The biggest economic upheavals in modern history trace back to identifiable decisions made by identifiable people — and those decisions could have gone differently

Farm Security Administration / Wikimedia Commons

Economic history has a tendency to make the past feel inevitable. The Great Depression reads, in retrospect, as the natural consequence of the excesses of the 1920s — the speculative bubble, the easy credit, the overextended banks. The 2008 financial crisis reads as the natural consequence of a housing market that was always too inflated, a derivatives market that was always too opaque, a regulatory framework that was always too permissive. The eurozone debt crisis reads as the natural consequence of currency union without fiscal union — a structural problem that was always going to produce this outcome eventually.

This retrospective fatalism is analytically convenient and historically misleading. Economic crises are not natural disasters, produced by impersonal forces whose accumulation was inevitable from the start. They are produced by specific decisions, made by specific people, at specific moments when other decisions were available. The Treaty of Versailles's reparations clause was a choice — a choice that the economists advising the Allied governments advised against and that the political leaders overrode for domestic reasons. The Federal Reserve's decision to raise interest rates in 1931, in the middle of a banking crisis, was a choice — one that Milton Friedman and Anna Schwartz later identified as the single most consequential policy error in American economic history. The decision to allow Lehman Brothers to fail in September 2008 was a choice — and the people who made it have spent years explaining why it was not, in fact, the only option.

This list covers 15 economic events — crises, crashes, booms, reforms, and turning points — and identifies the specific human decisions that produced them. The framing is not primarily about blame, though accountability is relevant. It is about restoring agency to economic history — recognizing that the largest economic upheavals are not natural phenomena but the products of human judgment, operating under specific constraints, with specific information, making specific choices whose consequences unfolded across years and decades.

Each slide identifies the event, the decision or decisions that drove it, the person or people who made those decisions, and the counterfactual — what might have been different if the decision had gone another way. The counterfactuals are necessarily speculative, but their value is in making clear that alternatives existed and that the path taken was chosen, not inevitable.

Bec / Wikimedia Commons (CC BY-SA 4.0)

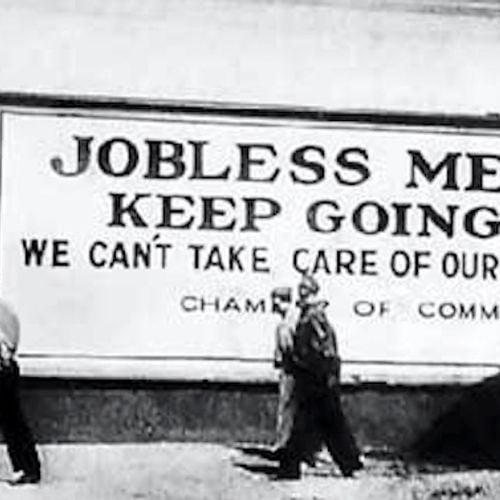

The Great Depression — the decade-long economic collapse that began in the United States in 1929 and spread globally, producing unemployment rates of 25% in the United States and comparable devastation in most industrialized economies — was not simply the inevitable consequence of the 1920s bull market. Its specific severity, duration, and global spread were substantially the product of a specific policy error made by the Federal Reserve between 1929 and 1933.

The decision, documented most thoroughly by Milton Friedman and Anna Schwartz in "A Monetary History of the United States" (1963), was the Federal Reserve's failure to act as a lender of last resort during the banking panics of 1930, 1931, and 1932, and its decision to raise interest rates in 1931 in response to Britain's abandonment of the gold standard — an action designed to protect American gold reserves that produced a further contraction of the money supply at precisely the moment when expansion was most needed.

Between 1929 and 1933, the money supply contracted by approximately one-third. Bank failures were allowed to cascade without Fed intervention — 9,000 banks failed in the United States between 1930 and 1933, destroying the savings of millions of ordinary Americans and collapsing the credit channels that businesses depended on for working capital. The Smoot-Hawley Tariff Act, signed by President Hoover in June 1930 over the objections of more than 1,000 economists who sent a signed petition opposing it, raised tariffs on imported goods to historically high levels and triggered retaliatory tariffs from trading partners, collapsing international trade.

Ben Bernanke, who chaired the Federal Reserve during the 2008 financial crisis, had spent his career studying the 1930s Fed's errors. His decision to aggressively expand the money supply and act as lender of last resort in 2008 was explicitly informed by Friedman and Schwartz's diagnosis. At a 2002 conference honoring Friedman's 90th birthday, Bernanke said: "You're right, we did it. We're very sorry. But thanks to you, we won't do it again."

The British Government / Wikimedia Commons (CC BY-SA 4.0)

The Treaty of Versailles, signed in June 1919, imposed on Germany reparations of 132 billion gold marks — equivalent to approximately $440 billion in contemporary terms — along with the loss of 13% of its prewar territory, 10% of its population, and the "war guilt" clause (Article 231) that assigned sole responsibility for the war to Germany and its allies. The economist John Maynard Keynes, who attended the Paris Peace Conference as a British Treasury representative, resigned in protest and published "The Economic Consequences of the Peace" in December 1919, predicting with considerable accuracy the instability that the settlement would produce.

Keynes's argument was specific: the reparations demand was set at a level that Germany could not pay without running persistent trade surpluses, which the victorious powers' trade policies would not permit. The attempt to extract reparations under these conditions would produce chronic German economic instability, hyperinflation, political radicalization, and ultimately another war. The specific decision that produced this outcome was the Allied leaders' choice — driven primarily by domestic political pressure, particularly in France and Britain, to demonstrate that Germany would pay for the war — to override the economic advice they received in favor of a settlement calibrated to political optics rather than economic stability.

The German hyperinflation of 1921 to 1923, the Great Depression's specific severity in Germany, the political crisis that brought Hitler to power in 1933, and the Second World War are all traceable, with varying directness, to the settlement of 1919. The counterfactual — a Carthaginian peace versus the more measured settlement that Keynes and others advocated — is one of the most studied in 20th-century economic history, and its lesson about the long-run costs of economically illiterate political settlements remains directly relevant.

On August 15, 1971, President Richard Nixon announced in a Sunday evening television address that the United States would suspend the convertibility of the dollar into gold, effectively ending the Bretton Woods system that had governed international monetary relations since 1944. The decision — made in a secretive weekend meeting at Camp David with a small group of advisors, without consultation with the international partners whose monetary systems depended on the dollar-gold link — transformed the global financial system in ways whose implications are still unfolding fifty years later.

The immediate cause was a balance of payments crisis: the United States had been running persistent deficits, dollar holdings abroad had accumulated to the point where the convertibility guarantee was no longer credible (foreign central banks held more dollars than the United States held gold to redeem them), and France under Pompidou had begun converting its dollar holdings into gold, accelerating the crisis. The decision to end convertibility, rather than devalue or deflate, was made by Treasury Secretary John Connally — a Texas Democrat turned Republican Nixon appointee with no prior interest in monetary economics — whose specific influence on Nixon's thinking was decisive.

Connally's famous remark to G10 finance ministers — "the dollar is our currency but your problem" — captures the attitude behind the decision: the United States would act in its own interest without regard for the systemic consequences for the international monetary order it had established and from which it had derived significant benefit. The floating exchange rate system that resulted — which produces the currency volatility, carry trades, and exchange rate crises that have characterized international finance since the 1970s — was not designed. It was the consequence of a unilateral decision made for domestic political reasons.

On September 16, 1992 — Black Wednesday — the British government was forced to withdraw the pound sterling from the European Exchange Rate Mechanism (ERM) after a speculative attack orchestrated primarily by George Soros and his Quantum Fund depleted the UK's foreign exchange reserves in a single day. The British government spent approximately £3.4 billion attempting to defend the pound and was forced to exit the ERM after raising interest rates twice in a single day — to 10%, then to 12%, with an announced intention to raise to 15% — failed to discourage the speculators.

The specific decision that created the vulnerability was the decision to enter the ERM in October 1990 at a rate of DM 2.95 per pound — a rate that most economists considered too high relative to the UK's actual competitive position. Chancellor John Major had championed ERM membership as a framework for anti-inflationary discipline, and the rate was set to demonstrate commitment rather than to reflect economic fundamentals.

By 1992, with Germany raising interest rates to manage the post-reunification inflationary pressure, the UK was required to maintain high interest rates to defend the exchange rate peg at precisely the moment when its recession required lower rates. Soros's specific insight was that this contradiction was unsustainable and that the UK government would eventually choose the domestic economy over the exchange rate commitment — a bet that proved correct.

The UK's exit from the ERM — and the recovery that followed as lower interest rates stimulated the economy — reinforced the lesson that exchange rate commitments that contradict domestic economic conditions are not credible and cannot be defended against determined speculative attack regardless of the volume of reserves deployed.

Office of the Vice President, The Republic of Indonesia / Wikimedia Commons

The Asian financial crisis of 1997 to 1998 — which spread rapidly from Thailand to Indonesia, South Korea, Malaysia, and the Philippines, collapsing currencies, stock markets, and banking systems across the region — was precipitated by a specific sequence of decisions made by the Thai government, by international investors, and by the International Monetary Fund whose combined effect was to turn a manageable balance of payments problem into a systemic economic catastrophe.

The initial vulnerability was created by Thailand's decision to maintain a fixed exchange rate peg between the baht and the U.S. dollar while allowing domestic banks to borrow cheaply in dollars and lend in baht — a carry trade that was enormously profitable while the peg held and catastrophically destabilizing when it did not. The Bank of Thailand spent approximately $30 billion of its foreign exchange reserves defending the peg against speculative attack before being forced to float the baht in July 1997.

The IMF's response — which conditioned emergency loans on fiscal austerity and high interest rates — has been extensively criticized as having amplified the crisis rather than contained it. The specific decision to impose pro-cyclical conditions (reducing spending and raising rates during a sharp economic contraction) reflected the ideological commitments of the IMF's management rather than the specific circumstances of the Asian crisis, and its effect was to deepen and prolong the recessions that the currency collapses had initiated.

Joseph Stiglitz, then Chief Economist of the World Bank, publicly criticized the IMF's handling and was subsequently pressured to resign — a political episode that produced his subsequent memoir "Globalization and Its Discontents," which is the most detailed insider account of the specific human decisions behind the IMF's crisis management.

Marek Slusarczyk / Wikimedia Commons (CC BY 3.0)

The 2008 financial crisis — whose immediate trigger was the collapse of the U.S. subprime mortgage market but whose systemic consequences reflected vulnerabilities in the global financial system that had been building for a decade — was the product of multiple interacting decisions whose combination produced the largest financial crisis since the Great Depression.

The specific decisions most directly responsible: the SEC's April 2004 decision to allow the five largest investment banks to increase their leverage ratios from 12:1 to as much as 40:1 — a decision made in a single 55-minute meeting at which none of the commissioners expressed concern; Alan Greenspan's decision to maintain interest rates at historically low levels between 2001 and 2004, creating the credit conditions that fueled the housing bubble; the ratings agencies' decisions to assign AAA ratings to mortgage-backed securities based on models that systematically underestimated the correlation of default risk across regional housing markets; and the decision — specifically attributed to Hank Paulson and Tim Geithner — to allow Lehman Brothers to fail without a pre-arranged buyer or government backstop.

The Lehman decision is the most contested. Paulson has argued that the Federal Reserve lacked the legal authority to rescue Lehman without a viable acquirer. Critics argue that this legal constraint was not as binding as claimed — that the Fed's emergency lending powers under Section 13(3) of the Federal Reserve Act were broad enough to support a rescue — and that the decision not to rescue Lehman reflected political calculation (the optics of a third bailout following Bear Stearns and the conservatorship of Fannie and Freddie) as much as legal limitation.

On the night of September 29, 2008 — two weeks after Lehman Brothers filed for bankruptcy and with the global financial system in acute distress — the Irish government announced a blanket guarantee of all deposits and most liabilities of its six main financial institutions, covering approximately €400 billion in liabilities against a GDP of approximately €160 billion. The guarantee was the most generous and most consequential single government intervention in the 2008 crisis, and it transferred the cost of Ireland's banking system's reckless lending from the banks' shareholders and bondholders to the Irish taxpayer.

The decision was made by a small group — Taoiseach Brian Cowen, Finance Minister Brian Lenihan, the heads of the financial regulator and the central bank, and the Government's attorney general — in approximately six hours, without consultation with the European Central Bank or Ireland's EU partners, and on the basis of financial information from the banks themselves that subsequently proved to be significantly worse than what was reported. The guarantee was presented to them as the minimum necessary to prevent the imminent collapse of the banking system; whether this was accurate, or whether a more targeted guarantee of deposits rather than bank bonds would have achieved the same result at lower cost to taxpayers, has been debated since.

The International Monetary Fund's subsequent assessment was that the guarantee had been too broad — that including subordinated debt and senior unsecured bonds had unnecessarily protected investors who bore risk in exchange for yield and should have absorbed losses. The ECB's refusal to allow Ireland to impose losses on senior bondholders subsequently limited the Irish government's ability to correct the error, producing a program of austerity whose social costs were borne by people who had no part in the lending decisions that caused the crisis.

Wang Liuying, et al. / Wikimedia Commons

The Great Leap Forward — Mao Zedong's 1958 to 1962 campaign to rapidly transform China from an agrarian economy into a communist industrial society — produced a famine estimated to have killed between 15 and 55 million people, making it the deadliest famine in human history. The famine was not a natural disaster. It was the direct and predictable consequence of specific policy decisions made by Mao and enforced by the Communist Party apparatus.

The central decisions: the collectivization of agriculture into People's Communes, which eliminated the individual incentive to farm effectively; the setting of grain quotas at levels that required local officials to report false production numbers to meet targets they could not achieve; the diversion of rural labor from food production to backyard steel furnaces whose output was mostly unusable; and the continuation of grain exports throughout the famine, based on official statistics that showed production far exceeding actual harvest.

Mao was informed that the statistics were falsified and that the famine was occurring. The specific decision to maintain the export of grain and the collectivization policies in the face of documented starvation reflects a specific political priority — the maintenance of the fiction that the Great Leap Forward was succeeding — over the lives of the population whose welfare the policy was nominally designed to improve. Officials who reported the famine accurately were accused of right-wing deviation and removed; officials who falsified reports were rewarded.

The Great Leap Forward is the most extreme example in this list of an economic catastrophe produced by the deliberate suppression of accurate information and the punishment of those who provided it — a dynamic whose less extreme versions recur throughout economic history.

William Warby / Pexels

In April 1925, Winston Churchill, then Chancellor of the Exchequer, announced Britain's return to the gold standard at the prewar parity of $4.86 per pound — a decision that Keynes immediately attacked in his pamphlet "The Economic Consequences of Mr. Churchill" as overvaluing the pound by approximately 10%, condemning British export industries to uncompetitiveness and British workers to wage cuts and unemployment.

Churchill's decision was made against the advice of his own economic advisors at the Treasury, who were divided, and against Keynes's specific public argument. It was driven by a combination of financial orthodoxy — returning to gold was considered the responsible monetary policy of the era, the mark of a serious economy — and by the specific prestige consideration that prewar parity was the rate that mattered symbolically, even if it was economically incorrect.

The consequences were as Keynes predicted. British exports became uncompetitive at the overvalued rate. The coal industry faced specific pressure, leading to the General Strike of 1926. Unemployment remained high throughout the late 1920s when the rest of the world was experiencing growth, and Britain entered the Great Depression from a weaker economic position than it would have held had the return to gold been at a lower parity or been avoided entirely.

Churchill later described the decision as the greatest mistake of his career. The specific lesson — that monetary arrangements that prioritize symbolic prestige over economic reality impose real costs on real workers — recurs throughout the history of exchange rate policy.

Pixabay / Pexels

The euro — the common currency of the European Union, adopted by 11 countries in 1999 and subsequently expanded to 19 — was launched with structural features that economists widely identified as problematic before its creation. The specific design choices were made by European governments that understood the risks and accepted them for political reasons, creating a currency union without the fiscal union that economic theory indicated was necessary for the union to function optimally under stress.

The optimal currency area theory, developed by Robert Mundell in 1961, identifies the conditions under which a common currency is beneficial: labor mobility, capital mobility, price and wage flexibility, or fiscal transfers. The eurozone in 1999 had the first two to a limited degree, the third insufficiently, and the fourth almost not at all. When the 2008 financial crisis hit and peripheral eurozone countries (Greece, Ireland, Spain, Portugal) needed fiscal stimulus to respond to their downturns, they could neither devalue (they had given up their currencies) nor significantly expand their deficits (the Stability and Growth Pact limited deficit spending), nor receive fiscal transfers from the stronger economies that might have absorbed the shock.

The decisions that created this structural vulnerability were made primarily by Germany and France, which insisted on the Stability and Growth Pact's deficit limits and refused to agree to a shared fiscal mechanism, and by Greece, which joined the eurozone in 2001 on the basis of statistics that it had falsified — a deception that its Goldman Sachs $GS advisors had helped to engineer through currency swap arrangements that moved debt off the official balance sheet.

Japan's "Lost Decade" — the prolonged economic stagnation that followed the collapse of the Japanese asset price bubble in 1989 to 1991 and that extended through the 1990s and into the 2000s — is the most studied example of a major economy's failure to recover from a financial crisis, and the specific policy failures that produced the lost decade have directly informed subsequent crisis response strategies.

The bubble was created by the Bank of Japan's decision to maintain extremely low interest rates through the late 1980s, fueling an asset price inflation in property and equities that produced extraordinary valuations disconnected from any fundamental basis. The Bank eventually raised rates in 1989 to cool the overheating, and the collapse of asset prices produced a banking crisis as the collateral backing enormous loan books evaporated.

The specific policy failure in the recovery phase was the Japanese government's refusal, through most of the 1990s, to force the banking system to recognize its losses — the mountains of non-performing loans on bank balance sheets that were kept alive through evergreening (lending more to borrowers who could not service existing loans, preventing them from defaulting) rather than written down. The zombie bank phenomenon — banks that were technically insolvent but kept alive by regulatory forbearance and government support — prevented the credit allocation to productive new businesses that recovery required.

The IMF and Western economic advisors who studied Japan's experience in real time identified the zombie bank problem clearly; the Japanese Ministry of Finance resisted the prescription of forced bank recapitalization and loss recognition for reasons that combined institutional self-interest with the specific cultural difficulty of the public failure that bank write-downs would represent.

Argentina's convertibility crisis of 2001 to 2002 — the largest sovereign debt default in history to that point, the collapse of a currency board that had pegged the Argentine peso to the U.S. dollar since 1991, and the social upheaval that produced five presidents in two weeks — was the endpoint of a decade of economic policies whose fatal flaw was apparent to economists before the crisis but was not corrected because correction was politically difficult.

The convertibility plan — the 1:1 peg of the peso to the dollar introduced by Economy Minister Domingo Cavallo in 1991 — succeeded spectacularly in eliminating the hyperinflation that had devastated Argentina in the late 1980s and produced a period of growth and capital inflow. Its structural problem was the same as Britain's 1925 gold standard return at the wrong parity: the real exchange rate appreciated substantially over the decade as Argentina's inflation, though low by historical standards, remained higher than its trading partners', making exports progressively less competitive.

The IMF's role in sustaining the convertibility plan past the point when its correction would have been manageable has been heavily criticized. The Fund provided large emergency loans in 2000 and 2001 — a $40 billion package in 2000, described as the largest in Fund history to that point — that delayed the inevitable crisis while increasing its eventual scale. The specific decision by IMF management to provide these loans, over the objections of some Fund economists who argued the plan was unsustainable, reflected the Fund's institutional discomfort with acknowledging the failure of a program it had endorsed and the specific geopolitical pressure to prevent the contagion that an Argentine collapse might spread.

National Photo Company / Wikimedia Commons

The Smoot-Hawley Tariff Act, signed by President Hoover in June 1930, raised U.S. tariffs on more than 20,000 imported goods to record levels. More than 1,000 economists signed a petition urging Hoover to veto the bill; Henry Ford $F visited the White House personally to argue against it; J.P. Morgan's Thomas Lamont described himself as "almost breaking down and weeping" in his efforts to convince Hoover to veto. Hoover signed it anyway.

The decision was driven by congressional logrolling — the process by which legislators trade votes across bills — that had assembled a coalition of agricultural and industrial interests each seeking protection for their specific sector, and by the political dynamic of a president facing re-election in a deepening recession who did not want to be seen as opposing protections for American industries. The economic advice was unanimous and was overridden by political calculation.

The immediate response was retaliatory tariffs from Canada, Great Britain, France, Germany, and others, collapsing international trade. U.S. imports fell 66% between 1929 and 1932; U.S. exports fell 61%. The collapse of trade deepened and lengthened the Depression. The specific causal contribution of Smoot-Hawley relative to monetary policy failures is debated among economic historians — Friedman gave more weight to monetary policy — but the tariff's role in the collapse of international trade and the globalization of the Depression is not seriously contested.

The South Sea Bubble of 1720 — the spectacular inflation and collapse of the South Sea Company's share price in the first half of 1720 — is the first major financial crisis of the modern era and a template for every speculative bubble that followed. Its specific mechanism — the deliberate manipulation of share prices, the corruption of government officials, and the extension of credit to fund share purchases that amplified the bubble — was the product of decisions made by specific people who understood what they were doing and profited from it while it lasted.

The South Sea Company had been granted a monopoly on trade with South America in 1711, but the trade was largely fictional — Spain controlled the relevant ports and had no interest in allowing British trading access. The company's actual business was the management of government debt, converted into company shares whose value depended on public confidence rather than commercial performance. In 1720, the company's directors — led by John Blunt, the company's primary architect — proposed to take over the entire national debt, issuing company shares in exchange for government debt instruments.

The share price was then deliberately inflated through a series of techniques: company directors lent money to investors to buy shares (creating artificial demand), company officials bribed key government ministers (including the Chancellor of the Exchequer) with shares at below-market prices, and false reports of successful South American trade were circulated to maintain the speculative enthusiasm. The share price rose from £128 in January 1720 to £1,000 in August before collapsing to £124 by December.

The Parliamentary inquiry that followed — the first in British history into a financial scandal — resulted in the imprisonment of several company directors and the sequestration of their estates. The scandal also prompted Robert Walpole, who had opposed the scheme, to become the first de facto Prime Minister and to impose financial regulations that were the earliest precursors of modern securities law.

The dot-com bubble — the inflation and collapse of technology company valuations between approximately 1995 and 2001, which destroyed an estimated $5 trillion in market value and wiped out hundreds of companies — is the most recent large-scale speculative bubble before 2008 and the one whose specific human decision mechanisms are most thoroughly documented, because it occurred in an era of financial journalism, SEC filings, and analyst reports that left an unusually complete record.

The bubble was created by a specific set of interacting decisions. Investment banks made the initial public offerings of unprofitable technology companies at valuations justified by metrics invented to circumvent the absence of earnings — eyeballs, page views, click-through rates — and collected fees proportional to the valuations they assigned. Equity research analysts at those same banks issued buy recommendations on companies their private communications described as worthless — a conflict of interest documented in the subsequent investigations by New York Attorney General Eliot Spitzer, who published emails by Merrill Lynch analyst Henry Blodget describing as "a piece of junk" and "a dog" stocks he was simultaneously recommending to clients.

Alan Greenspan's "irrational exuberance" speech in December 1996 — in which he identified the possibility of irrational exuberance in asset markets and suggested the Fed might need to respond — was followed by no policy action and was interpreted by markets as a warning that was not followed up. The Fed kept interest rates low through the bubble's most extreme inflation phase. Greenspan subsequently acknowledged that he had expected the market to self-correct without intervention.

The specific decisions of venture capitalists to fund companies with explicitly negative unit economics — businesses designed to grow at any cost with profitability deferred indefinitely — created the conditions for the most spectacular failures: Pets.com, Webvan, Boo.com, and dozens of others that raised hundreds of millions and collapsed within months. The decisions of individual investors to buy shares in these companies reflected a belief that greater fools would pay more — a rational individual strategy in a bubble whose systemic irrationality was clear to any analyst willing to do the arithmetic.