America’s consumer spending—which is about about 70% of all economic activity in the US—is once again being driven by a subprime lending boom.

America’s consumer spending—which is about about 70% of all economic activity in the US—is once again being driven by a subprime lending boom.

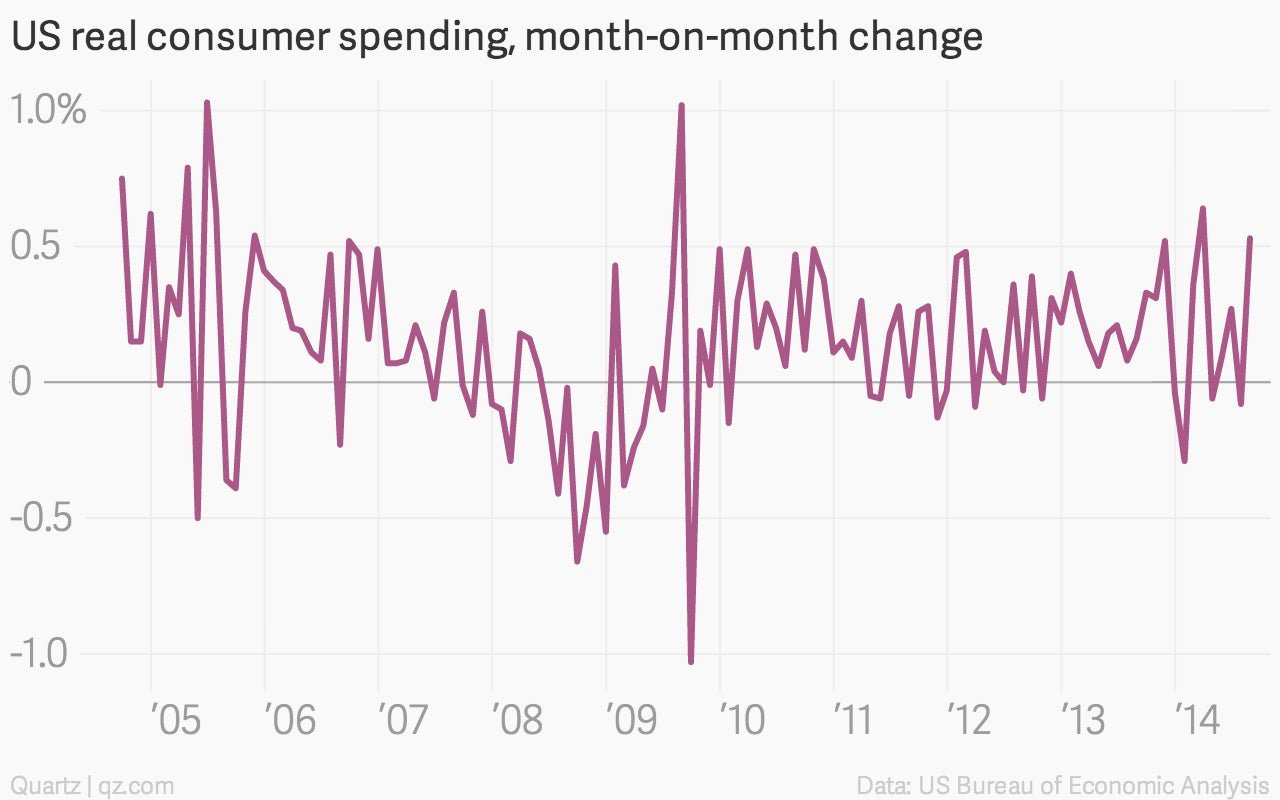

Just look at today’s personal spending data. Month-over-month spending rose 0.5% in August, driven by a 1.9% bump in spending on durable goods. Spending on such goods—big ticket items designed to last more than three years—rose the most in five months, and the US Bureau of Economic Analysis said in a statement that about half the gain was driven by a jump in motor vehicle and parts sales.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

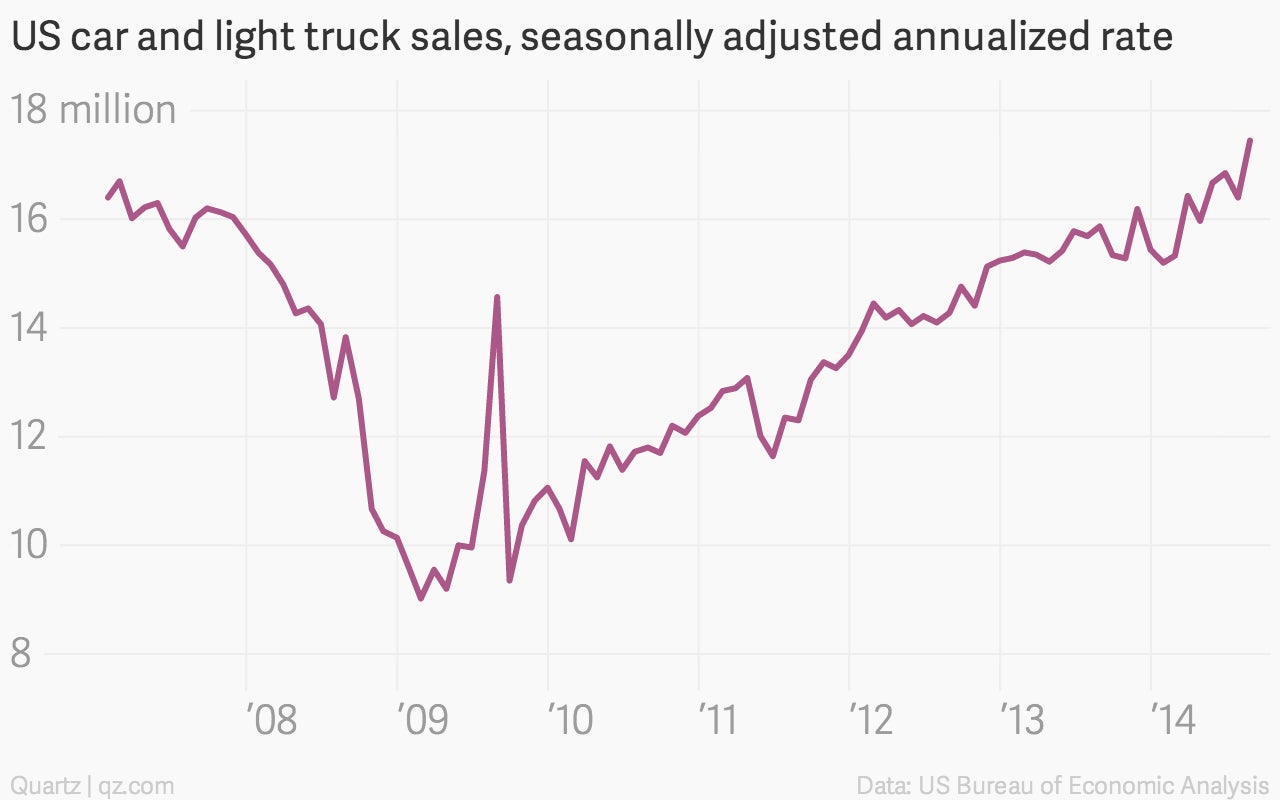

It’s true. Motor vehicles sales have been on a tear lately. In August they were on pace to notch 17.5 million sales in 2014.

Given the outsized impact of vehicle sales on the US consumer economy, this is really helpful to economic growth. But in the wake of the financial crisis, it’s always important to get a sense of what’s enabling consumer purchases. In the market for vehicles, car purchases are being driven increasingly by loans to the less-than-credit-worthy. Yes, subprime is back.

How do we know? By looking at the the credit markets where auto loans are packaged up and sold as securities to investors. Asset-backed securities (ABS) were a key source of instability during the financial crisis. In recent years, one of the fastest-growing sectors of the ABS market has been the market for subprime auto loans. “Subprime auto ABS was one of the few auto sectors to have grown in 2013, and issuance continues to be strong thus far in 2014,” wrote Barclays analysts in a recent note, adding that ABS comprised of packages of subprime loans are now at historic highs as a percentage of the US auto ABS market.

If you think investors would be wary of investing in subprime bonds after the crisis, you’d you be wrong. For one thing, investors have learned that Americans rely on their cars so heavily to get to and from work that they’re often willing to prioritize car payments over other bills. And when they do default on loans, it’s much easier to repossess a car than it is to evict a family from a house. (Also, because used car prices have been so high lately the losses—known as ‘severities’ in the ABS world—have been relatively low.)

That doesn’t mean the market is without problems. For example, the US Department of Justice has confirmed it is looking into lending and securitization practices at two large subprime car lenders, GM Financial and Santander Consumer USA, in the wake of a scorching story in the New York Times that detailed unsavory lending practices in the market.

Even so, the auto market has been one of the few bright spots in recent years for a weaker American economy, which puts the politicians in charge of regulation in a tough spot. There are indications that lenders might start to tamp down some on the extension of subprime loans, which would dampen auto sales and weigh on the economy.

That’s because US consumer incomes are not growing nearly fast enough to supply the kind of growth that the consumption-driven economy requires. In recent decades, the political answer to that problem (which never ends well) has been to open the lending floodgates and let consumers binge on debt. The fate of the auto market should provide an instructive example about whether policy makers are willing to go down that road again.