This is the full transcript for episode 2 of season 3 of the Quartz Obsession podcast, National debt: Acceptable imbalance.

Kira Bindrim: You could be forgiven for thinking that hanging onto debt, any debt, is a bad thing. When people go into debt, like many do to attend college, make major purchases, or put a down payment on a home, they’re often aiming to pay it off as quickly as possible. After all, no investment is worth drowning in interest payments.

But those same rules don’t apply at the national level. Yes, for as long as countries have been around, their governments have spent money to get ahead, the same way you or I might invest in our education. And in many places, including the US, that means decades of adding to the national debt. But federal governments don’t need to balance their budgets the way you and I do. In fact, doing so can hold them back.

National debt isn’t a mark for or against a country—it’s a litmus test for that country’s resources, influence, values, and economic philosophy. And that’s what makes debt so interesting now: After two years of pandemic, how a country invests in itself explains something about how it sees the future.

This is the Quartz Obsession, a podcast that explores the fascinating backstories behind everyday ideas, and what they tell us about the global economy. I’m your host, Kira Bindrim. Today: debt, the price tag on progress.

I’m joined now by Nate DiCamillo, who is an economics reporter with Quartz. And before we really get into sort of the history of debt and the implications of national debt, I kind of want to start with my personal experience and gut check it with you, Nate. Which is, when I was growing up, I was very much taught that debt was something to avoid. I didn’t get a credit card until my 20s, I made a lot of decisions about college based on my ability to pay off my loans or even go into debt. The idea from my parents was really that you don’t do this unless you must. And I’m curious, one, if that is your experience, and, two, if you think that mentality kind of infects how we think about debt overall?

Nate DiCamillo: Absolutely. When I was young, the main goal of getting me through school was that I would get through school without any debt. The idea that kind of looking down debt is something that exists in all the major religions, where debt is seen as this burden, as something that you shouldn’t pass down to your children. And it’s something that has leaked into our national conversation about debt. We talk about the national debt as if it were like household debt. And we talk about it in terms of needing to balance it, needing to have fiscal responsibility, and using what economists call this household fallacy, this idea that it needs to be balanced, like a household budget.

Kira Bindrim: I want to start with some basics. And for the purposes of this question, but really, for the purposes of this episode, let’s assume that I am about a freshman-econ comprehension level, like I took a 101 class, but it was at 8am, and I fell asleep for a good number of them. So let’s go through our 101 questions in almost like a lightning round format.

Nate DiCamillo: Okay.

Kira Bindrim: Question one: When we talk about consumer debt, like I might have from student loans or from credit cards, and we talk about national debt like a country has, how are they different?

Nate DiCamillo: The difference is in how long each entity lives. You and I have a limited lifespan, and we can only refinance our debt so many times. National government is essentially eternal. They can keep refinancing as much as they like.

Kira Bindrim: Next question. Why do we need national debt, or a better way to ask this would be, what are countries spending money on going into debt for?

Nate DiCamillo: To go to war, to recover from a pandemic, recover from hurricane or natural disasters, to provide services for their people.

Kira Bindrim: So any big outlay of capitals, probably?

Nate DiCamillo: Yeah.

Kira Bindrim: Okay. Next question. Who do countries go into debt to?

Nate DiCamillo: Other countries, their own government, and their own people.

Kira Bindrim: Okay, so far, so good. I feel like I’m getting it. It’s like I didn’t even sleep through that class. How do countries pay off their debts?

Nate DiCamillo: Generally, with tax revenue. The Federal Reserve can lower interest rates as low as they can go so that people spend more so you get more tax revenue. You could take down like the debts themselves, the liabilities. So you could like cut spending, try to rein in everywhere that you’re spending. Or you could try to increase your assets, so you’re raising taxes on the rich or corporations, or raising taxes across the board. They can also do it in other ways, wonky ways.

Kira Bindrim: Okay. So there are things that countries can do to manage their debt by virtue of being countries. And there are things that countries can do to manage their debt by virtue of how long they exist, because they’re countries. I feel like you’ve just answered the first half, but what levers do they have available to them to manage their debt over a course of time or hundreds of years?

Nate DiCamillo: Sure. That is something where they can issue new bonds when they want to restructure their debts.

Kira Bindrim: When did we learn about bonds, high school? Explain a bond to me.

Nate DiCamillo: Bonds are essentially loans that the government issues for itself that other people can invest in.

Kira Bindrim: Okay, I feel like I’m following so far, let’s keep wonking out and let’s see how we do.

Nate DiCamillo: In some extreme cases, if we ever got to it, the Federal Reserve could buy bonds directly from Treasury. This is something that you might have heard of, under a term called quantitative easing, where the Federal Reserve buys bonds from the private market, which is essentially money creation.

Kira Bindrim: So when we talk about national debt, what I’m hearing is there’s a little bit of a difference based on what country you are.

Nate DiCamillo: Yeah.

Kira Bindrim: So when we talk about a country controlling its monetary policy, I’m doing a little air quotes here, what does that mean?

Nate DiCamillo: When it comes to like a country controlling its own monetary policy, it’s essentially like when a country is able to control the interest rates on whatever currency it’s using. So, the United States, the Federal Reserve sets those interest rates on the US dollar, essentially. And if I’m a country like El Salvador, I can’t raise the interest rates on the US dollar; even though I’m transacting in dollars, my central bank doesn’t have any authority there. So having control of your own currency, having your own monetary policy, means that you’re allowed to print your way out of crisis.

Kira Bindrim: So maybe you can help me understand this by giving me a few examples of countries that are emblematic of different ends of that spectrum, one with a high level of control, and then one that is an example of where a country might be controlled by its debt because it doesn’t actually have as many levers.

Nate DiCamillo: The one with probably the most control of various currencies is the United States. Because the United States is a world reserve currency and it’s able to set its own monetary policy, it has a lot of leeway in terms of how much debt it can issue. On the opposite end of that, it was Greece. During its debt crisis, it owed the majority of its debt in euros. So when it tried to issue bonds in drachma, its national currency, it couldn’t pay off those debts.

Kira Bindrim: So the value of your country’s currency is going to impact your ability to pay off debts that are in another currency, and then that in and of itself is going to control what you can do, what you’re willing to do, with your national debt.

Nate DiCamillo: Absolutely.

Kira Bindrim: How do we measure debt? Is it just the big number of money that’s owed?

Nate DiCamillo: So that, that is what people generally think. So the headlines that flash when the big number, the whole number crosses some sort of threshold—that number is not super useful because it doesn’t fully capture how well a country could pay off its liabilities in a given moment. The other stat that economists look at is debt-to-GDP ratio. So that’s essentially like the percentage of your GDP that your debt makes up. But in terms of our year-to-year, like being able to run countries and manage them, most important statistic is in debt servicing, especially with the the cost of interest on your debt and the principal of your debt that’s owed that year. So whatever bonds have matured that year and the interest on those bonds.

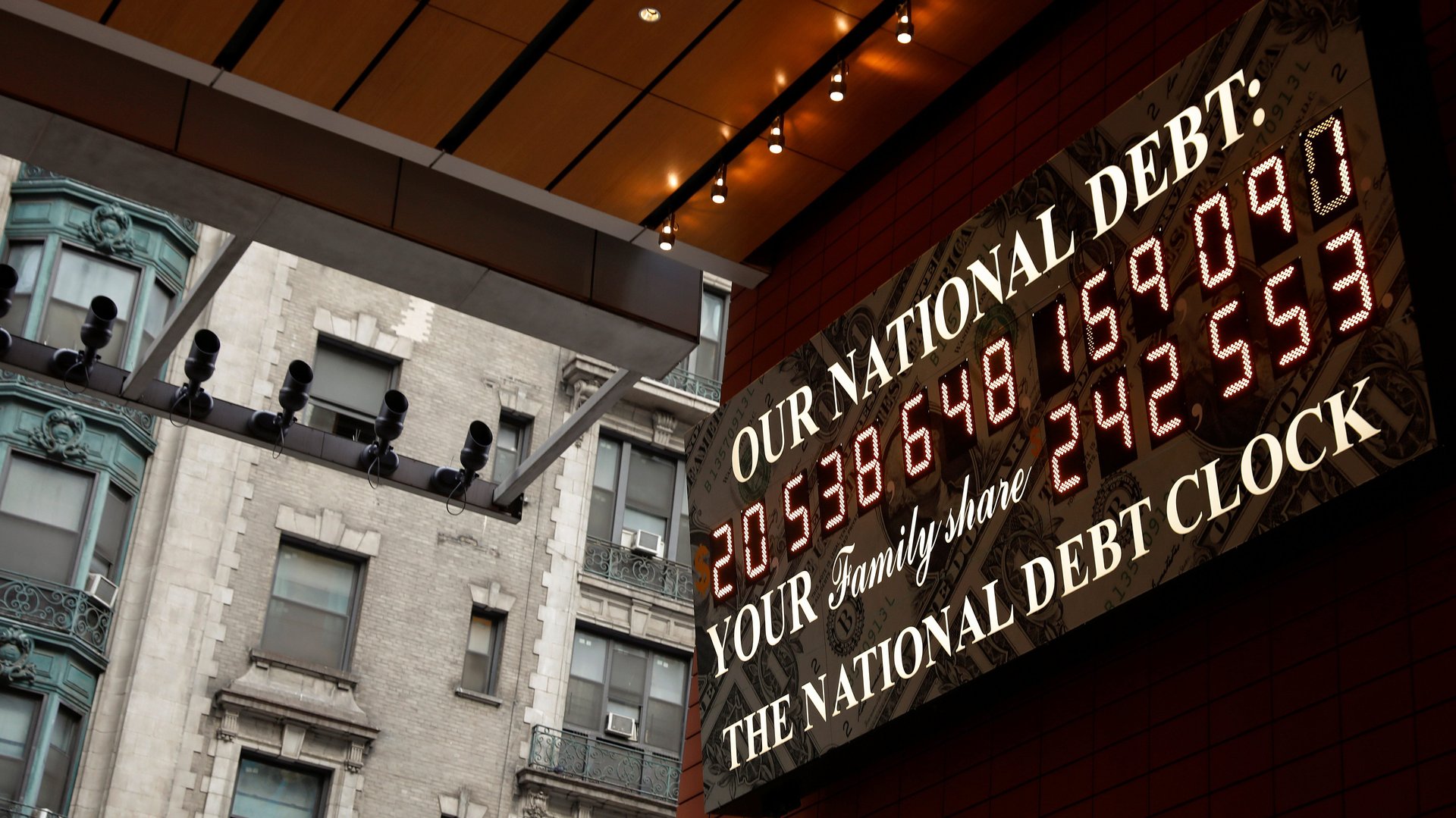

Kira Bindrim: So if I am $1 million in debt personally, that’s gonna look bad on paper, I probably shouldn’t be $1 million in debt. But, surprise, I make $2 million a year. Now my debt-to-GDP ratio—debt-to-salary ratio, let’s say—is different, and that changes things. And of that $1 million, I actually owe $250,000 of it each year for the next four years, that’s going to be very different than if I owe $10,000 every year for the next bajillion years. So all of that nuance gets a little bit lost when you’re just looking at the $30 trillion if you’re talking about the US national debt, but is actually really relevant to whether a country can sustain its debt levels.

Nate DiCamillo: Right, I completely agree with you Kira, that like when people show up with signs that say, ‘This is the whole number of the national debt and whatnot, and this is how much your family owes,’ it’s completely disingenuous. That is not how much your family owes. The debt is spread out over a certain period of time. And what those families owe is the part of debt servicing that makes up our national budget.

Kira Bindrim: The only circumstance in which that would be fair, right, is if every person or entity that we owe money to right now called in that debt for right now, then, yes, every family would have to pay $700 or whatever that number is?

Nate DiCamillo: Yeah, essentially, everyone at once in the world would have to lose faith in your government and the trustworthiness of your government.

Kira Bindrim: To help me understand a little bit better how different countries deal with their national debts, maybe you could give me a couple of examples that are emblematic of different positions from a national debt standpoint.

Nate DiCamillo: So let’s start with Liechtenstein, which has zero debt, because they don’t run an army. They have incredibly low business taxes. There are more companies in Liechtenstein than there are people in Liechtenstein. The majority of their labor force comes from Austria and Switzerland and Germany; people commute in and then they leave, Liechtenstein doesn’t have to pay their social services. Because of Liechtenstein’s ability to profit off of a lot of these workers of these companies from other places, they’re able to bring in a lot more tax revenue than they spend. They don’t have a lot of expenditures.

The opposite of Liechtenstein, in that regard is probably the US in that we have to find a massive military. And we have to manage taxes as a world leader.

Another couple examples of how debt affects different countries is like Japan. Japan has an aging population that needs bonds to use as an investment vehicle. They need a lot of retirement savings, because of their population, they need a lot of bonds. And their currency is primarily in yen.

The complete opposite of them is Greece. During their debt crisis, the majority of their debts were in euros, and when they tried to issue drachma bonds, they couldn’t pay off those debts because the debts were in euros.

Kira Bindrim: So there’s like the no-overhead approach—that would be Liechtenstein, just have no overhead. There’s sort of the ‘have a lot of overhead, but have a lot of revenue’ approach, so try and balance those things. And then there’s the control element—have whatever level of overhead you need, but have enough control over your debt and your currency that you can deal with it.

Nate DiCamillo: Yeah, exactly.

Kira Bindrim: One of the questions this is making me think is: Are there long term downsides to running a balanced budget? Which is sort of counterintuitive. And it sounds like, yeah, there definitely can be.

Nate DiCamillo: Yeah. You can cause the social services to run out. You can cause your country to run behind in terms of new technologies for your people. Your infrastructure can run down. There are all sorts of bad things that can come out of austerity.

Kira Bindrim: Let’s flip. So we just talked about the long-term downsides of a balanced budget, or potential downsides of a balanced budget. What are the long-term downsides of holding high levels of debt for a long period of time? And let’s assume here that we are not talking about countries that are sort of beholden to currency considerations, but we’re talking about the US are countries that theoretically, you know, have as much power as one can have in this situation. Is there a downside to keeping a really high level of national debt for a long period?

Nate DiCamillo: I think the main downside is what happens, again, to your debt servicing costs, if they become too large part of your budget. If you’re a smaller country and your debt is primarily because another wealthier country loaned something, then that wealthy country, which many of the developed economies have done this to developing economies, can lord that over you. So that’s a dangerous game. But if you’re like the richest nation in the world like the US, it’s just the debt servicing costs you keep an eye on.

Kira Bindrim: So it goes back to that sort of, I owe $1 million, I make $2 million analogy—you need to be thinking about your revenues, you need to think about your control over your debt servicing, how onerous it’s going to be, your control over your currency—all of that would inform a country’s decision about what it’s willing to go into debt for, but probably more importantly, how much debt?

Nate DiCamillo: Exactly. And I think one of the major misconceptions of today’s age and how we look at debt is what we consider to be revenue. People have such a narrow view of what revenue is—[that] it’s just taxes, when revenue is, in fact, what comes out of the long-term investments that we make.

Kira Bindrim: After the break, debt gets political.

[ad break]

Kira Bindrim: I feel like we’ve laid a good groundwork for the nuance that goes into the national debt conversation. And what’s so interesting is, especially in the US, but I have to imagine elsewhere, the actual national debt conversation does not have a lot of nuance. It is sort of, ‘A high national debt is bad, period.’ And depending on, you know, which side of the political aisle is arguing the other, either can kind of take up that mantle. So I want to talk about that conversation. What are the different schools of thought—I don’t mean political but more economic thought—on national debt?

Nate DiCamillo: So generally, I think of this, in terms of mainstream economics, there’s like two schools of thought that pervade our society. One is new Keynesianism, which is very much focused on spending during times of recession, when interest rates are low, and there’s lots of access to cheap capital. So John Maynard Keynes was a big figure in economics. Economists who really helped us understand that economies might not be so much constrained by the number of dollars in the economy, but by the resources that it has, just the real resources that it has to produce things. And on the flip side of that, there are the like post-Keynes, or like some heterodox schools of thought like modern monetary theory, where there is a feeling that you can spend anytime, whether you’re in a recession or whether you’re in rapid growth. And that you should try to employ certain governmental kind of accounting maneuvers, like the Federal Reserve buying bonds directly from Treasury, in order to manage inflation.

Kira Bindrim: So one school of thought is kind of opportunistic. Like, when there are moments that everything gets cheaper, that’s the time to really invest because you get the benefit of investing and also everything’s cheap. And the other school of thought is, you have a lot of tools at your disposal as a country to manage your own debt, so you might as well just go hard and embrace it.

Nate DiCamillo: Yeah, like, let’s go and have the government play a larger role in the market and in our lives in terms of deciding how the economy looks.

Kira Bindrim: So it doesn’t sound like the economic disagreement between those two schools of thought is about which things are worth going into debt over, given their likelihood to contribute to GDP, versus what debt level is appropriate considering the state of the economy and a country’s autonomy in terms of its monetary policy? Is that right?

Nate DiCamillo: Yeah, it has to do with like, what are the economic conditions that we’re seeing right now?

Kira Bindrim: And is that debate about which things are worth going into debt over, it seems like that’s where politics comes in?

Nate DiCamillo: Definitely. So then you begin to start to ask what is our deficit spending? What is it geared towards? And what does that actually produce for us? So, wars in other countries doesn’t produce a lot for us, generally. Investments in healthcare, and education, and social services here at home, generally have a really, really high yield.

Kira Bindrim: Given the many decades of history we have to look at that, like, what did we invest in, what did we go into debt for and what did it produce for us in terms of GDP, why is it still so political? Or I guess, when did the conversation about national debt, and maybe this is mainly a US thing, become so politicized?

Nate DiCamillo: I think that, in a sense, debt has always been political. In some ways, the ability to issue debt does kind of signify that you’re a sovereign nation state with its own agency. I think that in terms of our current state of how do we feel about debt now, I think that there’s been a lot of propaganda that tells people that when we enter into economic hard times, that it’s because of this or that boogeyman. And debt operates in the same way in terms of, it’s one of these things that politicians like to drag out when they see the government doing things that they don’t want it to do.

Kira Bindrim: Is the debate about national debt the loudest in countries that have the most of it, or the the largest national debts?

Nate DiCamillo: I mean, to my knowledge, no one’s yelling about debt in Japan, or in South Korea. Whether or not you have a really high level of debt doesn’t really dictate how people talk about debt. Really, what dictates the way people talk about debt is whether or not times are good—can I get a job? Am I getting a raise? What’s the price of gas? Those types of things.

Kira Bindrim: To that end, I’m curious, because in the US, it is discussed a lot and it is sort of this political cudgel on either side. But do average people care a lot about national debt?

Nate DiCamillo: I know that the concern about debt among Americans is dropping, but it’s definitely still there. Like, for instance, in 2020, the share of Americans who were concerned about the federal budget deficit, which is basically when we’re spending more than we’re taking in, dropped below 50% for the first time. And that is kind of representative of people realizing, especially in times of crisis, it’s really necessary to spend more than you’re taking in in order to kickstart economic activity.

Kira Bindrim: But to your point, I guess it sounds like, as an abstract concept, a lot of people do not on the daily think about the national debt as something they need to worry about—as they shouldn’t, because it is not the same as, you know, your credit card bill or whatever. But when the economy is struggling in a macro sense, and especially when people start to feel it in their lives or think they’re going to, the national debt then becomes this bigger symbol, either of, ‘Now is the time to spend money because I’m feeling it in my wallet,’ but almost a little bit at the same time, ‘Now is the time not to spend money because the economy’s in trouble.’ And that tension is part of what gets fed into the politics.

Nate DiCamillo: Totally. The only person that I think thinks about the national debt every day is West Virginia senator Joe Manchin, because he has an aide text it to him.

Kira Bindrim: That’s sad.

Nate DiCamillo: It is sad.

Kira Bindrim: Joe, get like a haiku or like a motivational saying texted to you. National debt, that’s not it. And it’s also a good example of thinking about something in this really micro way that is not micro, like even if you have very strong opinions on the national debt, the day-to-day fluctuations cannot be that important.

Nate DiCamillo: No, if anything, just text me the cost of debt servicing or something.

Kira Bindrim: Right, yeah. We’ll text you.

Nate DiCamillo: Okay, thank you.

Kira Bindrim: Okay, so to that end, we have been talking in the abstract a fair bit, and I kind of want to come back to the present and where debt intersects with some of the stuff that’s happening now, or has happened in the last few years, because we’re talking about when people tend to stress out is when things are uncertain. How has the pandemic affected national debts, both in overall amount, which I have to assume is going up, because countries are investing in preventing collapse, and in what countries are going into debt to do—in other words, the things that you might invest in, in the middle of a pandemic, when the economy is shut down, are quite different than things you might invest in otherwise.

Nate DiCamillo: So the important context for this is, we’d already been on a surge of borrowing before the pandemic. In the past two decades, several countries, the US, UK, Italy, Spain had seen their debt-to-GDP ratios go over 100%. For global debt in 2020, that rose as a percentage of GDP, so the the debt-to-GDP ratio increased by 30 percentage points to 263% of GDP for the entire world. In some cases, like the US sent direct checks to households, whereas the EU, they paid businesses to put workers on furlough. And then there was the emergency spending, in terms of vaccine distribution, testing, that sort of thing.

Kira Bindrim: Is that an example where the things that we are going into debt to do are actually not necessarily going to be directly correlated to an increase in GDP or revenue, versus just a not utter fall off in those things?

Nate DiCamillo: Basically, it’s keeping us from cratering even further. And it also keeps us from, especially in those cases, losing more people. And, you know, when we talk about the economy, especially in the pandemic, the best economic policy, was to try to get rid of covid as quickly as possible, and to slow the spread of covid. Just because, when lots of people die, that is a lot less people being able to start businesses, have families, be happy, spend.

Kira Bindrim: Yeah. A pandemic is a good reason to go into more debt, but not an ideal reason in terms of the normal things that you’d do. I’m interested in this framework we’re circling around, which is that you should go into national debt for things that are likely to boost GDP, which makes sense. From that perspective, to your mind, is there anything that is being underinvested in by countries?

Nate DiCamillo: There are a ton of things that the US underinvests in. Also the EU, but not to the same extent. In terms of just like, thinking about just this past year during the pandemic like you’d mentioned, the US passed bills to help ease the pain of the pandemic and tried to help save lives. But like when it came to the more transformational stuff that president Joe Biden wanted to then go and increase our spending on, critical pieces of technology like semiconductors, or biotechnology, or artificial intelligence, like we’ve slowed on passing those bills. We’ve slowed on passing a bill to go and address the ever-accelerating climate crisis. We’ve also failed to expand like healthcare services in United States. So there’s a whole host of things that really hit home during this pandemic, and the fact that we come out of it without any change in our healthcare system is kind of pathetic.

Kira Bindrim: It reminds me of the comparison we were making at the beginning, which it almost sounds like countries fall into the trap of thinking like individuals, which is ‘I’m using my national debt to deal with immediate crises, to sort of finance things that I need to in the short term, and I am not thinking that I am a country that will exist for hundreds of years and my investments or the things that I’m going into debt for should reflect that vision and that trajectory.’ So let’s take that same framework—national debt is valuable when it’s something that will likely boost GDP over time. Are there any debt fears that you think are actually quite valid?

Nate DiCamillo: With as low as interest rates are right now? No.

Kira Bindrim: Easy, okay. So, there’s a lot of wonk in everything that we’ve just talked about, which is fine, and I’ve learned so much. But if you had to give people one thing to come away from this episode with to understand about national debt, what would it be?

Nate DiCamillo: To no longer think about it like you think about your credit card debt. To no longer like attach it to this idea of it needing to be balanced in some sort of way in which everything cancels out. And to see it as a powerful tool that the state can use to help people.

Kira Bindrim: Okay, let’s end on a fun note. I have one more question for you. And it is a series of words I have never said in this exact order: What is your favorite fun fact about debt? As you got into this subject, what is something that you find that you can’t stop thinking about?

Nate DiCamillo: Probably the trillion-dollar coin. Essentially, the US Mint does have the constitutional authority to mint a trillion-dollar coin to wipe out debt.

Kira Bindrim: It feels like a Nicolas Cage National Treasure-type movie, that he would have to like find the coin or someone would steal the coin. Would it be very large? Would it be like the world’s largest chocolate chip cookie? It should be. Thank you, Nate. This was super wonky and fascinating.

Nate DiCamillo: Thank you, Kira.

Kira Bindrim: That’s our Obsession for the week. This episode was produced by Katie Jane Fernelius. Our sound engineer is George Drake and our executive producer is Alex Ossola. The theme music is by Taka Yasuzawa and Alex Suguira. Special thanks to Nate DiCamillo in New York.

If you liked what you heard, please leave a review on Apple Podcasts or wherever you’re listening. Tell your friends about us! Call in your debts and get them listening. Then head to qz.com/obsession to sign up for Quartz’s Weekly Obsession email and browse hundreds of interesting backstories.