Pretty much everyone on Wall Street thought the taper was a done deal back in September.

Pretty much everyone on Wall Street thought the taper was a done deal back in September.

And—ahem—even some observers based in less well-heeled areas of Manhattan.

As it turned out, it wasn’t.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Lucky for us that we didn’t have billions of dollars riding on our thoughts about whether or not the Federal Reserve would begin winding down its bond-buying program. (The most we might lose was some Twitter $TWTR followers.)

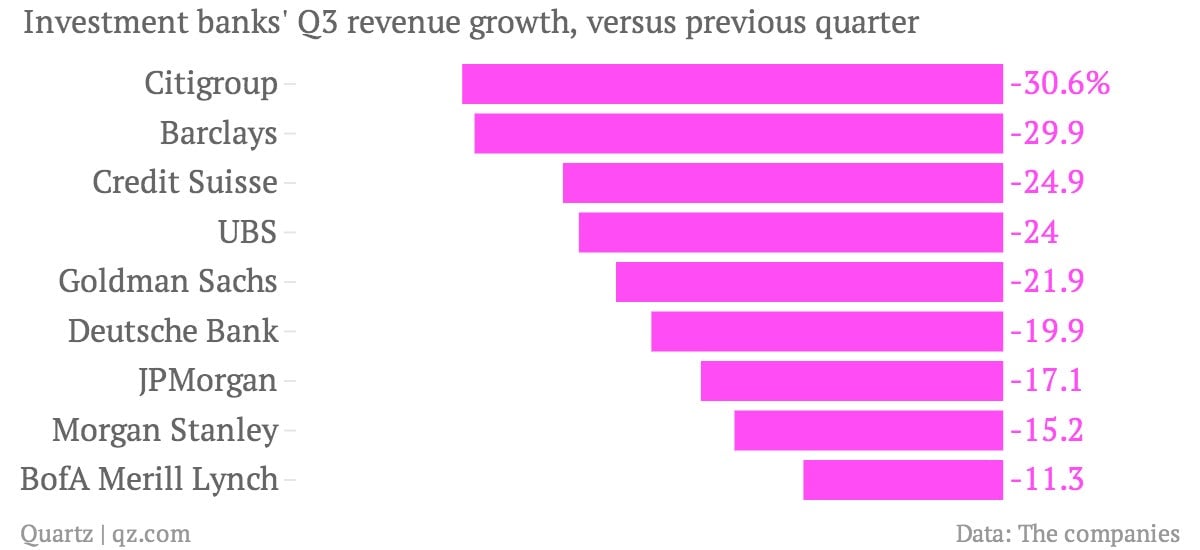

But for bond traders on Wall Street, the repercussions were a lot worse. In fact, the third quarter was one of the ugliest in recent memory for Wall Street.

As you can see, the pain was widely felt. But, as always, Goldman Sachs $GS attracted its fair share of attention. Given its reputation for having some of the smartest people on the street, there was plenty of schadenfreude going around when Goldman’s fixed income, currencies and commodities division—where bond trading is housed—saw revenue tumble more than 44% to $1.25 billion. That was Goldman’s weakest quarter since the financial crisis, according to Reuters, which today published a few more interesting tidbits about Goldman’s tough run in the fall, citing two unnamed sources.

The bank was anticipating that the Federal Reserve would begin winding down its monetary-easing programs, the sources said. When the Fed unexpectedly announced that it would keep its massive bond-buying program in place, Goldman was left with positions that, “absolutely got annihilated,” as one person familiar with the matter put it.

Goldman spokesman Michael DuVally declined to comment.