Westminster is in turmoil. The UK parliament can’t agree on how to leave the EU, and prime minister Theresa May is clinging to her leadership after a no-confidence vote yesterday. Britain’s financiers are following every twist and turn because the manner of Britain’s divorce with the EU will affect their access to clients on the continent.

Westminster is in turmoil. The UK parliament can’t agree on how to leave the EU, and prime minister Theresa May is clinging to her leadership after a no-confidence vote yesterday. Britain’s financiers are following every twist and turn because the manner of Britain’s divorce with the EU will affect their access to clients on the continent.

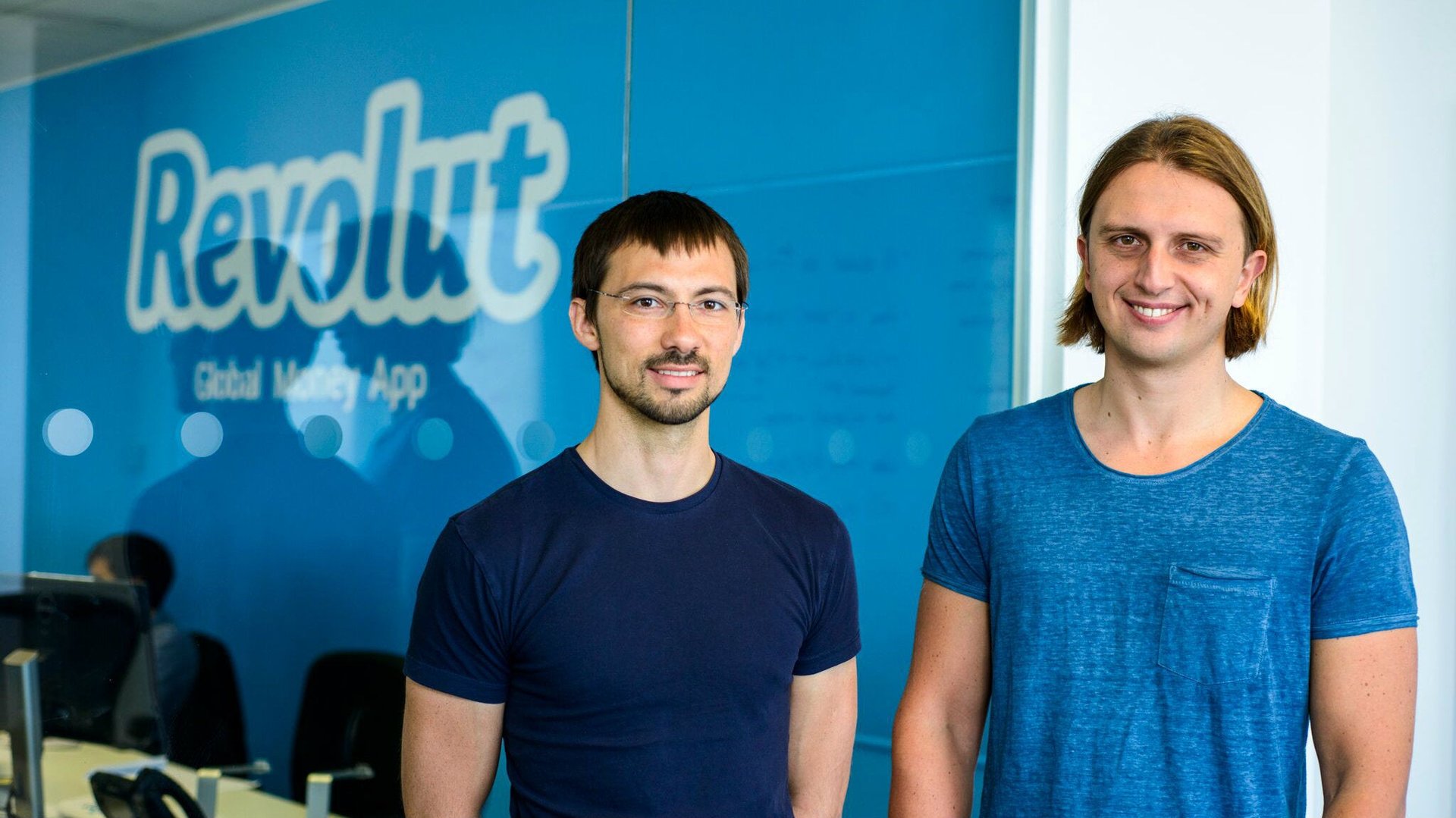

They have reason to worry, as EU politicians have sought to use Brexit to chip away at the British capital’s world-leading role in banking and trading. But one person who’s not sweating it is Nikolay Storonsky, co-founder of one of Britain’s fastest-growing financial technology startups, Revolut. The company, which just secured a European banking license through the Bank of Lithuania, says its goal remains to become the “Amazon $AMZN of banking,” Brexit be damned.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Like a lot of people who work in London’s Canary Wharf financial district, Storonsky isn’t originally from the UK and wouldn’t seem to have any particular reason to be loyal to it. He was born on the outskirts of Moscow before studying physics at the Moscow Institute of Physics and Technology and then working as an equity derivatives trader at Lehman Brothers and Credit Suisse. His long-standing views on Brexit haven’t changed: He says the UK is still one of the best places in the world to set up and run a fintech company.

Storonsky points out that the financial regulator favors startups, and the government is pro-entrepreneurship. But that government is fractured. May won a vote of confidence within by her own party yesterday by 200 to 117 votes; it’s a margin that keeps her leadership intact, but without a strong mandate that helps her negotiate her stalled deal through the full parliament.

Revolut, meanwhile, has thrived in London. The company runs a whizzy payment app tied to a debit card that also provides things like foreign-exchange transfers and insurance for mobile devices. It says it has more than 3 million customers, opens as many as 10,000 accounts each day, and handles transaction volumes of more than $4 billion per month.

Storonsky says that despite Brexit turmoil, investment and access to highly skilled talent haven’t been an issue: The company has raised around $340 million from investors and doesn’t anticipate any trouble hiring new workers.

Likewise, for the 2.3 million workers in the UK’s financial sector, Brexit hasn’t been the catastrophe some feared. A September survey by Reuters of 123 companies showed that as few as 630 UK finance jobs had moved or been replaced by equivalents overseas. (That compares with projections not long ago signaling that hundreds of thousands of jobs could go.) In addition, the British tech industry is still the envy of Europe—it boasts more funding and highly valued startups than its rivals on the continent.

Not every financial executive is nonchalant about Brexit, of course. Kristo Kaarmann, CEO of TransferWise, a London-based money transfer service, has said the breakup could, for example, make engineering talent less interested in living in the UK. There are some signs of this happening—the UK’s advantage versus Germany in attracting software developers has slipped, according to a report by venture capital firm Atomico.

Compounding matters, it’s been more than two years since Brits voted to leave the bloc and it remains to be seen whether the divorce will be messy with no agreement in place (unlikely, but the odds are improving), will resemble the plan the prime minister spent months negotiating with Brussels (nobody seems to like it), or will be canceled entirely (remote, but increasingly conceivable as the gridlock grinds on).

Chances are, Revolut will soon have to operate in a more fragmented, uncertain Europe. In 2019, the company plans to use its European banking license to offer full checking accounts as well as get into lending and commission-free stock trading. Storonsky’s vision is for retail and business customers to apply for loans in the Revolut app and have the money in their account almost instantly. Revolut plans to implement its license in smaller EU countries before using it in the UK, France, Germany, and Poland.

In an emailed comment, the company acknowledged the uncertainty about the future status of its EU bank license in the UK. Revolut says it had always planned to have licenses in both places, and that it already has e-money recognition in both jurisdictions so that its core payments business will go on as usual.

Rivals grumble that getting an EU bank license through Lithuania instead of a better-known regulator smacks of taking a shortcut. The company says the license was approved by the European Central Bank like any other and that Lithuania is an “innovative and fintech friendly” financial hub.

And while it will soon offer accounts that are backed up to €100,000 ($114,000) by the European deposit insurance scheme, a key test is whether customers will trust it with their paycheck deposits, a sign the neobank is gaining the stature that long-lived incumbents now enjoy.

As for Brexit, it may not have been a complete catastrophe for Britain yet, but it certainly hasn’t improved the prospects for financial companies in the UK. Britain’s divorce from the EU isn’t official until March next year, and a lot can happen in the meantime.