Investors suddenly seem to think the outlook for the music business is not as bleak as the commentary surrounding it suggests.

Consider the following examples:

Let’s focus on the last one. New York-based P. Schoenfeld Asset Management (PSAM) is pressing for changes at French media conglomerate Vivendi aimed at boosting the company’s share price. Most of PSAM’s suggestions are pretty boring, except for a proposal to spin off Universal Music, the world’s biggest music company, which controls more than 30% of the global recording industry.

It’s worth noting from the outset that PSAM owns less than 1% of Vivendi. It’s trying to pull off a classic “activist” campaign (the Carl Icahn way of building a stake in a company and then whining about its performance) to rally support from other shareholders for changes it wants to make. As a result, its projections about Universal’s performance are inherently biased. Yet they’re still notable for those interested in the future of the music business.

In a presentation (pdf), PSAM argues that the underlying value of Universal is obscured by Vivendi’s conglomerate structure, and that the stock market “systematically undervalues” the bump it will get from subscription-based streaming music, which could be poised for a major expansion, particularly with Apple $AAPL about to enter the fray.

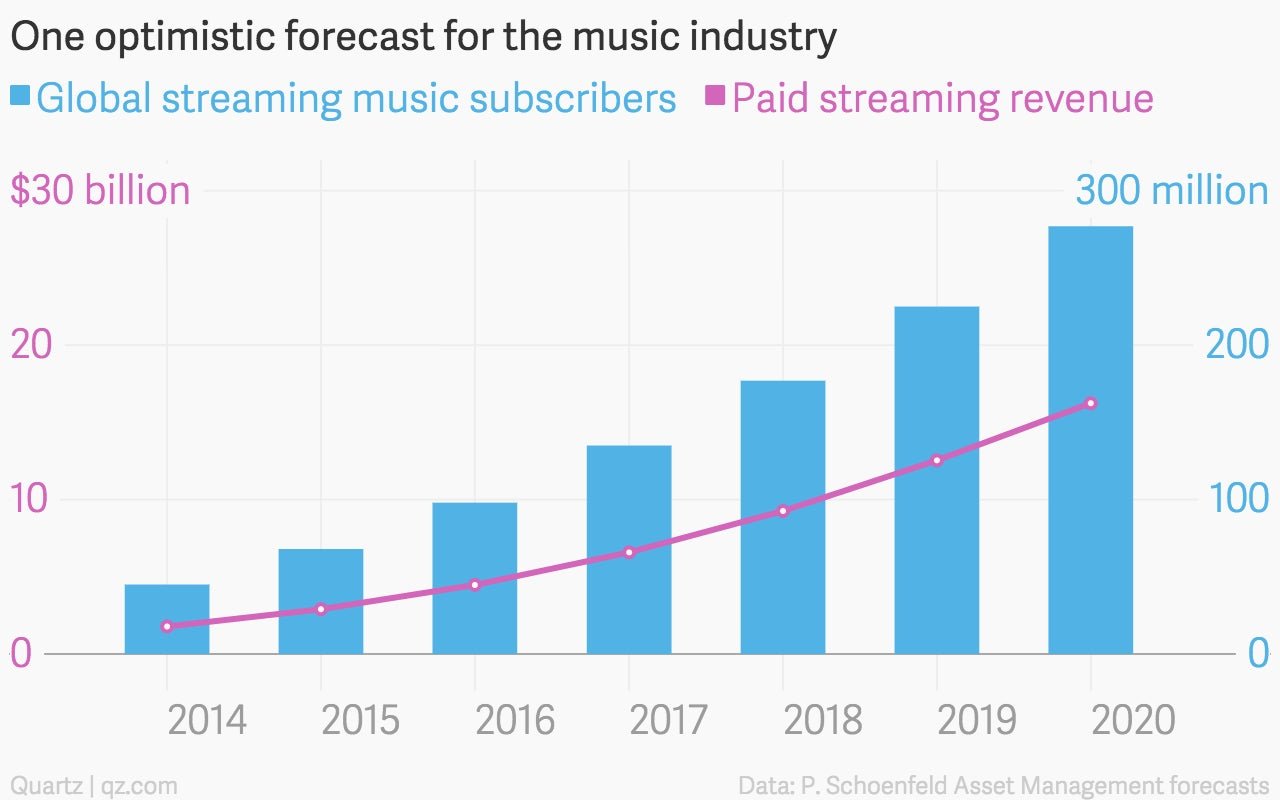

PSAM argues there will be more than 250 million streaming music subscribers globally by 2020 (that number is about 5% of the predicted global smartphone customer base in 2020, which PSAM thinks will be 5.03 billion). These subscribers alone, it goes on to say, will generate $16.42 billion in revenue—more than the entire global recorded music industry (including physical sales and downloads) is expected to generate this year ($14 billion).

Interestingly, that $16.42 billion works out to just $5.45 per month per subscriber—less than the $10 a month most streaming services currently charge—which would suggest that different pricing models may take hold.

In any case, streaming platforms like Spotify return about 70% of their revenues to record labels and publishers in royalties, and since Universal is both the world’s largest record company and one of its largest publishers, it would presumably receive a very significant chunk of that money.

These projections for revenue and global streaming subscribers are much more bullish than anything we’ve seen yet—and they’re extremely hypothetical. Credit Suisse, for example, expects paid streaming to be a $12.2 billion market by 2020, with fewer than 150 million subscribers globally.

Also, the spinoff of Universal Music might never happen. Vivendi’s CEO has said he will sell Universal “over my dead body,” and the company formally rejected PSAM’s other proposals on Mar. 24.

Still, investor optimism about the music industry is refreshing. PSAM’s extremely bullish projections have the total recorded music market approaching $26 billion by 2020. That’s not quite the $38 billion it hit at its peak back in 1999, but it’s almost double where it is today.