When commodity prices spiked in 2007-08, it took most people by surprise. The global commodity “super cycle” had crept up upon us stealthily. This month commodity markets have been jolted again. Energy, metals, bullion and agricultural commodities have all hit multi-year lows. Only this time, there is a method to the madness.

When commodity prices spiked in 2007-08, it took most people by surprise. The global commodity “super cycle” had crept up upon us stealthily. This month commodity markets have been jolted again. Energy, metals, bullion and agricultural commodities have all hit multi-year lows. Only this time, there is a method to the madness.

The large investments in mining and refineries made since the 2008 boom are now coming on stream, which has brought global demand and supply finally close to equilibrium. Food crops are bolstered by good agronomical weather for two consecutive seasons. Add to this a dollar that hasn’t been stronger since Bretton Woods and you have the perfect conditions to foster bearishness.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Crude oil prices have defied the price trend you would expect given the geopolitical tensions in the Middle East, Africa, and Central Europe because of slowing demand and well supplied markets. Oil demand could dwindle further due to an economic slowdown in Asia and lower US imports as it scales up shale oil production. US became the world’s largest natural gas producer in 2009 and may become the largest oil producer in a few years.

US oil production achieved its highest July level in 28 years, and oil imports declined to their lowest July level in 19 years. US refineries are taking advantage of the low oil prices by maximizing their processing volumes and raising exports, especially to Europe. At the same time, the oil that is no longer being bought by the US is also flooding the world market and pushing prices downwards.

New metals supply is coming on stream, triggered by investments after the 2007-2008 boom. China, which contributes 45% of the demand for copper and aluminum, remains in surplus and capacity continues to rise strongly. The International Aluminum Institute estimates China produced almost 9% more in the first seven months of the year versus the same period last year. But the Chinese real estate market is oversupplied and fewer new projects are likely to start in future. This will affect metal demand. Iron ore is in oversupply from higher production in Australia, which is determined to give China stiff competition.

A firm US dollar and rising equity markets have curbed investment demand for gold. Recent bouts of safe haven buying due to geopolitical tensions have not been able to staunch the significant outflows from gold, platinum and palladium ETFs. Chinese gold imports from Hong Kong declined for the fifth consecutive month in July to just 22 tons—their lowest level for more than three years. At this rate, China may import less than 700 tons of gold from Hong Kong this year, down from 1,100 tons last year. India’s gold imports are already in doldrums.

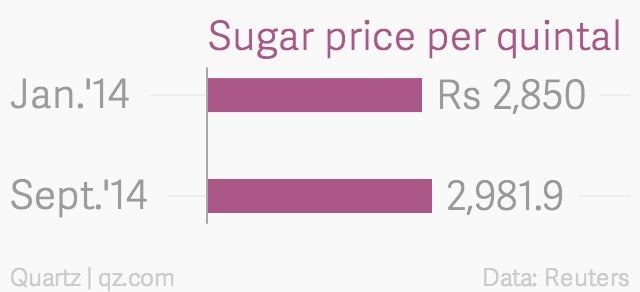

After a slow start, the overall monsoon deficit in India narrowed to 11% by early September. Planting is complete in paddy, oilseeds, corn, pulses, cotton and sugarcane. Agriculture ministry data shows that planted acreage is almost the same as last year. The global storage bins are full. Global wheat supply remains ample, says the International Grains Council. US is anticipating record yields of corn, cotton and soyabean, which will result in higher global stocks. Palm oil production has now entered the seasonally high cycle in Malaysia and Indonesia. Indonesian efforts to boost use of palm oil in making biofuel have missed expectations. Sugar too has a global surplus, despite unfavourable weather in Brazil and India. International Sugar Organization estimates that stock levels have risen significantly since 2010-11. India is poised for record cotton crop on the back of higher acreage and yields.

Who will benefit from the market cooling off? Manufacturers—industrial and food processing—will enjoy higher operating margins due to cheaper raw material and energy. Falling food prices have brought down the Wholesale Price Index to a five-year low in August. But it will yield tangible benefits for political parties headed for state polls next month and the RBI’s monetary policy only when the Consumer Price Index gives up its stubborn resistance and follows suit. Luckily, however, the drop in bullion prices is well-timed with the festival season starting this weekend. So shoppers can splurge on jewellery, silver artefacts and diamonds.

Unfortunately, those who gain may be outnumbered by those who will rue this decline in prices. India’s 50 million farmers will have little reason to celebrate when the harvests hit the market from October as selling prices are already precariously close to breakeven levels. Rural incomes will, therefore, take a hit. This has a cascading effect on rural demand for everything from shampoos, soaps and clothes to motorbikes, mobile phones, and cement.

Banks will have to review both their priority sector and their collateral financing portfolios for potential bad loans. Collateral financing, in particular, will have to be re-visited as the value of commodity stocks continues to decline with each passing week. On the other side, commodity processing companies, such as sugar mills, seeking working capital loans will find it an uphill task to maintain their existing lines. Public sector companies, such as FCI, Nafed and CCI, holding commodity stocks, will also have to brace themselves for their declining value.

Commodity exporters—companies and nations—are also disadvantaged by the falling market. The Australian dollar slumped to a seven-month low against the US dollar Monday on concerns that a slowdown in China’s economy would push commodity prices lower and weigh on Australia’s growth prospects. Analysts at research outfit Bernstein have reportedly calculated that for every dollar fall in the price of iron ore, which accounts for more than 80% of Rio Tinto profits, its assets lose $1.5 billion in value. Rio is the world’s second-largest producer of iron ore.

The real takeaway is that this situation may be here to stay in the medium term unless global economic growth ratchets up. This means people have to mothball their boom-time coping strategies and think afresh about how to handle this new reality. Because the dangers from a falling market are just as real and perhaps even larger, since they stem from eroding asset value. Hedging risk, short selling, forward contracts that lock prices, timely sales of physical stocks, cost management, and finding new sources of demand through value addition are all ways that will find early adopters as the reality sinks in. Will the transition be easy? No. But then bear markets were never for the faint of heart.