And we’re back.

Nearly four years after Greece set off the European debt crisis, the Hellenic Republic is being allowed to borrow from global bond markets again, [paywall] with a projected €2 billion ($2.76 billion) debt offering today.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Let’s be clear. This makes no sense.

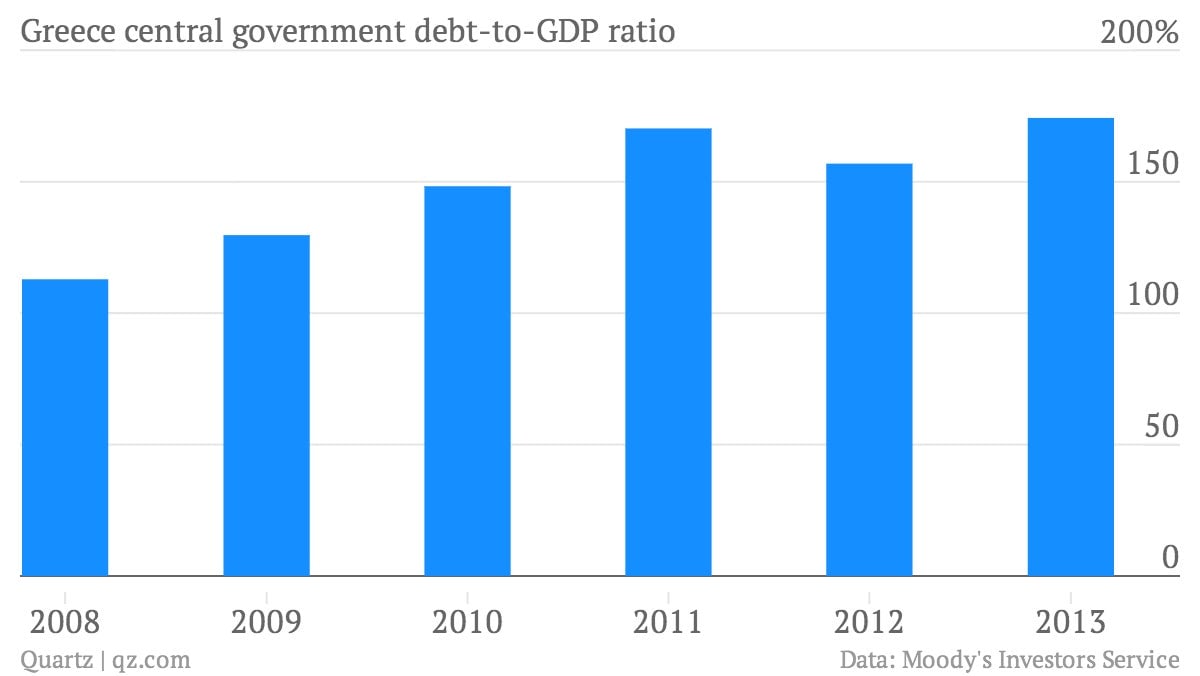

For one thing, Greece’s debt load has gotten much worse over the last few years, not better. Greece’s debt-to-GDP ratio in 2010 was an impossible to manage 148%. Last year it was an even more impossible 174%.

The debt-to-GDP ratio is the gold standard of debt metrics, because it measures liabilities—or debt—as a share of an economy’s productive capacity. In other words, it tells you whether the economy is productive enough to generate the money needed to pay its debts. Without an economy, it’s hard for a country to pay its creditors.

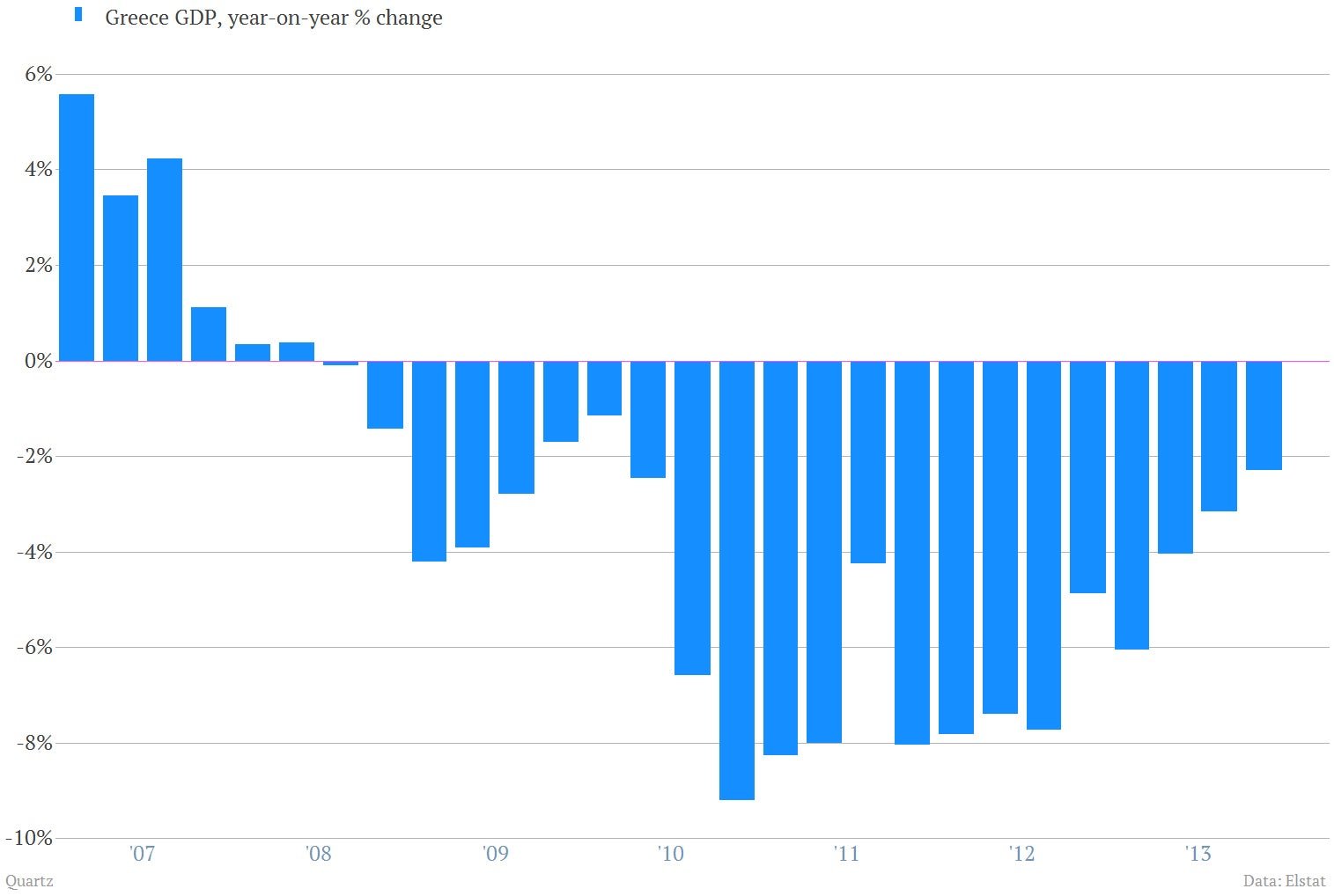

And that’s the heart of the problem for Greece. Over the last few years, the Greek economy has looked like this.

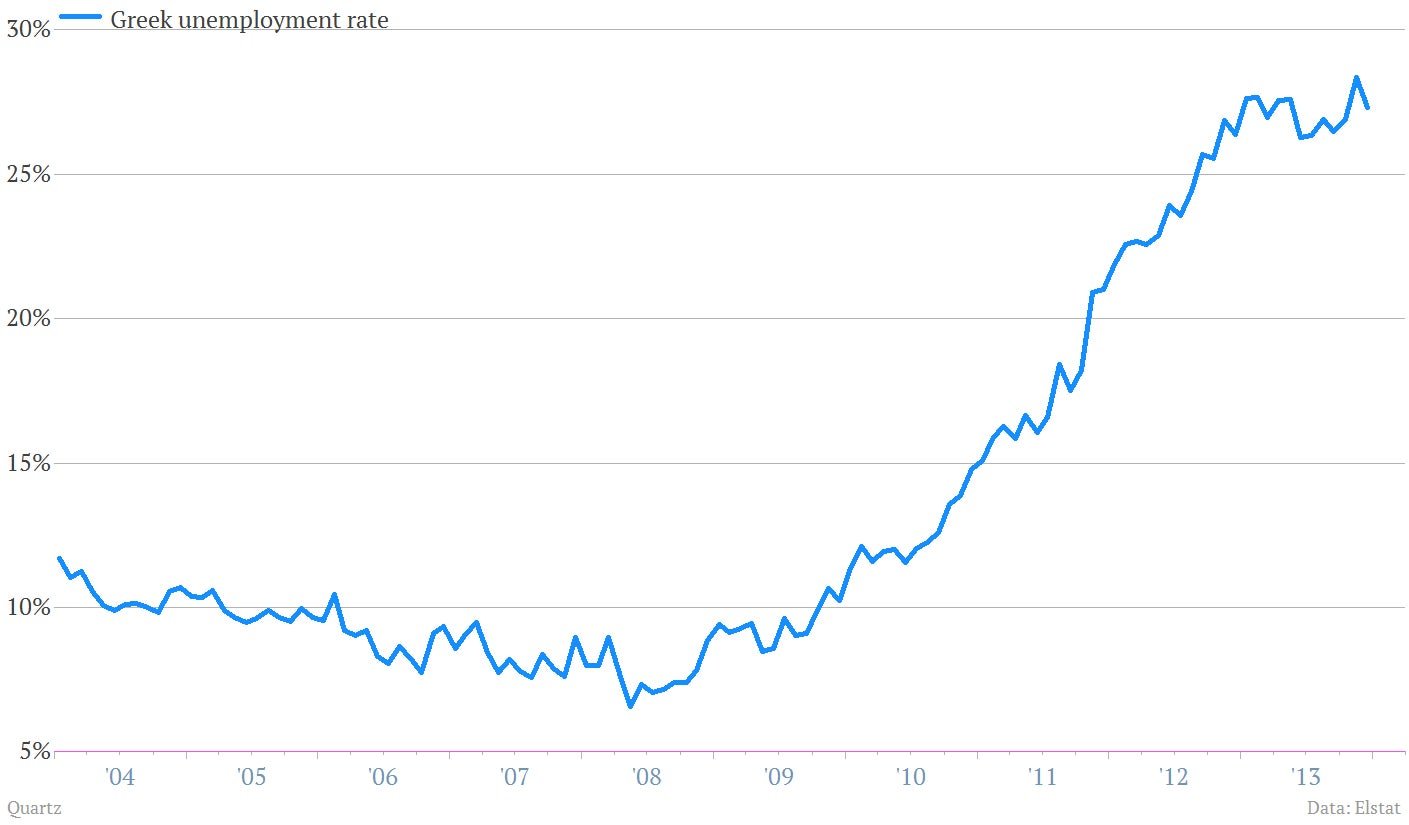

And the Greek labor markets have looked like this.

About 25% of the Greek economy has been destroyed. (To be more precise, it’s 24.8%. During the fourth quarter of 2007 Greece’s GDP was €53.20 billion by the fourth quarter of 2013 it was about €40.01 billion.) Nobody knows if any of it is going to come back any time soon.

But try explaining any of this to the bond market. This year Greek bonds have been some of the hottest investments around, and prices have surged. The Bank of America $BAC Merrill Lynch Greek Government bond index has returned more than 30% in 2014.

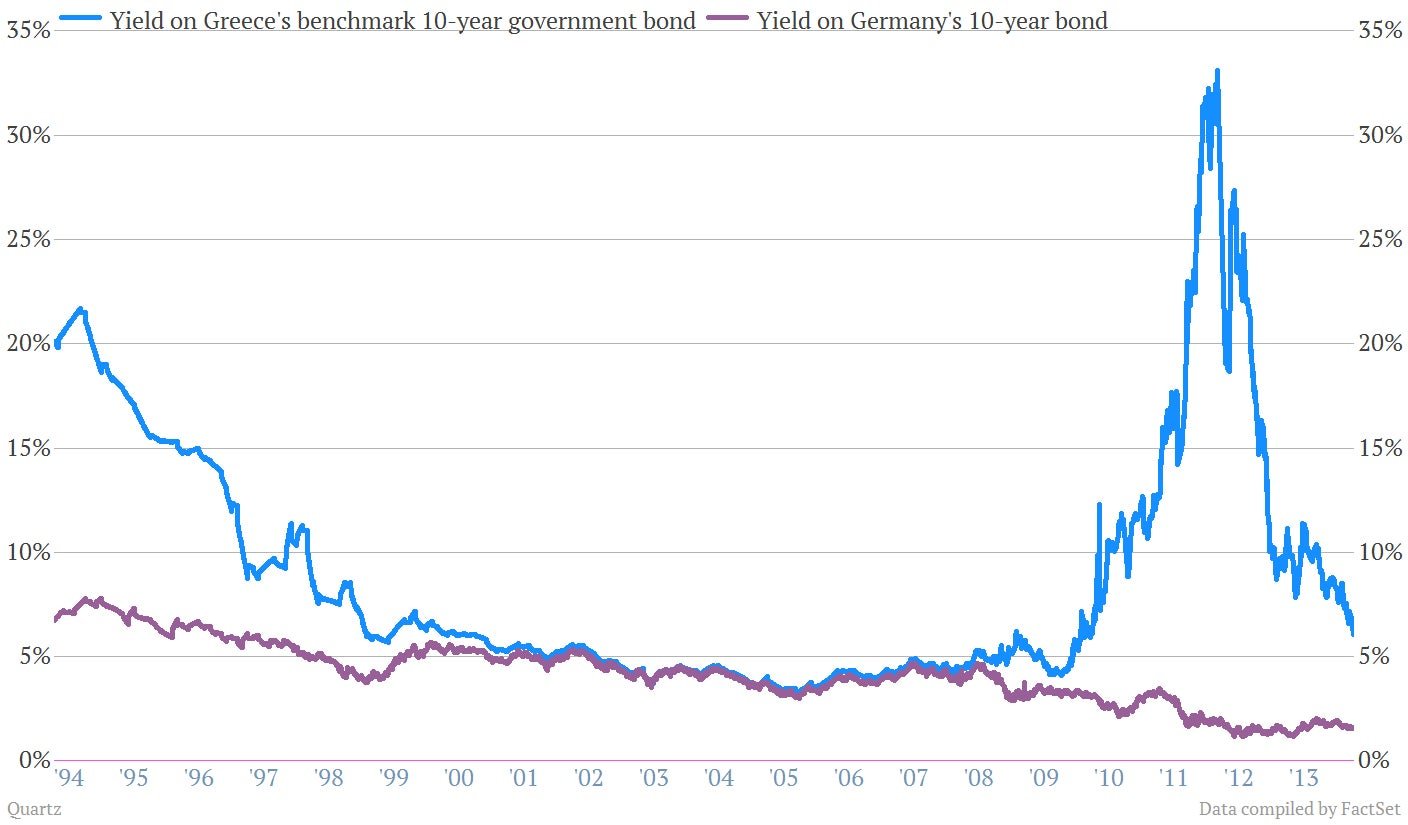

Yields, which move in the opposite direction from prices, have tumbled. In fact, yields on Greek debt are now starting to return to within shouting distance of Germany, which are are seen as the safest form of euro-denominated debt. If the market sees a borrower as riskier, that risk is measured—in part—by how much higher its bond yields are compared to Germany.

With that in mind, this chart tells you a lot. The short version: Greece used to be thought of as risky. The market forgot about the risks when it joined the euro. Then it suddenly remembered them back in 2010.

What’s so dumbfounding about investor willingness to buy Greek government debt is that investors suffered heavy losses just a couple of years ago. Remember all of the hubbub about private sector involvement? Basically investors were forced to “voluntarily” fork over their Greek bonds in exchange for new ones that paid a lot less. The Reserve Bank of Australia estimates that private sector investors suffered losses of 54%—in nominal terms—on the swap.

Of course, that’s ancient history now. (It was 2012.)

But the question remains. Why would investors lend any money to Greece?

As we’ve said before, it’s not because of the country’s dynamic economy. Nor is it because Greece’s debt load has been restructured in a way that makes it possible to manage over the long term. Nor is it because of the country’s track record as a debtor. (Reinhart and Rogoff famously noted that the country has been in default for roughly half of the years since it gained independence from the Ottoman Empire in the 1832.)

No, the answer must be that a consensus is building in the markets, that the European Central Bank now stands behind Greek government debt in a way that it didn’t before. After all, the bonds of all the troubled European nations—Portugal, Ireland, Italy, Greece and Spain—have been enjoying a gobsmacking rally since ECB chief Mario Draghi vowed to do “whatever it takes” to preserve the euro back in July 2012.

Savvy investors know it will be tough for the ECB to disabuse the markets of this notion. Is Draghi going to come out and specify that his “whatever it takes” comments don’t pertain to Greece? He can’t. It would immediately set the markets on a hunt for the next country where “whatever it takes” doesn’t apply.

At the same time, the ECB needs to think long and hard about the kind of conventions that are getting baked into the bond market right now. Financial markets run on conventional wisdom. When Greece won entry to the euro zone in 2000, its bond yields inexplicably converged with those of Germany. Nobody said anything, and as a result, the markets began to view all euro-denominated bonds as essentially interchangeable.

It only took 10 years for the bond market to realize the Greece and Germany are very different countries. It’s taking even less time for the market to forget that hard-won lesson, all over again.