The news just became worse for Iran, Russia and Venezuela, and better for motorists around the world: Another big Wall Street voice has weighed in with a forecast of long-term lower oil prices—below what these three nations require to balance their budgets.

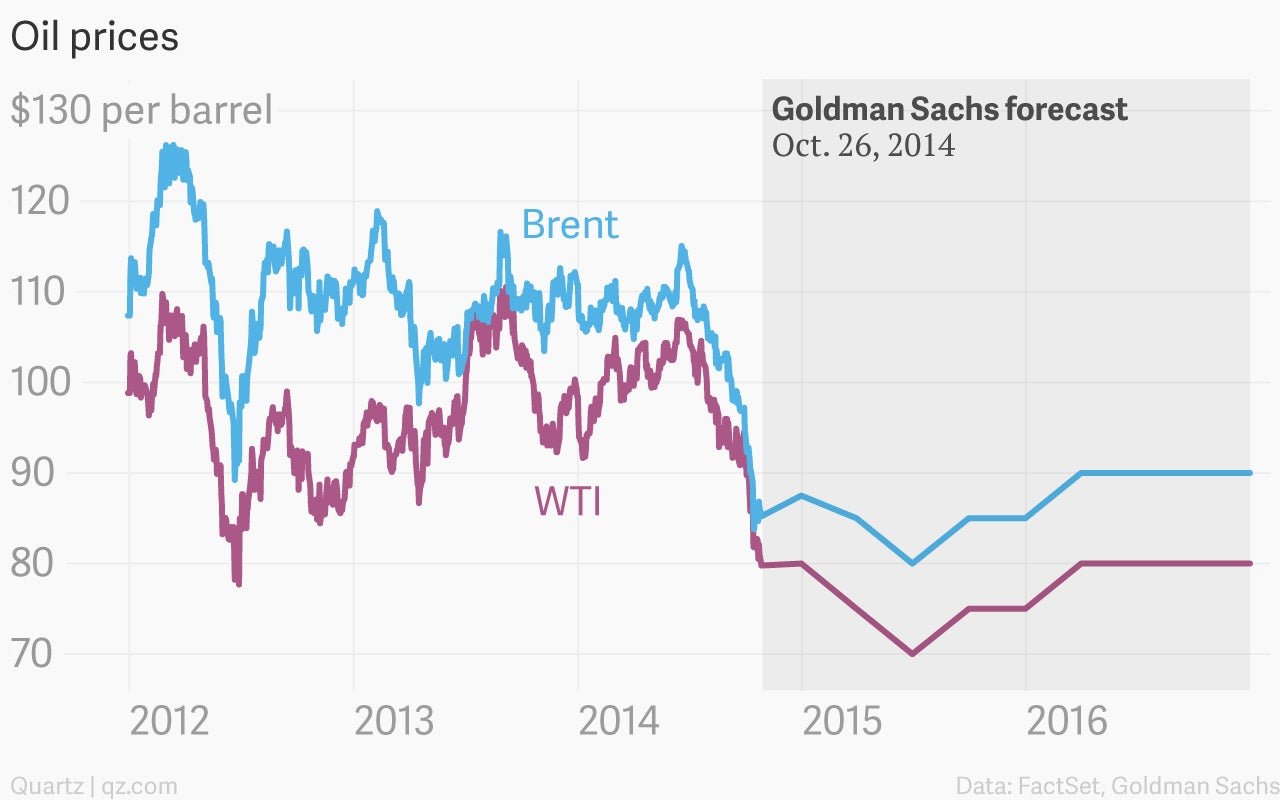

Oil prices have been plunging for more than six weeks now, falling more than 20% off their highs of about $115 in June. But in what it calls “The New Oil Order,” Goldman Sachs $GS says that US shale-oil drillers have become so potent that they have supplanted OPEC as the reigning global powerhouse. These shale drillers, and not the Saudi-led cartel, will for some time govern oil prices, the bank says in an Oct. 26 note to clients.

As a first order of business, says Goldman, internationally traded Brent crude will drop to $80 a barrel the second quarter of next year, 30% below the price just five months ago.

The pronouncement comes on top of a series of similar notes from Citi. But as another establishment bank coming to the same conclusion, Goldman spooked traders, who at the end of last week pushed prices back up a bit but yesterday resumed their oil selloff. They bid Brent down to $85.37 a barrel.

These are misery levels for fiscally loose oil producers. Prudent Kuwait can cover its state budget at $63-a-barrel Brent, Goldman estimates; even Saudi, with its generous handouts to the restive members of its society, can balance the books at $85. But not Russia. It requires $104 a barrel; for Iran, the number is $139. Goldman didn’t estimate Venezuela’s break-even price, but recent reports by Reuters and the Wall Street Journal put the number at $117-$121 a barrel.

The reason for this massive upheaval is a perfect storm of bad news, if you happen to be a petrostate—a surge of 1 million barrels a day of new supply this year from the US, with another such gusher of new US oil expected next year, plus a revival of the fortunes of Libya, whose production rose to 900,000 barrels a day in October, up from about 200,000 in July.

This new supply has entirely swamped demand, which will grow at just 630,000 barrels a day this year, or half what Goldman had projected. Goldman thinks demand will pick up next year, but not enough to meet the expected new 2015 supply.

All is not lost, Goldman said, however. It thinks that starting next year, some US shale drillers will pull back production—sufficient to stabilize Brent at about $85 a barrel the second half of 2015 and $90 in 2016, where it will stay for a few years. This is not nirvana for Russian president Vladimir Putin, but at least it would be stable.

Goldman’s note relies on the premise that US shale-oil drillers, being rational actors, will produce less oil starting in a few months. An unknown factor, however, is the lesson taught by shale gas drillers, who have produced as much or more natural gas despite pulling rigs off the market—because their efficiency and productivity have gone up.

While Brent is the blend watched by petrostates, it’s not as relevant to US shale drillers, whose oil is sold according to the US-traded benchmark known as West Texas Intermediate (WTI).

According to Goldman, WTI will dive to $70 a barrel in the second quarter next year before stabilizing at $80 a barrel in 2016. (WTI closed yesterday at $80.68.) Goldman doesn’t address this question, but a substantial risk to its forecast is that US production doesn’t drop, or not as much as it expects–that the same rise in efficiency experienced in shale gas will happen to shale oil. If it does, the price may not stabilize as it expects, but may instead go even lower. If it does, the geopolitical shakeout could be more profound.