of incoming orders to pocket a small but sure profit. Naturally this precipitates an arms race, as an even faster trader can calculate an NBBO** to see the future of NBBO*, and so on.

Advocates of HFT have argued that this kind of trading is good because it cuts down transaction times and cost, and pretty much ensures that any retail or institutional investor can find someone to take the other end of their trade. But Wah and Wellman argue that HFT doesn’t actually make markets more efficient. It’s great for those who practise HFT, but it reduces profits to everyone else, because in those few milliseconds before the NBBO is calculated and disseminated, the high-frequency traders carry out deals at a price that favors them.

In fact, Wah and Wellman find, the difference between investor bids (offers to buy) and asks (offers to sell) is wider when arbitrageurs get into the mix, meaning neither sellers nor buyers in the non-HFT world are getting the best price they could.

The study finds that these losses are substantial over time. It proposes a system that doesn’t allow exchanges to continue trading while an NBBO is being calculated. Instead, exchanges would have to wait for the NBBO to come out before executing an order. That would eliminate the advantages offered by arbitrage, the study argues—and exchanges probably wouldn’t like it either, because they make money each time a trade happens. But it would bring more value to background investors.

However, it’s not clear that a centralized system would make markets much more stable. HFT has been blamed for swift drops in the market—like the “flash crash” of 2010—but what sets these off is when computer algorithms (not just high-frequency arbitrage traders) issue orders to sell all at once. Then again, a new, centralized system might be a step in the right direction.