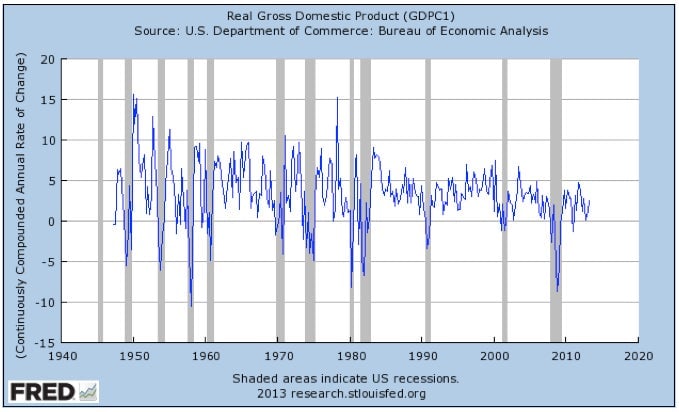

President Obama was right to say his appointment of Janet Yellen to head the US Federal Reserve has been one of his most important economic decisions. As the graph below shows, from the mid-1980s through 2007, monetary policy kept US GDP growth fairly steady, without needing much help from Keynesian fiscal policy. Economists talk about this period when GDP growth was much steadier than before as “The Great Moderation.” Monetary policy has done less well in years since the financial crisis in 2008, because the Fed felt it could not lower its target interest rate below zero, and has not been fully comfortable with its backup tools of quantitative easing and “forward guidance” about what it will do to interest rates years down the road.

President Obama was right to say his appointment of Janet Yellen to head the US Federal Reserve has been one of his most important economic decisions. As the graph below shows, from the mid-1980s through 2007, monetary policy kept US GDP growth fairly steady, without needing much help from Keynesian fiscal policy. Economists talk about this period when GDP growth was much steadier than before as “The Great Moderation.” Monetary policy has done less well in years since the financial crisis in 2008, because the Fed felt it could not lower its target interest rate below zero, and has not been fully comfortable with its backup tools of quantitative easing and “forward guidance” about what it will do to interest rates years down the road.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Yellen’s academic research on the theory of unemployment points to one of the key reasons it is important to keep the growth of the economy steady. Let me explain.

With her husband George Akerlof, who was among recipients of the Nobel Prize in Economics in 2001, Yellen edited “Efficiency Wage Models of the Labor Market,” which gives one of the leading theories of why some level of unemployment persists even in good times, and why unemployment gets much worse in bad times. Yellen summarized the major variants of Efficiency Wage Theory. They all share the idea that firms often want to pay their workers more than their workers can get elsewhere. It might seem that employers would always want to pay workers as little as possible, but badly paid workers don’t care much about keeping their jobs.

Low pay affords workers an attitude of “Take this job and shove it!.” If workers have no reason to obey you because they are just as well off without the job—and owe you nothing—it will be hard to run a business. And if you hire someone at very low pay who actually sticks around, it is reasonable to worry about what is wrong with the worker that makes it so that worker can’t do better than the miserable job you are offering them. The way out of this trap is for an employer to pay enough that the worker is significantly better off with the job than without the job.

It might sound like a good thing that firms have a reason to pay workers more, except that, according to the Efficiency Wage Theory, firms have to keep raising wages until workers are too expensive for all of them to get hired. The reasoning goes like this: There will always be some jobs that are at the bottom of the heap. Suppose some of those bottom-of-the-heap jobs are also dead-end jobs, with no potential for promotion or any other type of advancement. If bottom-of-the-heap, dead-end jobs were free for the taking, no one would ever worry about losing one of those jobs. The Johnny Paycheck moment—when the worker says “Take this job and shove it”—will not be long in coming. If they were free for the taking, bottom-of-the-heap, dead-end jobs would also be subject to high turnover and low levels of emotional attachment to the firm.

The only way a bottom-of-the-heap, dead-end job will ever be worth something to a worker is if there is a something worse than a bottom-of-the-heap, dead-end job. In Efficiency Wage Theory, that something worse is being unemployed. To make workers care about bottom-of-the-heap, dead-end jobs, employers have to keep raising their wages above what other firms are offering until workers are expensive enough that there is substantial unemployment—enough unemployment that being unemployed is worse than having one of those bottom-of-the-heap, dead-end jobs. For the worker, Efficiency Wage Theory is bittersweet.

Some of what counts as unemployment in the official statistics arises from people in between jobs who simply need a little time to identify and decide among all the different jobs potentially available to them. And some is from people who have an unrealistic idea of what kinds of jobs are potentially available to them. But let me call the part of unemployment due to this Efficiency-Wage-Theory logic motivational unemployment. In the case of motivational unemployment, there will be people who are unemployed who are essentially identical to people who do have jobs. It is just bad luck on the part of the unemployed to be allotted the social role of scaring those who do have jobs into doing the boss’s bidding.

In criminal justice, swift, sure punishment does not need to be as harsh as slow, uncertain punishment. Just so, in Efficiency Wage Theory, the better and faster bosses are at catching worker dereliction of duty, the less motivational unemployment is needed. Because it is easier to motivate workers when worker dereliction of duty is detected more quickly, firms will stop raising wages and cutting back on employment at lower levels of unemployment.

There are other conceivable ways to reduce the necessity of motivational unemployment in the long run.

To make possibilities 5 and 6 more concrete, let me mention online activist Morgan Warstler’s thought-provoking (if Dickensian and possibly unworkable) proposal that would make unemployment less attractive and would better track workers reputations: An “eBay job auction and minimum income program for the unemployed.” The program would require those receiving unemployment insurance or other assistance to work in a temp-job—within a certain radius from the worker’s home. The employer would go online to bid on an employee to hire and the wages would offset some of the cost of government assistance. Both the history of bids and an eBay-like rating system of the workers would give later employers a lot of useful information about the worker. Workers would also give feedback on firms, to help ferret out abuses. It is obvious that many of the policies that Efficiency Wage Theory suggests might reduce unemployment would be politically toxic and some (such as using the threat of deportation to keep employees in line) are morally reprehensible. But some of those policies merit serious thought.

What does Efficiency Wage Theory have to say about monetary policy? The details of how motivational unemployment works matter. Think about bottom-of-the-heap, dead-end jobs again. As the unemployment rate goes down in good times, the wage firms need to pay to motivate those workers goes up faster and faster, creating inflationary pressures. But the wages of those jobs at the bottom are already so low that when unemployment goes up in the bad times, it takes a lot of extra unemployment to noticeably reduce the wages that firms feel they need to pay and bring inflation back down. This is one of several, and possibly the biggest reason that the round trip of letting inflation creep up and then having to bring it back down is a bad deal. And a round trip in the other direction—letting inflation fall as it has in the last few years with the idea of bringing it back up later—is just as costly. (You can see the fall in what the Fed calls “core” inflation—the closest thing to being the measure of inflation the Fed targets—in the graph below.) It is much better to keep inflation steady by keeping output and unemployment at their natural levels.

The conventional classification divides monetary policy makers into “hawks,” who hate inflation more than unemployment and “doves” who hate unemployment more than inflation. Most commentators classify Janet Yellen as a dove. But I parse things differently. There can be serious debates about the long-run inflation target. I have taken the minority position that our monetary system should be adapted so that we can safely have a long-run inflation target of zero. But as long as there is a consensus on the Fed’s monetary policy committee that 2% per year (in terms of the particular measure of inflation in the graph above) is the right long-run inflation target, it is entirely appropriate for Janet Yellen to think that inflation below 2% is too low in any case, so that further monetary stimulus is beneficial not only because it lowers unemployment, but also because it raises inflation towards its 2% target level.

To see the logic, imagine some future day in which everyone agreed that the long-run inflation target should be zero. Then if inflation were below the target—in that case actually being deflation–then almost everyone would agree that monetary stimulus would be good not only because it lowered unemployment, but also because it raised inflation from negative values toward zero. Anyone who wants to make the case for a long-run inflation target lower than 2% should make that argument, but otherwise they should not be too quick to call Janet Yellen a dove for insisting that the Fed should keep inflation from falling below the Fed’s agreed-upon long-run inflation target of 2%.

Nor should anyone be called a hawk and have the honor of being thought to truly hate inflation if they are not willing to do what it takes to safely bring inflation down to zero and keep it there. Letting inflation fall willy-nilly because a serious recession has not been snuffed out as soon as it should have been is no substitute for keeping the economy on an even keel and very gradually bringing inflation down to zero, with all due preparation.

There is also no special honor in having a tendency to think that a dangerous inflationary surge is around the corner when events prove otherwise. One feather in Yellen’s cap is the Wall Street Journal’s determination that her predictions for the economy have been more accurate than any of the other 14 Fed policy makers analyzed. For the Fed, making good predictions about where the economy would go without any policy intervention, and what the effects of various policies would be, is more than half the battle. Differences in views about the relative importance of inflation and unemployment pale in comparison to differences in views about how the economy works in influencing policy recommendations. Having a good forecasting record is not enough to show that one understands how the economy works, but over time, having a bad forecasting record certainly indicates some lack of understanding—unless one is learning from one’s mistakes.

In the last 10 years, America’s economic policy-making apparatus as a whole made at least two big mistakes: not requiring banks to put up more of their own shareholders’ money when they took risks, and not putting in place the necessary measures to allow the Fed to fight the Great Recession as it should have, with negative interest rates. It is time for America’s economic policy-making apparatus to learn from its mistakes, on both counts.

As the saying goes, “It’s difficult to make predictions, especially about the future.” But I will hazard the prediction that if the Senate confirms her appointment, monetary historians 40 years from now will say that Janet Yellen was an excellent Fed chief. There will be more tough calls ahead than we can imagine clearly. As president of the San Francisco Fed from 2004 to 2010, and as vice chair of the Fed since then, Yellen has brought to bear on her role as a policymaker both skills in deep abstract thinking from her academic background and the deep practical wisdom also known as “common sense.” It is time for her to move up to the next level.