The Federal Reserve’s monetary policy committee meeting gets underway today. When it unveils its decision on Wednesday, Wall Street expects Bernanke & Co. to cut back slightly on the bond-buying programs collectively known as quantitative easing, which the central bank used to push long term interest rates down over the last few years.

Will the markets freak? They shouldn’t. Or rather, they already have.

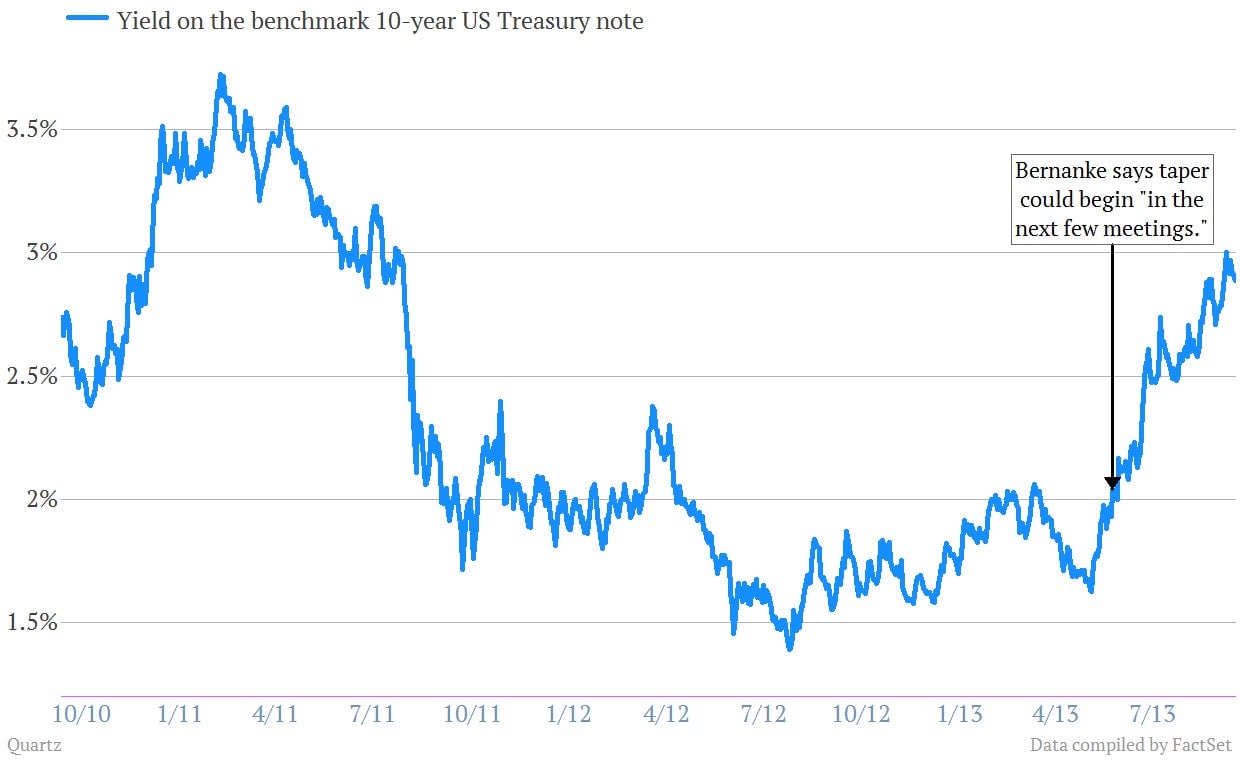

Yields on long-term Treasury bonds have risen sharply since May, when Bernanke first mooted the possibility of cutting back on bond buying. The yield on the benchmark 10-year US Treasury note is currently just under 3.00%; in early May it was yielding less than 1.70%. So as long as reduction in bond purchases comes in between $10 billion and $15 billion a month, the market shouldn’t be startled.

In fact, now that Fed geeks are pretty much over the taper, there’s a new hot topic among the cognoscenti.

As part of the big to-do on Wednesday, members of the FOMC are also going to publish their projections for 2016. They’re likely to show that the Fed expects US unemployment to be between 5% and 6% and inflation around 2%—levels most Fed heads think are about normal for the US economy over the long run, according to the Wall Street Journal’s Jon Hilsenrath.

At the same time, the Fed will also publish projections for where it sees interest rates. JP Morgan expects the Fed’s projection for the key Fed Funds rate to be about 2.25% by the end of 2016, as does most of Wall Street. So that number may well be the key to how the market reacts.

“If the Fed presents a 2016 interest rate forecast that is well above the market’s expectations—and if the market takes any cue from the Fed—this could tighten financial conditions such that the forecasted acceleration in growth fails to materialize,” wrote Michael Feroli, a Fed watcher at JP Morgan.

Translation?: Even if the taper is well understood by the markets, the Fed could still spook the bond market on Wednesday with its interest rate projections. Tread carefully, Ben.