The Fed has been laser-locked on keeping up the momentum in the US housing market. In its asset-purchase program, known as QE3, it’s been buying the mortgage bonds where almost all US home loans eventually end up. Doing so pushes rates lower in the secondary markets where traders buy and sell those bonds. And, in theory, those lower rates are passed along to consumers by the banks.

The Fed has been laser-locked on keeping up the momentum in the US housing market. In its asset-purchase program, known as QE3, it’s been buying the mortgage bonds where almost all US home loans eventually end up. Doing so pushes rates lower in the secondary markets where traders buy and sell those bonds. And, in theory, those lower rates are passed along to consumers by the banks.

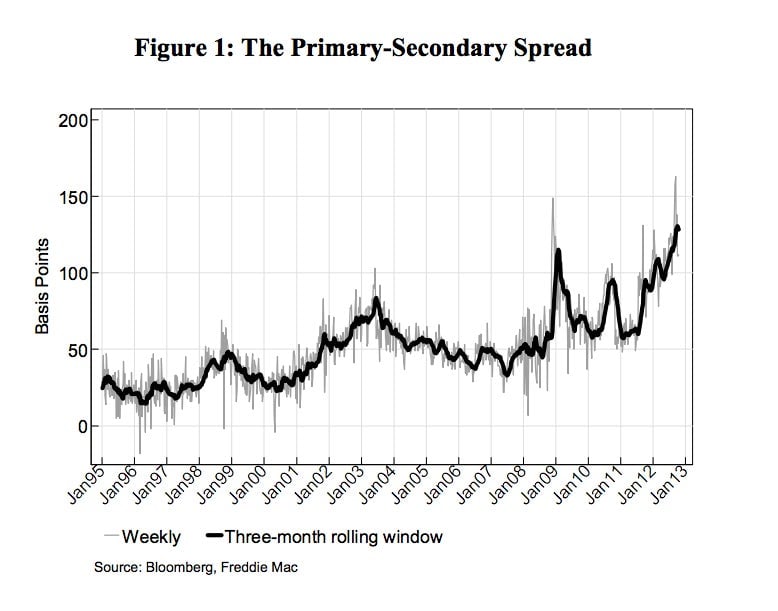

The problem is that the banks aren’t passing on all the savings they could. How do we know? One measure is the primary-secondary spread. This is the difference between the average mortgage rate consumers are offered and the benchmark rate on mortgage bonds in the financial markets. It serves as one gauge of the profit a bank can make on a mortgage. And recently, as mortgage rates have hit historic lows, the spread has blown out to historic highs. Here’s a look from a Fed paper published recently.

Join 500,000+ readers who start their day with Quartz.

By subscribing, you agree to our Terms of Service and Privacy Policy.

Economists from the Fed churned out a paper recently calculating whether the bigger spread means the banks are making bigger profits (Answer: yes) and trying to figure out why. This matters because the main point of the Fed’s bond-buying is to make mortgages cheaper for home-buyers, not to make them more profitable for banks. The short version is that there are a bunch of factors at play. Over at WSJ.com’s Developments blog they give a nice summary.

But we found one of the lines of reasoning in the Fed paper somewhat strange. It was over the question of concentration in the mortgage market. There’s a theory that because a few big banks control most of the mortgage world, they aren’t competing against one another as fiercely, so they can get away with offering rates that aren’t quite as low. The Fed paper downplays this notion (emphasis ours):

It is well-known that the mortgage market in the United States is dominated by a relatively small number of large banks that originate the majority of loans. However, as shown in Figure 10, a simple measure of market concentration given by the share of loans made by the largest five or ten originators has actually decreased over the period 2011-12, as a number of the large players have decreased their market share (while the largest originator has further increased its origination share). Thus, market concentration alone is unlikely to provide an explanation of high profits in the mortgage business.

Really? You’ll look at market concentration over the last year alone? That seems a strange way to measure things. Don’t take our word for it. Listen to Ed DeMarco, the acting head of the Federal Housing Finance Agency, an important US housing regulator (again, emphasis ours):

I would like to see the mortgage market of the future become more competitive than it is today. We have seen a great deal of concentration in mortgage origination and in mortgage servicing in recent years. This has come, in part, at the expense of small and local banks and thrifts, institutions with both local market knowledge and direct and multiple relationships with borrowers.

During the first half of 2012, three banks—Wells Fargo $WFC, JP Morgan and US Bancorp—originated half the mortgages in the US. Three. Wells Fargo alone made more than one third of the mortgages. By itself. According to Bloomberg, back in the 1990s a lender with 7% of the mortgage market would have been considered a big player.

Even the head of the New York Fed, Bill Dudley, has acknowledged that the mortgage market is increasingly concentrated. In a speech back in October, when Dudley explained why the Fed wasn’t getting as much bang for its buck, the power of the banks was the first thing he mentioned (emphasis ours):

The incomplete pass-through from agency MBS yields into primary mortgage rates is due to several factors—including a concentration of mortgage origination volumes at a few key financial institutions and mortgage rep and warranty requirements that discourage lending for home purchases and make financial institutions reluctant to refinance mortgages that have been originated elsewhere.

In a speech on the topic at the New York Fed this week, Dudley mentioned similar factors, though his focus on the market power of the banks seemed a tad more muted. Of the Fed’s paper on the rise of bank profits he says:

The study examines a number of potential explanations. These include capacity constraints, market concentration, pricing power over Home Affordable Refinance Program (HARP) refinance loans and pricing power on other loans. It finds that capacity constraints play a role and that there is evidence to suggest that originators enjoy pricing power and elevated profits on HARP and other refinancings.

Why this dancing around what seems to be an obvious problem? At the very least, it seems high time that the folks at the Fed devote their considerable powers and expertise to a study focusing exclusively on the concentration of lending among banks in the US mortgage market, and whether that is holding back the US recovery as a whole.