In the age-old contest between stocks and bonds, stocks triumphed once again in 2014—at least in the US.

In the age-old contest between stocks and bonds, stocks triumphed once again in 2014—at least in the US.

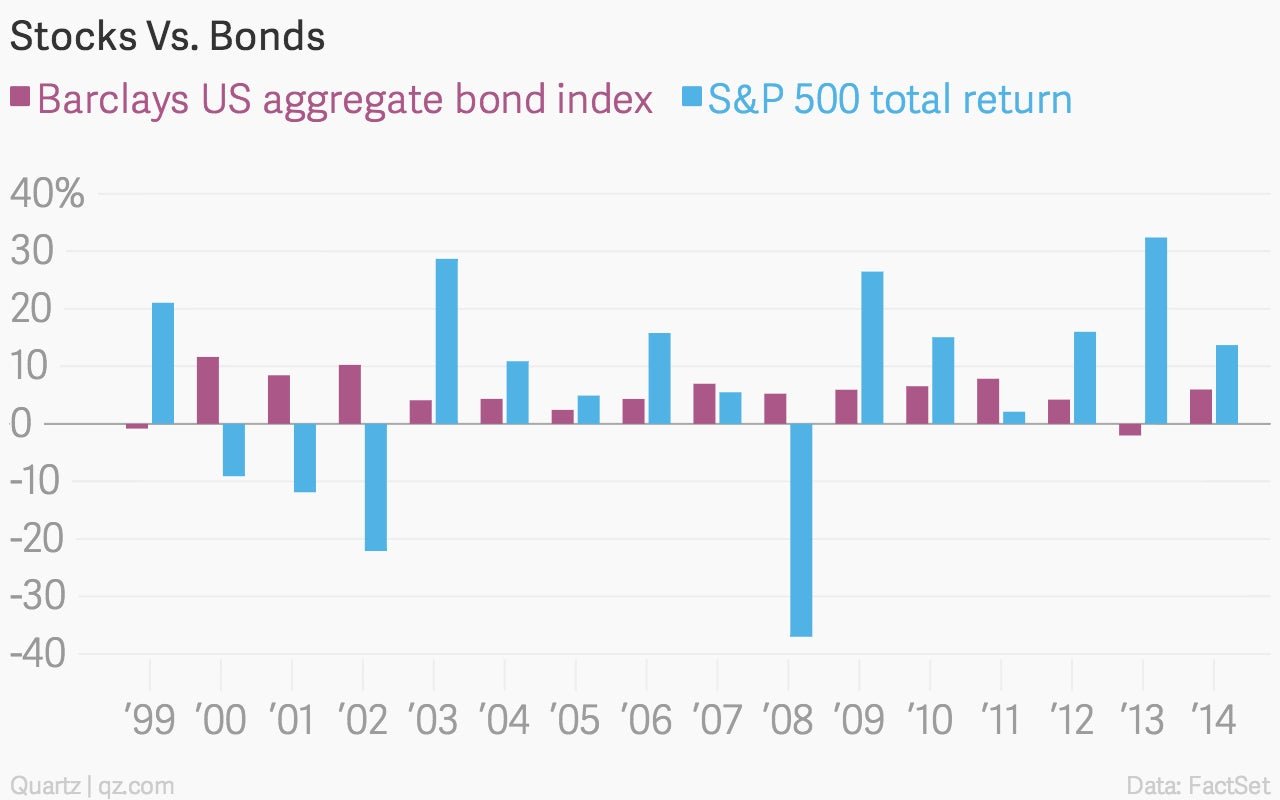

The broadest gauge (pdf) of the investment-grade US bond market, the Barclays US Aggregate bond index—it doesn’t include speculative-grade debt—delivered respectable returns of 5.97% for the year, including capital appreciation and coupon payments. The US benchmark S&P 500 easily outpaced that, delivering a 13.69% return from price gains and dividend payments combined. (Price gains alone accounted for an 11.39% increase.)

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

While stocks didn’t match their 2013 returns of 32.39%, 2014 marked the third straight year of double-digit gains for US equities, as investors priced in an economic recovery showing significant momentum. On the other hand, the bond markets showed resilience, bouncing back from a decline in 2013, as flight-to-safety inflows to the US—driven in part by global unrest such as that seen in Russia and Ukraine—helped keep US interest rates low. (Rising interest rates would have hit the bond market, as rising rates push bond prices down.)

Of course, we’re talking in terms of indexes. There were plenty of individual bonds that did much better than stocks this year. And there are always stock market dogs that trail bonds. But with more retail investors piling into index funds in recent years, it’s always worth looking at the big picture.

So what about 2015? Will it finally be the year of the big bond market sell-off? Probably not. Sure, the market will be tested, especially as the US Federal Reserve finally raises interest rates, which is widely expected to happen this year. The thing that investors should remember is that in the long run, stocks outperform bonds. But they also should remember that even during the worst year in recent memory for US bonds markets—1994—the Barclays Aggregate index was down only 2.9%. Compare that loss to the gobsmacking collapses of the early 2000s or the 37% decline in 2008.

It’s hard to overstate how damaging losses like this are for individual investors. Because of the mathematics of investment losses, investors need to generate percentage gains in excess of their losses just get back to square one. That’s why investment legends such as Warren Buffett stress that the first rule of making money is to avoid losing it.