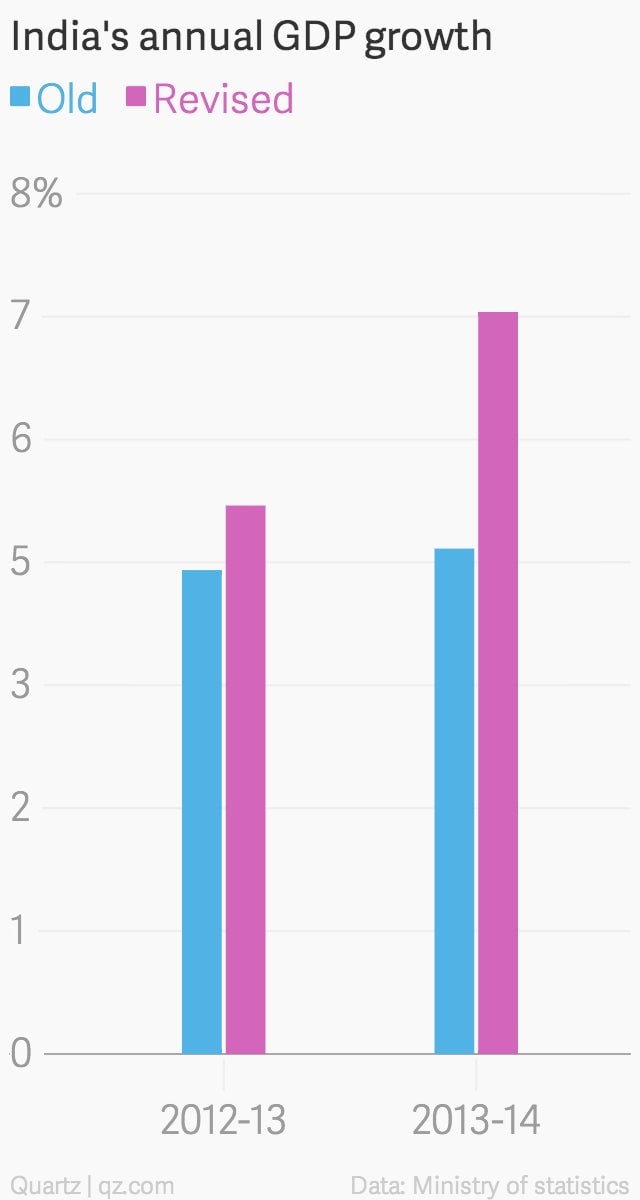

This morning, India’s GDP growth for the 2013-14 financial year was 4.7%.

By evening, it had suddenly jumped to 6.9%.

What gives?

What happened is that the Indian government decided to change the way it measures economic output. To be precise, it’s a “base year” revision (pdf), where statisticians shift the reference year for measuring inflation-adjusted growth from 2004-05 to 2011-12. A few other tweaks have also been made, including the addition of new data sources, classification systems, and items like LCDs and smartphones to the country’s national accounts.

This was the most comprehensive overhaul ever of India’s GDP measurement method, Pronab Sen, chairman of the National Statistical Commission, told The Mint newspaper. It will bring the country’s measurement techniques in line with global best practices.

Periodic revisions are common practice around the world. The UK and Nigeria both saw their GDP jump after changing the way they measure national output, for example.

In India’s case, ratings agency Ind-Ra said in a report (pdf) that “the base year should be changed frequently considering fast-changing economic structure and to update/estimate national accounts based on latest available information.” And given the slow recovery, the revision to growth could also make it easier for the government to meet its challenging fiscal deficit target.