Companies are using price cutting wars to push out new entreats, according to a new paper.

When monopoly power is the prize, competition becomes dangerous for both companies and consumers.

This was one of several conclusions in a preprint paper published in the National Bureau of Economic Research. Economists from MIT, the University of Hong Kong, and the University of Pennsylvania used a theoretical model to study how firms try to take each other down to become superstar companies that can charge higher prices with less competition.

Before companies settle into a peaceful tacit collusion, the economists found,they may engage in predatory pricing wars to push another firm out of the market. These wars have nothing to do with making business better or improving products for customers, and instead are aimed at bankrupting the competition.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

What follows is a a Q&A with Hui Chen, a finance professor at MIT and one of the paper’s authors. The conversation has been edited for length and clarity.

There are two sets of facts that motivated us to study this phenomenon. The first one is a more macro level: This rise of superstar firms in the US, and to some extent in other countries as well. Industry concentration has risen in the majority of the industries in the US for the last 20 to 30 years.

On top of that, there’s also evidence suggesting that these large, superstar firms, they have really long lasting power. This gives them room for what we call collusive competition or implicit collusion.

Without entering into explicit collusive agreements, which are illegal, they can economically motivate each other to charge higher prices and enjoy higher profit margins.

Implicit collusion until this point has only been studied at a relatively simple static framework. In particular, the interaction of [implicit collusion] with financial conditions of the firm has not been explored before.

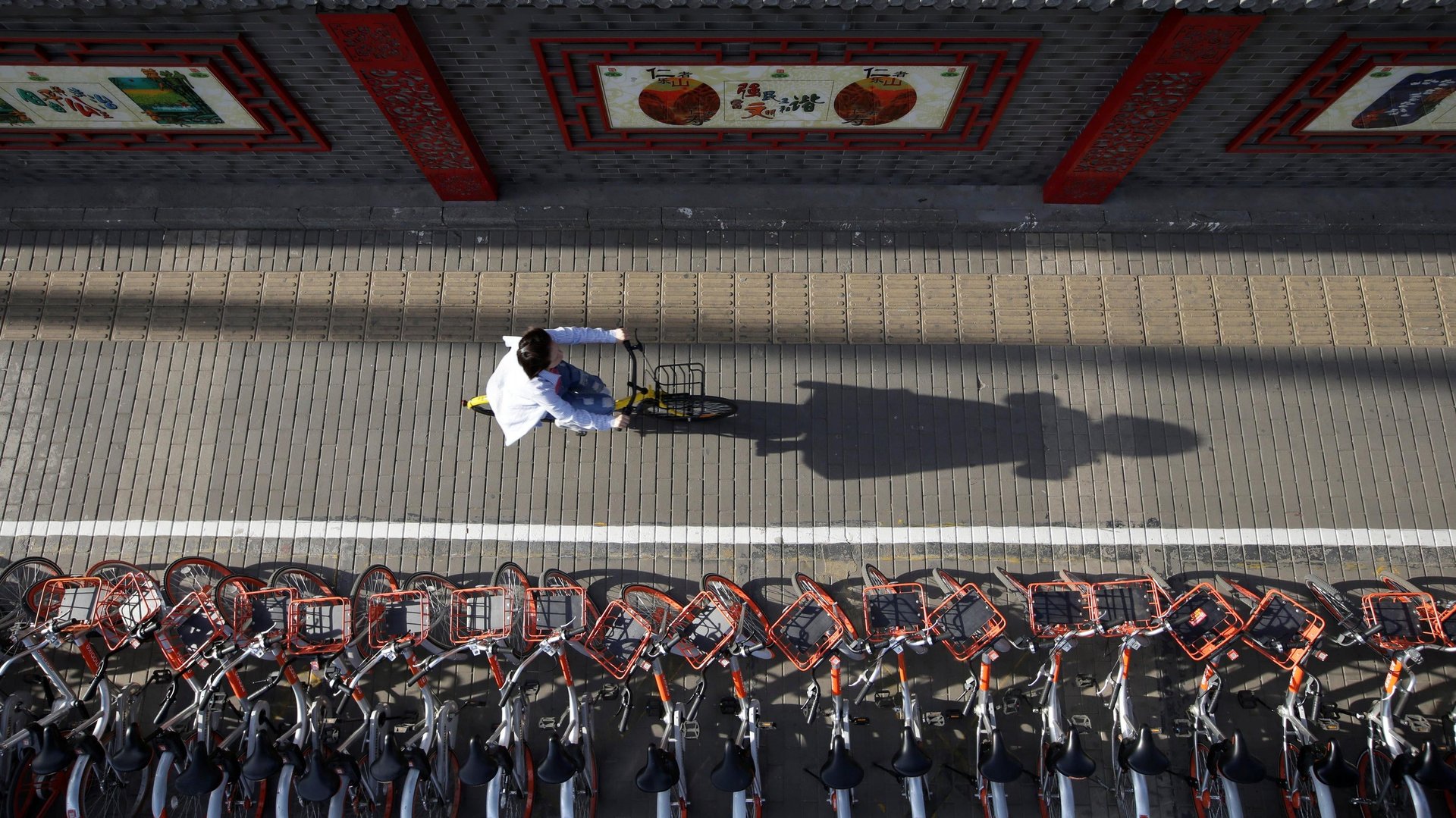

The second fact that motivated us was observing some new internet companies competing. The one we like to talk about is competition of mobile bike providers in China.

An interesting example is two companies called Mobike and Ofo. These two companies, basically, were trying to grow their market share very aggressively. They would try to price very aggressively on their services—in this case, mobile bikes—and they charge very little. And then they borrow very heavily and try to grab as much market share as possible.

The consumers benefit a lot, but [the companies] are putting tremendous competition pressure on each other. Mobike got acquired by a larger internet company, and the other one went bankrupt.

In this case there was not any kind of peaceful implicit collusion, but they went after each other as financial trouble started to emerge.

They not only didn’t take a step back, but they went even more gung ho and cut prices even more to try to kick their opponent out of the market and after that enjoy more pricing power.

That also motivated us. The fact that it’s not just competition, but also predatory price behavior to try to force your competition out of the market. That’s another reason that we thought bringing in the financial risk of these firms into this type of collusive competition was important.

These kinds of incentives are driving firms to not compete in a calm way but rather be ultra aggressive. They’re even willing to endure some short term losses in exchange for the higher market share

The more calm equilibrium is where major players—think about Uber $UBER and Lyft $LYFT—they enter into more of a calm partnership. They both agree to not go after each other too aggressively and both can live in a relatively stable environment so they don’t have to sacrifice their pricing power too much.

Yeah, first of all, economic equilibrium is good for companies but not necessarily good for customers. That’s one thing to clarify.

Within the framework of our model, it’s primarily determined by the entry threat. If an incumbent exits the market and a new entrant comes in, do they present a bigger threat than the incumbents who already survived competition?

Let’s say that Uber managed to kick out Lyft. For the sake of discussion, let’s also imagine that there are limited licenses that the government is willing to issue for these ride sharing apps. The question then becomes, is the new competitor going to be many times financially stronger than Lyft, or will they be small and non-threatening?

That matters a lot. Because if it’s the former, why would I want to kick out Lyft and invite a hundred pound gorilla? I would much rather keep a relatively weak incumbent and that would push me toward being more accommodative with Lyft.

In fact, our model shows if Lyft gets in trouble for some kind of idiosyncratic reason, not only would you not see Uber step up competition, but they would actually step back and be more friendly to help Lyft survive the episode.

But if they see no entry threat, then the exact opposite would happen. As soon as they see weakness, that could trigger a price war between the two firms.

If you’re thinking like the regulator and want to deter this price war and monopoly power, then encouraging the entry of stronger players is going to be good.

Because our paper didn’t get into the welfare analysis very deeply, I’m only speculating here.

If you think about the consumer, in the short run the price wars do benefit customers because they can have low prices, but let’s not be confused about this because in the long run these firms are hoping to become a monopoly. Consumer welfare will suffer in the long run.

For that reason, I think the regulators should find ways to discourage these types of price wars. So if there are regulatory hurdles that prevent new entrants, we should try to loosen and maybe even get rid of them. The example we like to think about when presenting this paper is examples where government licenses are limited.

Think about telecommunication and other markets where there are limited licenses available for players. Relaxing those restrictions could be helpful. Of course, there are going to be reasons for why there were a limited number of licenses in the first place, so there’s going to be a question of balancing the trade-off there.