From Kodak's refusal to embrace digital to Theranos's fabricated science, tech history is full of companies that had resources, talent, and timing — and still collapsed. Here's what each one got wrong

Annatsach / Wikimedia Commons (CC BY-SA 4.0)

Tech failure has a mythology problem. The standard narrative — the visionary founder who moved too fast, the corporate giant that failed to innovate, the startup that ran out of runway — flattens the specific, instructive details of what actually went wrong into archetypes that are satisfying but not particularly useful. Kodak invented the digital camera and then failed to commercialize it, which fits the incumbent-disruption story perfectly. But the more interesting question is not why Kodak didn't commercialize digital photography — it did, eventually — but why the specific decisions it made in the decade between the invention and the commercialization produced a company unable to survive the transition it had pioneered.

The companies in this list failed for reasons that are specific, documented, and in most cases avoidable in retrospect. Several failed because of a single catastrophically bad strategic decision whose consequences took years to materialize. Several failed because of a cultural failure that corrupted every subsequent decision. Several failed because of a simple timing problem — the right product for a market that did not yet exist, or the right product for a market that had already moved on. Several failed because the people running them were committing fraud, which is a specific kind of failure whose lesson is straightforward but whose human consequences were severe.

The selection covers the full range of tech failure modes — incumbent paralysis, startup delusion, platform misjudgment, hardware timing errors, fraud, and the specific failure of companies that were genuinely excellent at one thing and confused that excellence with a general capacity to succeed at anything. The list ranges from the 1990s dot-com era through the 2020s, covering failures whose lessons are as relevant to the current generation of tech companies as they were to the ones that experienced them.

A note on what counts as failure: several companies on this list were acquired rather than going bankrupt, and a few are technically still operating in reduced form. The failure being analyzed in each case is the specific failure of the company's original mission, leadership, or market position — the end of the company as a meaningful independent force in its industry — rather than a legalistic definition of corporate death.

Eastman Kodak / Wikimedia Commons

Kodak's failure is the most frequently cited example of incumbent disruption in business literature, and the standard telling — a company that invented digital photography but couldn't bring itself to cannibalize its film business — is accurate as far as it goes. But it understates the specificity of Kodak's strategic error, which was not ignorance of digital photography but a deliberate choice to extract maximum value from the film business while managing the transition to digital at a pace that preserved the incumbent's advantage. The problem was that the transition was not manageable — it was a cliff rather than a slope.

Steve Sasson, a Kodak engineer, invented the digital camera in 1975. Kodak's management reviewed the invention, understood its implications, and made a calculated decision not to commercialize it aggressively because digital photography would destroy the film business that generated Kodak's revenue and profits. The calculation was rational in the short term and catastrophic in the long term: by the time Kodak moved seriously into digital, the market had been shaped by companies — Sony $SONY, Canon, Nikon — that had no film business to protect and had competed aggressively on price and features that Kodak's cost structure could not match.

Kodak's second specific error was in its digital strategy when it finally committed: it focused on printing digital photographs — using digital capture to generate demand for its photo printing services — rather than on the broader digital imaging ecosystem. This strategy was coherent from the perspective of protecting the existing business model but missed the direction of the market, which was moving toward sharing photographs digitally rather than printing them. Kodak was optimizing for the wrong endpoint of the digital transition.

The bankruptcy in 2012 — 137 years after the company was founded — was the endpoint of decisions made in the 1980s and 1990s. The lesson is not that incumbents should ignore financial considerations when disruption approaches but that the deliberate pacing of a technological transition to protect existing profits is a strategy that works only when the transition pace can actually be controlled — and it rarely can.

Blockbuster Entertainment, Inc. / Wikimedia Commons

Blockbuster's failure is, like Kodak's, a canonical disruption story — the video rental giant that passed on the opportunity to acquire Netflix $NFLX in 2000 for $50 million and subsequently lost its entire business to the company it declined to buy. The Netflix story is accurate. The deeper story is why Blockbuster passed.

In 2000, Netflix was a DVD-by-mail service losing money and looking for an exit. Blockbuster's CEO John Antioco met with Netflix's Reed Hastings and Marc Randolph and declined to acquire the company. The reason, according to accounts from the meeting, was that Blockbuster's leadership considered Netflix a niche business that would not threaten the store-based model that Blockbuster's entire revenue structure depended on. This was plausible in 2000, when broadband penetration was minimal and streaming was not yet a viable delivery mechanism.

Blockbuster's real failure came later, when it had a genuine opportunity to compete. In 2004, Antioco launched Blockbuster Online, a subscription service that directly competed with Netflix, and eliminated late fees — a policy that was genuinely competitive and that Netflix's internal analysis identified as a serious threat. Blockbuster was winning the competitive battle. Then its board, pressured by activist investor Carl Icahn, fired Antioco, reversed the no-late-fees policy, and gutted the online business to protect short-term margins. The company that might have competed with Netflix was dismantled from within by investors who could not see past the quarterly earnings report.

The specific lesson is not that Blockbuster failed to see the future but that it saw the future, started to respond, and was prevented from completing its response by a governance failure that prioritized short-term financial metrics over the strategic investment required to survive. This is a more common and more instructive failure mode than simple incumbent blindness.

News Corporation / Wikimedia Commons

Myspace was the dominant social network in the United States from 2005 to 2008, at its peak attracting 100 million users and selling to News Corp for $580 million in 2005 — a sale price that represented a triumph for its founders and a disaster for News Corp. By 2011, Myspace had been sold again for $35 million, having been overtaken by Facebook $META so completely that its name had become a byword for platform failure.

The specific mistake Myspace made was prioritizing advertising revenue over user experience — and making every product decision through the lens of maximizing ad impressions rather than engagement quality. Myspace pages were notoriously cluttered, slow, and aesthetically chaotic, because users were allowed to customize them with autoplay music, animated backgrounds, and arbitrary HTML that made pages difficult to navigate and extremely slow to load on the connections of the mid-2000s. The chaos was a feature for Myspace's management — more page elements meant more opportunities for advertising — and a failure for users, who migrated to Facebook's cleaner, faster interface with remarkably little friction.

Myspace's second error was in how it managed the talent that was building it. The company was absorbed into the bureaucracy of News Corp immediately after the acquisition, replacing the scrappy development culture with corporate approval processes that slowed product iteration at precisely the moment when Facebook was iterating rapidly. Engineers who might have built the features that kept Myspace competitive were instead navigating approvals for changes that needed to happen in weeks rather than months.

The platform competition lesson is specific: in social networks, user experience quality is the product, not a feature, and the choice to degrade user experience for short-term ad revenue is a choice that accelerates platform abandonment.

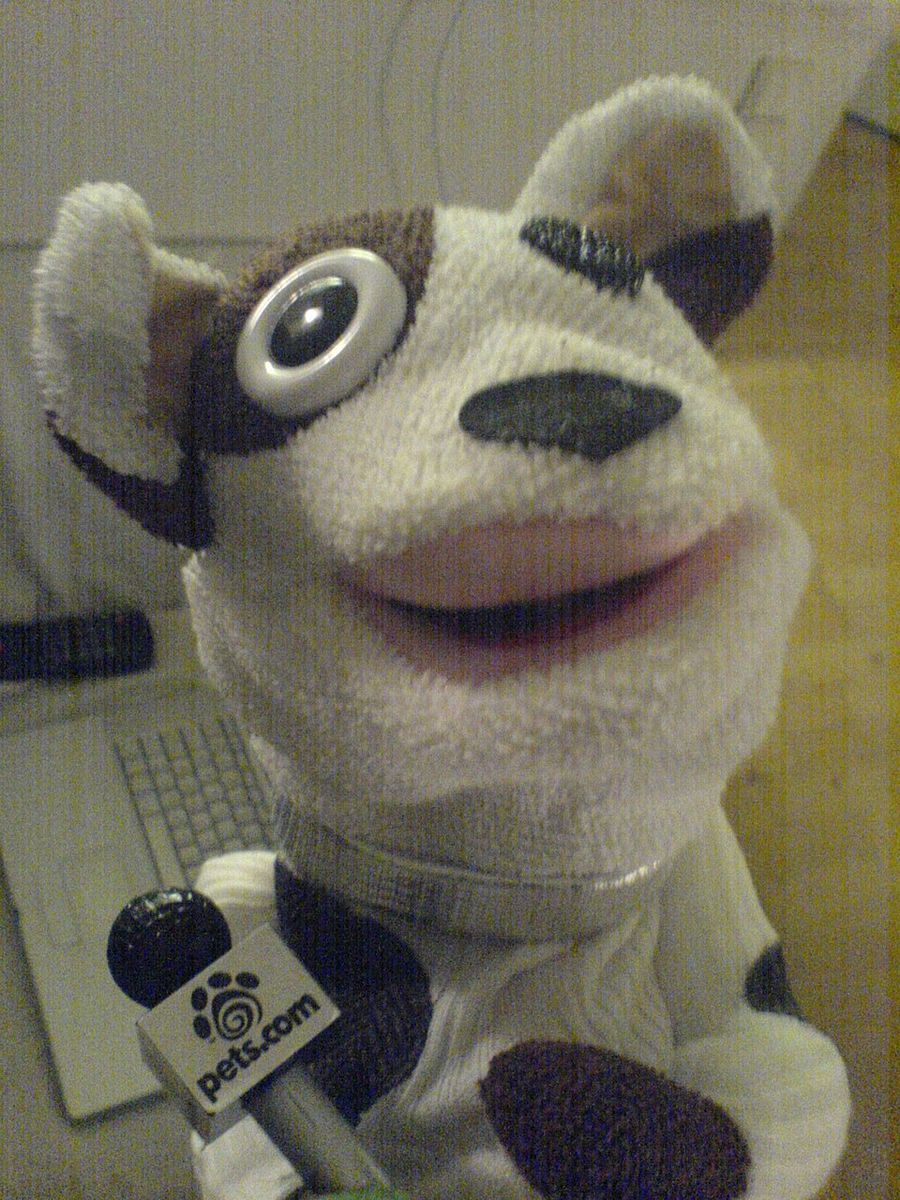

Jacob Bøtter /Flickr via Wikimedia Commons (CC BY 2.0)

Pets.com is the canonical dot-com bubble failure — the company that raised $82.5 million in a February 2000 IPO, spent $11.8 million on a Super Bowl ad featuring a sock puppet, and went bankrupt nine months later with $61 million in liabilities. Its failure has been used ever since as the definitive example of dot-com excess, but the specific reasons it failed are more instructive than the cultural memory of the sock puppet implies.

Pets.com failed primarily because its unit economics were catastrophically negative and its leadership either did not understand this or chose not to address it. The company sold pet food and supplies online at prices below its cost of acquisition and delivery, subsidizing customer growth with venture capital and IPO proceeds in the expectation that scale would eventually produce profitability. The problem was that the unit economics did not improve with scale: delivering heavy pet food nationwide by courier to individual households is expensive regardless of volume, and the cost structure of the business was not competitive with established pet supply retailers who could deliver large orders to stores efficiently.

The board and management knew the unit economics were unsustainable — this information was available in the financial statements that accompanied the IPO — but the market conditions of 1999 and early 2000 rewarded growth metrics over profitability, and the company was funded and valued on the assumption that the economics would improve or that a larger acquirer would absorb the losses. When the market turned in late 2000, the funding dried up, and the company that could not survive without continuous capital infusion did not survive.

The specific lesson is about the relationship between user growth and unit economics: growth that is purchased at a per-unit loss does not become profitable at scale unless the unit economics improve with scale. Pets.com's unit economics did not improve with scale, and the company's entire capital structure depended on the assumption that they would.

Nokia Corporation / Wikimedia Commons

Nokia was the world's largest mobile phone manufacturer from 1998 to 2012, commanding peak market shares of over 40% globally, and its decline from that dominant position to near-irrelevance in the smartphone era is one of the most studied strategic failures in business history. The specific causes are more nuanced than the standard "Nokia missed the smartphone" narrative suggests.

Nokia did not miss the smartphone. It had touchscreen smartphone prototypes in development before Apple $AAPL's iPhone was announced, and its internal research teams understood the direction mobile computing was moving. What Nokia missed was the software ecosystem — the app store model that Apple introduced in 2008 — and the organizational capability to move from hardware manufacturing excellence to software platform management.

Nokia's operating system, Symbian, was powerful enough for feature phones but was not architected for the application-centric smartphone use case that the iPhone demonstrated. The decision to continue investing in Symbian rather than transitioning to a modern operating system — driven by the enormous installed base of Symbian developers and devices — was a classic innovator's dilemma: the existing platform was too successful to abandon and too limited to compete with the new paradigm.

The organizational failure was equally significant. Nokia's culture had become politically complex by the mid-2000s, with middle management layers that filtered bad news upward and created the illusion that competitive threats were less severe than they were. Internal research that identified Symbian's limitations was systematically downplayed. The consequence was a leadership team that was making strategic decisions on information that underrepresented the severity of the competitive challenge.

The Microsoft $MSFT acquisition in 2013 — which preserved some Nokia assets but effectively ended the company's independent existence in mobile — was the endpoint of decisions made between 2007 and 2011, when the competitive window was still open and the transition still possible.

Glenn Fawcett / Wikimedia Commons

Theranos is the tech failure on this list that is not a strategic error but a fraud — and its inclusion reflects the importance of understanding the specific mechanisms by which fraud in the technology sector is enabled and sustained. Elizabeth Holmes and her company claimed to perform hundreds of blood tests from a single finger-prick of blood using a proprietary device called Edison. The device did not work as claimed. Holmes and her company knew it did not work as claimed and covered the fact up for a decade, subjecting patients to inaccurate medical test results that could have and may have led to harmful treatment decisions.

The specific mechanisms that allowed Theranos to operate for a decade despite the non-functionality of its core product are instructive. Holmes raised capital from investors who did not demand scientific validation of the technology's claims — the laboratory science was proprietary and the investors deferred to Holmes's authority on its viability. The board of directors was composed of political and military figures without biotechnology expertise who were not equipped to evaluate the technical claims. Partnerships with Walgreens $WBA and Safeway — whose technical due diligence was inadequate — lent the company operational legitimacy. And Holmes's personal charisma and the cultural moment of female tech founder celebration created a disincentive for skepticism that allowed obviously problematic claims to circulate unchallenged.

The lesson is not that investors should always distrust founders but that the specific combination of secrecy about core technology, implausible performance claims, a board without relevant expertise, and a cultural disincentive to challenge the narrative is a pattern that recurs in tech fraud, and whose recognition is a prerequisite for prevention.

.svg-1920x365.png)

Yahoo! / Wikimedia Commons

Yahoo's failure is particularly instructive because it involved not one but two decisions that, had either gone differently, would have produced one of the most valuable companies in technology history. In 2008, Microsoft $MSFT offered $44.6 billion to acquire Yahoo. Yahoo's board, led by CEO Jerry Yang, rejected the offer as undervaluing the company. Yahoo's market capitalization at the time of the rejection was approximately $42 billion; at the time of the company's sale to Verizon $VZ in 2016, it was approximately $5 billion.

The earlier decision was more consequential. In 2005, Yahoo acquired a 40% stake in the Chinese e-commerce company Alibaba for $1 billion. When Alibaba IPO'd in 2014 at a valuation of approximately $168 billion, Yahoo's stake was worth approximately $40 billion — more than Yahoo's entire corporate value. Rather than recognizing this as a signal that its own core business had been surpassed by its investment, Yahoo spent the intervening decade attempting to compete with Google $GOOGL in search and with Facebook $META in social, making a series of acquisitions (Tumblr for $1.1 billion, acquired when it had 30 employees, whose value was subsequently written down to zero) that did not produce competitive positioning in either market.

Yahoo's core strategic failure was the inability to define what kind of company it was. It began as a directory and portal, transitioned toward search, was overtaken in search by Google, and never made a clear decision about whether it was a media company, a technology company, or an advertising platform. The lack of strategic clarity produced an inability to make investment decisions against a coherent long-term plan, and the resulting execution was diffuse rather than focused at precisely the moment when Google and Facebook were making focused bets that defined their categories.

WeWork / Wikimedia Commons

WeWork is the most dramatic recent example of the gap between a company's stated valuation and its actual business quality — a commercial real estate business that convinced its investors and its own leadership that it was a technology company, and that the value of a technology company could be applied to it by sufficient repetition of the word "technology" in investor presentations.

At its peak private valuation of $47 billion in early 2019, WeWork was the most valuable startup in the United States. Its IPO prospectus — filed in August 2019 — presented a business losing approximately $219,000 per hour and described the company using language ("elevating the world's consciousness") that was widely mocked by financial analysts. The IPO was withdrawn, co-founder and CEO Adam Neumann was forced out, and SoftBank — which had invested approximately $18 billion — took control of the company at a valuation of approximately $8 billion. WeWork filed for bankruptcy in 2023.

The specific failure mechanisms were multiple. WeWork's business model — leasing long-term commercial real estate and subletting it on short-term flexible terms — was not new (it was essentially the serviced office model that IWG/Regus had operated profitably for decades) and was fundamentally mismatched with the "technology company" valuation it received. The company's cost structure required continuous occupancy growth to service its lease obligations, making it extremely vulnerable to any economic slowdown.

Neumann's governance failures — personal enrichment at the company's expense, chaotic management, and the elevation of personality over operational discipline — compounded the structural problems. But the primary lesson is about the specific danger of investors who accept the self-description of a business rather than analyzing its actual economics.

Quibi Holdings LLC / Wikimedia Commons

Quibi — the short-form mobile video platform founded by Jeffrey Katzenberg and Meg Whitman that raised $1.75 billion before launching in April 2020 and shut down six months later — is the most rapid and most expensive failure of a well-funded consumer media product in recent memory. Its failure was comprehensive and illustrates several distinct failure modes simultaneously.

The fundamental product error was the assumption that viewers wanted high-quality, professionally produced short-form video specifically on their phones in landscape mode. Quibi's technology — Turnstile, which adapted video to both portrait and landscape phone orientations — was genuinely innovative. Its content was expensive and produced by major talent. Its pricing (roughly $5 to $8 per month) positioned it above free alternatives. The product that resulted was a premium short-form mobile video service launched in the middle of a pandemic that confined everyone to their homes.

The timing could not have been worse. Quibi's value proposition — premium video entertainment for people on the go, during commutes, in waiting rooms, during lunch breaks — assumed a lifestyle that the COVID-19 pandemic eliminated entirely in its first week of operation. Users at home, with full access to television screens and laptops, had no motivation to watch premium content on their phones in short chunks when Netflix $NFLX, YouTube, and TikTok were available without restriction.

But the pandemic was an accelerant of failure rather than its cause. The specific product problem was that Quibi was solving for a need that users did not express: nobody was looking for high-quality short-form content specifically for phone viewing, and the evidence for that demand was not available from users but from the founding team's intuition about how media consumption would evolve. The product was built from a theory rather than from demonstrated user demand.

Google / Wikimedia Commons

Google $GOOGL Plus — Google's attempt to create a social network competitive with Facebook $META, launched in 2011 — was, in terms of technical execution, a polished and well-resourced product. In terms of strategic understanding of what makes a social network valuable, it was a failure that lasted eight years before being quietly shut down in 2018.

The specific mistake was the assumption that a social network's value is in its features rather than in its network. Google Plus launched with genuine innovations — Circles, which allowed nuanced control of who saw different types of content, and Hangouts, a video chat feature that was superior to anything Facebook offered at the time. These features were real improvements on Facebook's equivalent functionality. They did not produce significant user adoption because the users who might have valued them were already on Facebook, and Facebook's value to any individual user was not its features but its network — the specific people on it.

A social network's value is almost entirely in its connections. A person's existing friends, family, and professional contacts are on the network they joined first, and no feature improvement by a competitor is sufficient to motivate the migration of an entire social graph to a new platform. The switching cost of a social network is not the effort of creating a new account but the effort of convincing everyone you know to move with you.

Google compounded the problem by requiring Google Plus accounts for various Google services — YouTube commenting, Google Maps reviews — in an attempt to build network scale artificially. The strategy produced account creation without genuine engagement, inflating user numbers without building actual social value. By 2014, Google Plus had a large number of dormant accounts and a small number of active users — exactly the wrong ratio for a social network.

Vine Labs, Inc. / Wikimedia Commons

Vine — the six-second looping video platform launched in 2013 and acquired by Twitter $TWTR before it launched — was the original short-form social video platform, the product that established a creative format (the six-second loop) and a creator community whose work defined the aesthetic of internet video for several years. It was also shut down in 2017, before TikTok had become significant, because Twitter failed to respond to the competitive threat that Instagram's video features and Snapchat represented.

Vine's failure is a study in platform mismanagement. The specific error was Twitter's failure to give Vine's creator community the monetization tools that would have kept the most popular creators on the platform. In 2015, a group of Vine's top creators — collectively responsible for a large proportion of the platform's engagement — met with Twitter leadership and asked for revenue sharing, better creation tools, and direct communication with platform management. Twitter declined to offer any of these things.

The creators left. Some went to YouTube, some to Instagram, some to other platforms. Without the top-tier creators, the unique content that differentiated Vine from other video platforms was gone, and ordinary users followed. Vine's audience had been built on the work of its creators, and the failure to retain those creators — which would have cost Twitter a modest fraction of its advertising revenue — produced the collapse of the entire platform.

The specific lesson is about the asymmetric importance of power users in platform economics: a small number of creators produce a disproportionate share of the content that drives engagement, and the cost of retaining them is small relative to the value they generate. Twitter chose not to pay this cost, and Vine ceased to exist.

Friendster / Wikimedia Commons

Friendster was the first significant social network — launching in 2002, three years before Myspace and four years before Facebook $META — and its failure is one of the most specifically technical of the major social network collapses. It did not fail because of a strategic error in the conventional sense. It failed because its servers could not handle the traffic its own growth generated.

In 2003 and 2004, Friendster was experiencing explosive user growth — adding millions of users in months — and its technology infrastructure could not scale to support the load. Page loads took 30 to 40 seconds on a bad day, and a bad day was most days. Users who could not reliably load the site stopped using it. The network effects that drive social network growth — each new user making the network more valuable to existing users — ran in reverse: each departure made the network slightly less valuable, which encouraged more departures, in a declining spiral that the infrastructure failures had initiated.

Friendster's management made the situation worse by deleting fake profiles — the "Fakesters" who had created profiles for celebrities, fictional characters, and cultural figures — in a misguided attempt to enforce a real-identity policy. The Fakesters were disproportionately the profiles that drove engagement and discovery; their removal reduced the network's content diversity and entertainment value at precisely the moment when performance issues were already driving users away.

Google $GOOGL offered to acquire Friendster in 2003 for $30 million. Friendster's management declined. In 2011, Friendster sold its patent portfolio to Facebook for $40 million and shut down its social network entirely, having failed to monetize or preserve the first-mover advantage it had held in the most valuable internet category of the decade.

Tdorante10 / Wikimedia Commons (CC BY-SA 4.0)

The Segway — the self-balancing personal transportation device unveiled by Dean Kamen in 2001 with enormous pre-launch hype — is included on this list not because the company committed fraud or made a catastrophic strategic error but because it is the purest example of a product failure caused by the mismatch between a technology's capabilities and actual demand for its application.

Before its launch, Kamen and his investors claimed the Segway would be more important than the personal computer, would be adopted by millions of consumers, and would require cities to redesign their infrastructure to accommodate it. These claims were made by serious, intelligent people who had raised $90 million in funding and who genuinely believed them. The product that emerged was a well-engineered piece of technology that was expensive ($5,000), required special permissions to use in many jurisdictions, could not be taken on public transit, was difficult to store, and solved a transportation problem — the last mile — that most urban pedestrians did not experience as a problem sufficient to justify the cost and complexity.

The Segway sold 24,000 units in its first six years against its projections of 10,000 per week. The company was eventually sold to a British investor for an undisclosed amount — reported to be less than the cost of a single year's marketing budget.

The lesson is about the specific danger of confusing technological capability with market demand: the fact that a technology can do something does not establish that enough people want the thing done badly enough to pay for it. The Segway worked as advertised. What it did was simply not valuable enough to most people at its price point.

Credit: Wikimedia Commons

Jawbone was one of the most successful consumer technology companies of the early 2010s — a hardware manufacturer that produced popular Bluetooth speakers and fitness trackers, raised approximately $900 million in venture capital, and achieved a peak valuation of approximately $3 billion. It went bankrupt in 2017, unable to repay its creditors, its inventory liquidated and its technology assets acquired by a healthcare company.

The specific failure mechanism was the transition from consumer hardware to healthcare technology — a pivot that was never completed and that consumed the company's resources without producing revenue. Jawbone's fitness trackers competed directly with Fitbit and Apple $AAPL Watch in a market where Apple's distribution and Fitbit's established user base were decisive advantages. Rather than finding a differentiated position in consumer wearables or accepting the competitive pressure, Jawbone's CEO Hosain Rahman decided to pivot the company toward clinical healthcare applications — continuous health monitoring for medical purposes — a market that required regulatory approval, clinical validation, and a sales infrastructure the company did not have.

The healthcare pivot was funded by continued venture capital raises that priced the company at consumer electronics valuations while requiring healthcare company timelines. The investors who funded the pivot did so on the basis of projections that assumed regulatory approval and clinical adoption that never materialized. The company's cash was exhausted servicing its debt and funding a transition that produced no revenue.

The specific lesson is about the danger of the strategic pivot when it is used to escape a competitive problem rather than to address an identified market opportunity. Jawbone's pivot was a retreat from a market it was losing rather than an advance toward a market it had evidence for winning.

Rama & Musée Bolo / Wikimedia Commons (CC BY-SA 2.0 fr)

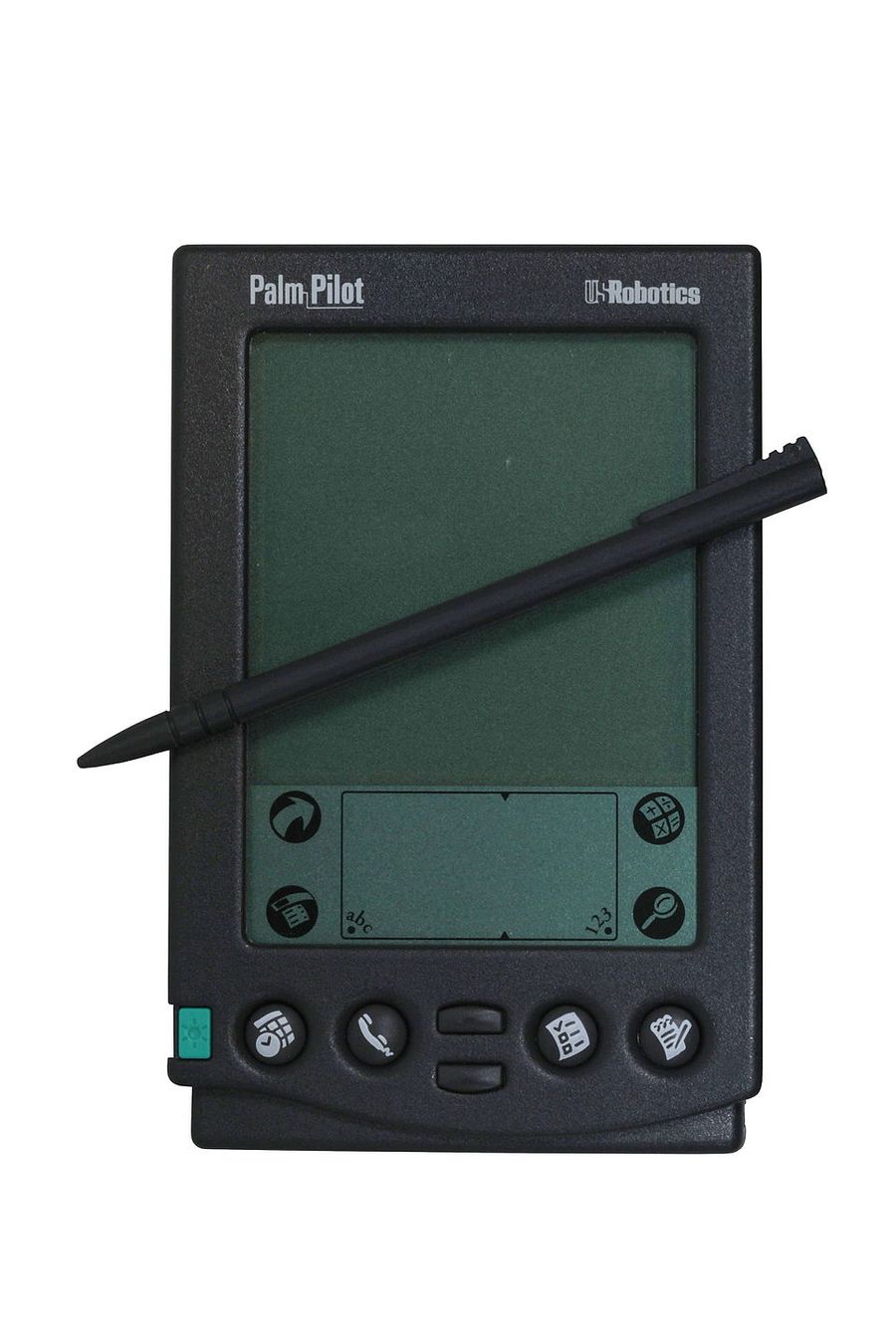

Palm invented the personal digital assistant market with the PalmPilot in 1996, dominated it through the late 1990s, and was eventually destroyed by the smartphone market that its own technology helped make possible. Its failure is one of the more technically specific in tech history: the company that built the first successful handheld computing platform failed to extend that platform to the phone category that would replace it.

Palm's platform — PalmOS, with its Graffiti handwriting recognition and its library of third-party applications — was the first mobile software ecosystem, predating the App Store by a decade. Palm developers built thousands of applications on the platform, and the ecosystem gave the PalmPilot the utility advantage over competing devices that software platforms consistently produce for the hardware they run on.

The failure happened in the transition to smartphones. Palm produced smartphones — the Treo series — that were genuinely popular and commercially successful. But Treo smartphones ran PalmOS, and PalmOS was not designed for the always-connected, multimedia, finger-touch interface that smartphones would require. The architecture that had served the PDA market well was a constraint in the smartphone market.

Palm recognized the problem and developed a new operating system — webOS, launched with the Palm Pre in 2009 — that was technically sophisticated, conceptually ahead of its time, and commercially too late. The iPhone had been released in 2007 and Android in 2008. WebOS was better in some ways than both — its multitasking model was widely praised by reviewers — but it launched into a market where Apple $AAPL and Google $GOOGL had already established distribution, ecosystem, and consumer mindshare that Palm could not displace. HP $HPQ acquired Palm in 2010 for $1.2 billion and discontinued webOS hardware within 18 months.

Credit: Wikimedia Commons

AOL was the dominant internet service in the United States through the 1990s, introducing millions of Americans to the internet through its CD-ROM distribution model and its walled-garden online experience. At its peak in 2000, it had 26 million subscribers and a market capitalization that allowed it to acquire Time Warner — one of the largest media companies in the world — in a $165 billion deal that is still cited as the worst corporate merger in history.

The specific failure was twofold. The merger itself destroyed value on a scale that requires separate examination: the combined company wrote down approximately $99 billion in goodwill in 2002, the largest accounting loss in corporate history to that point, reflecting the collapse of AOL's valuation as the dot-com bubble burst. The merger was consummated at the peak of AOL's stock price, and the value transferred to Time Warner shareholders was almost entirely paper wealth that evaporated within two years.

The underlying business failure was the transition from dial-up internet to broadband. AOL's walled-garden model — where users paid for access to AOL's curated content and services — was designed for the dial-up era, when the internet's open web was slow enough that curation had value. As broadband made the open internet fast and accessible, AOL's proprietary content and services became irrelevant: users could get better content, more quickly, without the AOL intermediary.

AOL's response — maintaining the subscription model rather than pivoting to free, advertising-supported access — was a rational defense of existing revenue but a failure to recognize that the competitive moat was gone. The company spent the first decade of the 21st century in managed decline, eventually being sold to Verizon $VZ in 2015 for $4.4 billion — a fraction of the valuation that had made it the acquirer of Time Warner fifteen years earlier.

Boo.com / Wikimedia Commons

Boo.com was a British online fashion retailer that raised $135 million in 1999, spent most of it in 18 months, and went bankrupt in May 2000 before the dot-com crash that destroyed most of its contemporaries — failing not because the market turned against it but because its own operations were catastrophically mismanaged.

The specific operational failures at Boo.com were so numerous and so well-documented by Ernst Malmsten (one of its founders) in his memoir that it has become a business school case study in startup operational mismanagement. The company operated offices in London, New York, Munich, Paris, Amsterdam, and Stockholm simultaneously before generating a dollar of revenue, each staffed with expensive talent. It built its website using technology that required the Flash plugin and a high-speed internet connection to render — excluding most users in an era when many were still on dial-up. The website's launch was delayed six months from its planned date, burning through the capital that was supposed to fund the first year of operations.

The culture at Boo.com, as Malmsten's memoir describes it, was characterized by the assumption that the money would keep coming — that venture capital was a renewable resource rather than a finite one with conditions attached. When the company ran out of money in spring 2000, it sought additional investment at a valuation that its performance did not support and could not secure it.

The KPMG liquidator who managed the bankruptcy sold Boo.com's brand and technology for $375,000 — approximately 0.3% of the capital the company had raised. The website's remaining inventory — fashion goods that had never been sold — was liquidated separately.

Credit: Fandom Wiki

Lernout & Hauspie was a Belgian speech recognition and language technology company that was, at its peak, the second-largest software company in Europe by market capitalization — and also, it turned out, engaged in systematic accounting fraud that inflated its revenue by hundreds of millions of euros through fictitious sales to fictitious customers in South Korea.

The specific fraud mechanism was relatively unsophisticated in retrospect: L&H created a network of distribution companies in South Korea, sold its software to them at inflated prices, and recorded these sales as revenue despite the fact that the distribution companies had no genuine customers and the sales had no economic substance. The Wall Street Journal investigation that exposed the fraud in 2000 found evidence for fictitious revenue of approximately $350 million.

L&H's fraud illustrates a specific pattern in tech fraud: the use of geographic remoteness to obscure fabricated sales. The South Korean distribution network was sufficiently distant from L&H's Belgian headquarters, and from the American analysts and investors who were covering the stock, that genuine due diligence was difficult. The complexity of the scheme — multiple layers of distribution companies with partial ownership relationships — made verification time-consuming, and in the bull market of 1999 there was little appetite for the time investment that verification required.

Microsoft $MSFT had briefly considered acquiring L&H for approximately $1 billion. The fraud was discovered before the acquisition was completed. L&H's stock, which had reached $72 per share at its peak, was worthless within months of the WSJ's reporting.

Credit: Wikimedia Commons

Rdio was a music streaming service founded in 2010 by two of the co-founders of Skype — Janus Friis and Niklas Zennström — that was, in the assessment of most people who used it, superior in product quality to Spotify $SPOT, its primary competitor. It had a cleaner interface, better music discovery features, and a social layer that was more thoughtfully designed than Spotify's equivalent. It went bankrupt in 2015 and sold its assets to Pandora for $75 million.

Rdio's failure is one of the clearest examples in tech of the principle that the better product does not necessarily win — specifically, that product quality is not a sufficient competitive advantage in markets where distribution and pricing create decisive consumer switching barriers.

Rdio charged a minimum of $10 per month for its service from the day it launched and never offered a free tier. Spotify launched in the United States in 2011 with a free ad-supported tier that allowed users to try the service without any financial commitment. The free tier was a loss-leading user acquisition strategy that Rdio's investors declined to fund. The result was that Spotify built a large user base of free users who converted to paid at rates that made the economics work at scale, while Rdio had a smaller base of paid users who were more engaged but not large enough to fund the label licensing costs that streaming economics require.

The specific lesson is about the relationship between free-tier user acquisition and streaming economics: in a market where every competitor has access to the same content library, the switching cost is low, and the conversion from free to paid at scale is the primary business model, declining to offer a free tier is a decision to compete at a structural disadvantage that product quality cannot overcome.

Juicero / Wikimedia Commons

Juicero was a San Francisco startup that raised $120 million in venture capital to sell a $700 internet-connected juicing machine that squeezed proprietary produce packets into a glass of juice. It was shut down in 2017 after a Bloomberg reporter discovered that the packets could be squeezed by hand — without the machine — in approximately the same time and with approximately the same yield as the $700 press produced.

The Bloomberg story — headlined "This Man Spent Two Years Trying to Reinvent Juice" — was the specific catalyst for Juicero's collapse, but the vulnerability it exposed had been present from the beginning. The company's entire value proposition rested on the necessity of the machine: if the packets could be squeezed without it, the machine was unnecessary, and if the machine was unnecessary, there was no reason to pay $700 for hardware or $5 to $8 per packet for proprietary produce. The hand-squeeze discovery did not create this problem — it revealed it.

Juicero's funding was enabled by the specific investment climate of 2016 Silicon Valley, in which the combination of hardware innovation, subscription business models, and health and wellness consumer trends attracted capital that may not have been adequately interrogated. Several prominent venture capital firms invested in the company, presumably without establishing that the machine performed a function that a human hand could not.

The company attempted to survive the publicity by reducing the machine's price to $400 and offering refunds to existing customers. Neither gesture addressed the fundamental product problem. Juicero ceased operations in September 2017.

Juicero is included because it is the most efficient illustration of a specific failure mode: the technology solution to a problem that either does not exist or that the technology does not materially improve on the non-technology alternative. The lesson is simple and has been stated in various forms since: before building a complex, expensive technology solution, verify that the problem it solves actually requires the technology.